Posts by CharlesHugh:

The World of Work Has Changed, and It’s Never Going Back to the “Good Old Days”

December 22nd, 2015By Charles Hugh.

Wishful thinking is not a solution.

The world of work has changed, and the rate of change is increasing. Despite the hopes of those who want to turn back the clock to the golden era of high-paying, low-skilled manufacturing jobs and an abundance of secure service-sector white collar jobs, history doesn’t have a reverse gear ™.

The world of work is never going back to the “good old days” of 1955, 1965, 1985, or 1995. Jason Burack of Wall Street for Main St. and I discuss these trends in a new podcast, Radical Changes in the Job Market, Now & in the Future (47:37).

Those hoping for history to reverse gears place their faith in these wishful-thinking fantasies:

1. That automation will create more jobs than it destroys because that’s what happened in the 1st and 2nd Industrial Revolutions. The wishful thinkers expect the Digital / 3rd Industrial Revolution to follow suite, but it won’t: previous technological revolutions generated tens of millions of new low-skill jobs to replace the low-skill jobs that were lost to technology.

Millions of farm laborers moved to the factory floor in the 1st Industrial Revolution, and then millions of displaced factory workers moved to sales and clerk jobs in the 2nd Industrial Revolution.

Even white-collar jobs that supposedly required a college degree could be learned in a matter of hours, days or at most weeks, and little effort was required to stay current.

The Digital/3rd Industrial Revolution is not creating tens of millions of low-skill jobs, and it never will. Even worse for the wishful thinking crowd, the 3rd Digital Revolution is eating tech jobs along with the full spectrum of service-sector jobs.

Those expecting to replace low-skill service jobs with armies of coders will be disappointed, because coding is itself being automated.

The new jobs that are being created are few in number and highly demanding. Jobs are no longer strictly traditional boss-employee; the real growth is in peer-to-peer collaboration and what I term hybrid work performed by Mobile Creatives, workers with highly developed technical/creative/social skillsets who are comfortable working with rapidly changing technologies, who enjoy constant learning and are highly adaptive.

The work that is being created in the Digital/3rd Industrial Revolution is contingent and thus insecure. The only security that is attainable in fast-changing environments is the security offered by broad-based skillsets, great adaptability, a voracious appetite for new learning and a keenly developed set of “soft skills”: communication, collaboration, self-management, etc.

I cover all this in depth in my book Get a Job, Build a Real Career and Defy a Bewildering Economy.

The problem is the number of these jobs is far smaller than the number of jobs that will be eaten by software, AI and robotics. the number of workers who can transition productively to this far more demanding and insecure work environment is also much smaller than the workforce displaced by software/robotics.

In short, we need a new system; wishful thinking isn’t a solution.

2. That the U.S. can unilaterally demand the right to export its goods and services to others at full price while refusing to accept competing imports. In effect, the fantasy is to return to 1955, when the U.S. could export goods at full pop to the allies who were rebuilding their war-shattered economies. Imports were few because those economies were busy focusing on their own domestic needs.

Trade is a two-way street. Fair trade is a moving target, depending on which side of the trade you happen to be on. Everybody wants to export their surplus at top prices, but competition lowers prices and profits. This forces global corporations to seek cost advantages by lowering the cost of components and labor.

3. The wishful thinkers want strong corporate profits to prop up their stock market and pension funds, but they don’t want corporations to do what is necessary to reap strong profits, i.e. move production of commoditized goods and services overseas or replace human labor with cheaper automation.

You can’t have it both ways.

Wishful thinkers choose to ignore the reality that roughly half of all U.S. based global corporate sales and profits are reaped overseas. It makes zero financial sense to pay a U.S. worker $20/hour, and pay the insanely expensive costs of sickcare/”healthcare” in the U.S. when the work can be done closer to the actual markets for the goods and services at a fraction of the cost.

Memo to all the armchair wishful thinkers: if you want to compete globally with a high-cost U.S. work force and no automation, be my guest. Put your own money and time at risk and go make it happen. Go hire people at top dollar and provide full benefits, and then go out and make big profits in the global marketplace.

The armchair pundits and ivory tower academics would quickly lose their shirts and come back broke. That’s why they wouldn’t dare risk their own security, capital and time doing what they demand of others.

4. The wishful thinkers decry the lack of “good-paying” jobs yet they refuse to look at the reasons why employing people in the traditional boss/employee hierarchy no longer makes sense. The armchair pundits and ivory tower academics have never hired even one person with their own money. These protected privileged are living in a fantasy-world of academia, think tanks and foundations, where workers are paid with state money, grants, venture capital, etc.

As I have often noted here, Immanuel Wallerstein listed the systemic reasons why labor overhead costs will continue to rise even as wages stagnate. This means employers see total labor costs rising even if wages go nowhere: it gets more and more expensive to hire workers.

