January 2nd, 2018

By Marc Chandler.

The New Year may have begun in fact, but in practice, full participation may return only after the release of US employment data on January 5. The macroeconomic and policy tables have been set, though interpolating from the Overnight Index Swaps market, there is 45% chance the Bank of Canada hikes rates at its policy meeting near the middle of the month.

In the currency markets, sentiment appears to be as uniformly dollar negative as it had been positive a year ago. More important for the near-term price action, there have been powerful but extended trends over the past two-three weeks as participation thinned. Consider that the Canadian dollar appreciated nine of the past 10 sessions. The Australian dollar rose in 13 of the last 15 sessions.

It is too difficult to find a consistent narrative of what the market is saying. The rally in industrial metals and equities suggest an economically optimistic outlook. However, the rally in the US Treasuries and the flattening yield curves in most advanced economies would seem to be consistent with downside risks. There is no sign in recent data that the synchronized upturn is slowing. In fact, on balance, data from Q4 suggests, growth may have accelerated.

The flash PMI for the eurozone is expected to be confirmed in the coming days. The composite firmed to a new cyclical high 58.0 from 57.5 in November. It averaged 56.0 in Q3. The composite PMI was at 54.4 at the end of 2016. Not only has economic activity quickened but it also broadened. Italy and France, and no less than Greece are participating.

Data over the last couple of weeks suggests that what might have begun as an export-led growth in industrial output and capital investment has spread to consumption. Overall household spending rose 1.7% year-over-year in November. This is the second strongest pace in more than two years.

China, the world’s second-largest economy, is also finishing the year on a firm note. The official manufacturing PMI slipped to 51.6 in December from 51.8 in November. The Q4 average was 51.7 after 51.8 in Q3 and 51.5 in H1. The non-manufacturing PMI edged up to 55.0 from 54.8. It averaged 54.7 in Q4 and 54.4 in Q3, following a 54.5 average in H1.

Of the large countries, India’s economy may be the most concerning. After a good H1 2017, the economy struggled in Q3. The composite PMI posted the year’s high of 51.7 in June before falling below the 50 boom/bust level in July and August. The recovery in September and October (51.3) fizzled out in November (50.3). The December reading is due January 4.

The minutes from the December FOMC meeting that delivered the third hike of the year will be scrutinized for clues into the bar for a March move. Assuming that there is no practical chance of a hike at the next FOMC meeting, the market appears to have discounted a little less than a 60% chance of a March hike.

The US jobs data is the economic highlight of the holiday-shortened first week of the New Year. Even modest disappointment with the December report will not prevent 2017 from being the seventh consecutive year the US economy created more than two million jobs. A little more than 8.5 mln jobs were lost 2008-2009 and 18 million jobs have been created since.

Job growth is expected to have cooled in December after two months in which 472k net new jobs were created. Newswire survey put the median guesstimate near 190k. Manufacturing has been on a hiring binge, with 54k new positions in October and November. Another 20k are expected to have joined the payrolls in December Through November, the manufacturing sector jobs have risen by 16k on average. Last year, there was an average loss of 1k manufacturing jobs.

In November, the work week ticked up to 34.5 hours. It is the third time in 2017 it has risen there, but each time it was quickly turned back. Some observers suggest there needs to be a sustained increase in the work week to boost the likelihood of wage pressure. Average hourly earnings need to rise by 0.3% in December to keep the year-over-year rate steady at 2.5%.

US auto sales are not particularly interesting presently. Sales had slowed in the March through August period. The terrible destruction of a couple of storms helped boost auto sales, and arguably, save the year. Through November the pace has averaged 17.11 mln (annualized pace) vehicles. This is the lowest in three years (17.45 mln in 2016 and 17.40 mln in 2015). December auto sales are expected to be around the 17.5 mln unit pace.

Geopolitical developments in recent days will be part of the talking points to start the New Year. In particular, reports that to show Russia and Chinese ships transferring fuel to North Korean vessels. Meanwhile, large urban protests in Iran, ostensibly over rising food and fuel prices, are apparently capturing the imaginations of many observers. The details are not particularly clear, and the press converge appears laced with ideological assumptions. The protests may have begun out orchestrated, but appear to metastasized into a something else. The demonstrations seem smaller than in 2009 (Green Movement). The government’s response has thus far been restrained.

Meanwhile, four political issues in Europe that are unresolved at the end of 2017 need closure in early 2018. Catalonia new regional parliament will take office January 17. The government it will create is not clear. Once the independence issue is subsumed by other issues, it is not clear the programmatic basis for a coalition of the independent-minded parties, whose views seem to extend across the political spectrum.

Germany has been unable to put together a government following the late September elections. The demand by the SPD for dramatic European integration cannot be accepted by the CDU/CSU Mathematically, appears to be three alternatives: A coalition government, a minority government, or new elections. The first is proving difficult. Merkel appears to have ruled out the second. Given that CDU, CSU, and SPD did the worst in modern history in the September election, a return so soon to the polls may be a nuclear option.

Brexit negotiations shift to the terms of the transition period after the end of March 2019 that the UK seeks. The UK is going to want to maximize its new position, while the EU wants to maintain the integrity of its institutions. After March 2019, the UK is not in the single market, but during a transition period, it will act as if it does without having a say in the formulation of new rules.