Why I Will Never Hire Anyone, Even at $1/Hour (November 10, 2015)

Then there’s the staggering burden of liability in a litigious society, the costs of training and supervising ill-prepared employees and the hard-to-calculate costs of increasingly complex regulations.

5. We can solve the decline of the traditional work model with more education. This is also wishful thinking, as not only is higher education failing to produce workers with the requisite range of skills, the emphasis on higher education has produced an over-supply of people with college diplomas.

The Nearly Free University and the Emerging Economy: The Revolution in Higher Education.

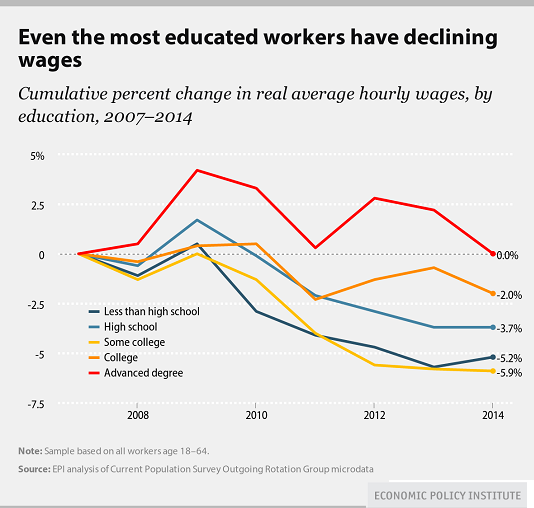

In the real world, even wages of the most highly educated are stagnating.

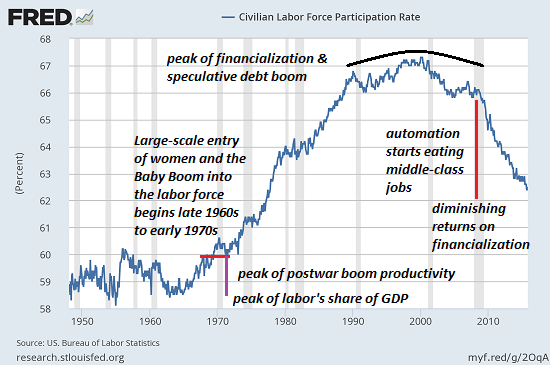

The structural changes in the world of work are visible in these charts:

The civilian participation rate is plummeting, despite the “recovery:”

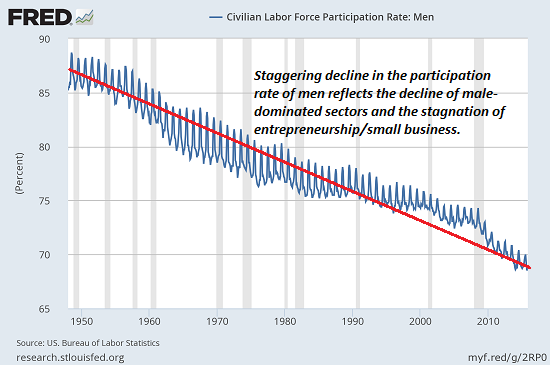

The civilian participation rate for men is in a multi-decade decline:

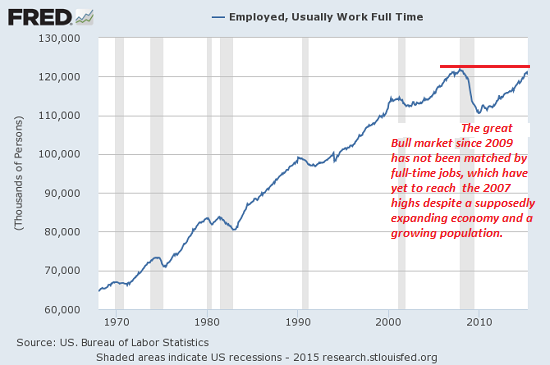

Part-time jobs do not provide enough income to have an independent household or raise a family, nor do they pay enough taxes to fund the Savior State. The only jobs that count are full-time jobs, and they haven’t even returned to 2007 levels despite a higher GDP and a rising population.

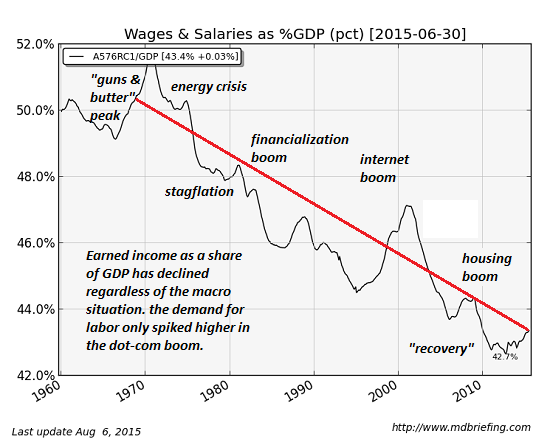

As a percentage of GDP, wages have been declining for decades.

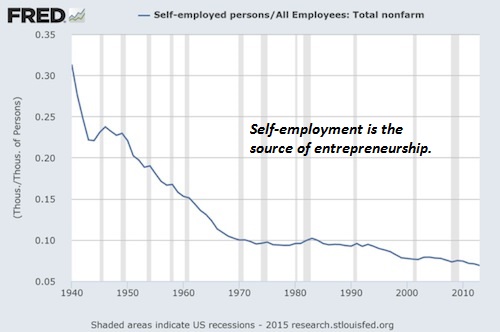

Self-employment is the wellspring of entrepreneurs and small business. As you can see, it has also been declining for decades.

It’s time to get real, people. Wishful thinking is not a solution. We need a new system for creating paid work and money, and here’s my proposed alternative system: A Radically Beneficial World: Automation, Technology and Creating Jobs for All.

Wall Street for Main St. podcast (47:37): Radical Changes in Jobs Market Now & in Future

Comments Off on The World of Work Has Changed, and It’s Never Going Back to the “Good Old Days”

About Those Forecasts of Eternally Rising Corporate Profits

June 6th, 2014

By Charles Hugh.

If corporate profits decline, what will hold up the market’s lofty valuations other than the tapering flood of liquidity from the Federal Reserve?

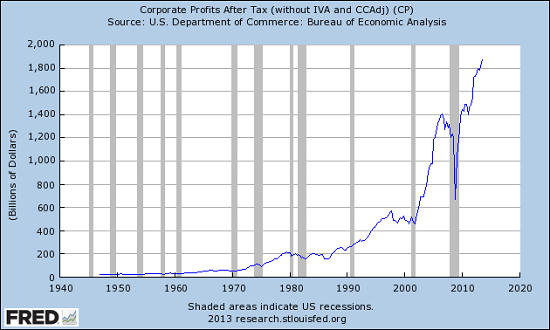

I have often noted that profits of global U.S. corporations have been boosted by the weak U.S. dollar (USD). In a weak-dollar environment, a company need not sell more goods or services or expand margins to book more profit: all a corporation needs to do is book profits earned in other currencies in dollars.

When the euro and the dollar were 1-to-1 back in the early 2000s, 100 euros of profit converted to $100 when stated in dollars. With the euro around $1.36, the same 100 euros of profit earned by the U.S. corporation in Europe converted to a $136 in profit when stated in dollars–a hefty 36% premium gained entirely as a result of the weak dollar.

This explains why the Fed has been so keen to trash the dollar: it magically increases corporate profits and thus drives stocks higher. The mainstream financial media’s explanation for the weak-dollar policy is that the Fed is anxious to increase exports, but this is a sideshow; exports make up less than 9% of the U.S. GDP. The real action is in corporate profits, which thanks to the weak dollar are near all-time highs of $2 trillion, about 12% of the nation’s entire GDP.

Courtesy of our friends at Market Daily Briefing, here is a chart of the USD and the S&P 500 stock index. Note that when the USD is strong, profits decline, and when the dollar is weak, profits soar:

For a variety of reasons, the dollar is in a long-term uptrend. These reasons include global capital flows, Triffin’s Paradox and the need to defend the dollar to prop up the U.S. Treasury bond market and fund the U.S. deficit. I have covered these topics in depth over the past few years:

What Will Benefit from Global Recession? The U.S. Dollar (October 9, 2012)

Understanding the “Exorbitant Privilege” of the U.S. Dollar (November 19, 2012)

Why the Shrinking Trade Deficit Will Choke U.S. Corporate Profits (August 8, 2013)

We can see the uptrend in a chart of the U.S. dollar. There’s nothing fancy here; the USD bottomed in late 2011 and advanced into a trading range that has lasted two years. A year-long triangle pattern has been broken to the upside, a move that can be viewed as a continuation of the uptrend from 2011.

Many observers focus on the eventual consequences of large-scale credit/money-printing, i.e. debasement of paper (fiat) currencies. While this may yet occur, the credit issuance/money printing of the Fed is actually modest compared to other issuances of credit/currency, and is tapering as the Fed is forced to defend other parts of the global Empire, for example, the Treasury bond market.

The dynamics and consequences of the various currency players’ actions are not linear, and so predictions based on linear projections are often wrong. But I think these two dynamics–the correlation of the weak dollar to global U.S. corporate profits and the dollar strengthening as other players’ fundamentals unravel–will be dominant, and the ones to watch in terms of explaining why U.S. corporate profits will weaken, regardless of sales and margins.

And if corporate profits decline, what will hold up the market’s lofty valuations other than the tapering flood of liquidity from the Federal Reserve? Answer: nothing.

Complacent punters will discover to their great dismay that liquidity is only one dynamic of many.

Comments Off on About Those Forecasts of Eternally Rising Corporate Profits