If the UK were to strike a new free-trade agreement with a third country, wouldn’t that leave the EU vulnerable to disruption? Shouldn’t the European Court of Justice still have sway where it currently does? And if the UK will still have access to the single market, ought it not abide by the EU’s immigration policies?

The EU-Polish conflict may come to a head in January. The EU objects to the government’s judicial reforms, which undermines the independence of the courts. Poland is of no mind to comply. The EU’s ability to escalate is limited by the need for the decision to be unanimous.

The confrontation with Poland is part of the broader fissure with the Visegrad countries (Poland, Hungary, Czech, and Slovakia). When the Soviet Union collapsed, there was a brief moment when nationalism and democracy coincided, but the former appears more dominant currently than the latter, and this rattles Western European sensibilities.

A new political story for 2018 will be the Italian elections on March 4. They will be the first under a new electoral law. Part of the purpose of the new electoral law is to provide for more stable governments. However, the camel that is the horse made by competing interests and motivations, may not be up to the job.

Polls suggest that no party or block will achieve a majority. A coalition government then is most likely come March. A broad coalition of center left and center right–a different shade of gray than the current government, excluding the 5-Star Movement–is the most likely scenario. The uncertainty, however, may see Italian assets underperform in the first part of the New Year, potentially creating new opportunities for Q2.

With US tax changes having been legislated late in 2017, the debate over the implication and meaning for US companies as well as subsidiaries and branches of foreign companies operating in the US will continue. The repatriation of foreign earnings will be monitored closely. The political agenda shifts to Trump’s infrastructure initiative. The conventional wisdom is that it will be difficult for Democrats, especially Senators from states that Trump carried in 2016, not to support an infrastructure bill, ahead of the midterm elections.

Although the US Administration’s actions on trade did not match some of the fiery rhetoric in 2017, it is still the early days. NAFTA negotiations resume this month. The US appears frustrated that Mexico and Canada are not making counteroffers on some of its more aggressive demands. A risk of a collapse in talks seems to be elevated at the start of the New Year. US-China trade tensions also seem set to escalate.

Even if the precise calibration is not knowable, we suspect many of the macroeconomic relationships hold, and that the business cycle has not been repealed, even if elongated and flattened. We think underlying price pressures are already increasing and expect this to be more evident in the coming months. We anticipate global higher interest rates and wider differentials favoring the US. The US agenda of deregulation, corporate tax cuts, including fully expensing capital investment, and protectionist threats will attract capital.

Comments Off on The Past is Not Passed: 2017 Spills into 2018

October 31st, 2017

Global equity markets are closing another strong month. The MSCI Asia Pacific Index was little changed on the day, but up 4.3% in October, the 10th consecutive monthly advance. Europe’s Dow Jones Stoxx 600 is also flattish today, but up 1.6% on the month. It is the second monthly advance after a June-August swoon. The benchmark is closing in on the high for the year set in May. The S&P 500 made new record highs at the end of last week. Coming into today’\s session, the S&P 500 is up 2.1% on the month, and since last October, has only posted a single losing month (March -0.04%).

While global equity markets rally, seemingly no matter what, the bonds and currencies know more than one direction. The US 10-year yield recorded the low for the year just above 2.0% in early September. It has since risen to around 2.47% and has backed off in recent sessions. A few attempts in Q2-Q3 to push above this area have failed. We suggested that a move below around 2.35% would spur ideas that this recent attempt has also failed. This area was approached earlier today, and it held.

Interest rate differentials have moved against the US dollar in Q2-Q3 but have moved more forcefully in the dollar’s direction recently. The dollar is likely to close higher against all the major currencies this month. However, here the too market is testing key levels. For example, the $1.1600-$1.1660 band in the euro is important, and while the euro had edged into the high $1.1500s, but the break has not yet been convincing. A convincing break would suggest losses toward $1.1250. On the other hand, if it holds, another the euro can recover back to $1.18, if not higher.

The dollar has been turned back from the JPY114 area in May and July, and again probed this area last week.The poor price action ahead of the weekend warned of the risk of a setback, we thought, toward JPY113.00. This was tested earlier today and it, reinforced by the 20-day moving average (~JPY112.90), held.

Sterling rallied in strongly in the first half of September on the back of the latest hint that the BOE would likely raise rates. However, Brexit and political issues seemed to weigh it into the first part of October, and this month has chopped around a two-cent range. A dovish hike by the BOE, or no hike, for that matter, could send sterling back toward $1.30 for a more significant challenge. On the other hand, a broader dollar pullback and a hawkish comments or forecasts could see sterling challenge $1.3350-$1.3400.

The US dollar has trended higher against the Canadian dollar, and with last week’s gains, retraced 50% of this year’s slide. To keep the upward momentum intact, the greenback must convincingly surmount the CAD!.2930 area. On the other hand, the support is seen in the CAD1.2725-CAD1.2750 area.

Today’s news stream and month-end adjustments will likely prevent a decisive move today. In terms ofeconomic developments, there have been a few highlights. First, China’s PMI. It will not surprise many that some less favorable news on the economy may have been held back ahead of the recent 19th Party Congress. In any event, the October PMIs softened. The manufacturing PMI slipped to 51.6 from 52.4, which is a bit larger of a drop than expected. The non-manufacturing PMI eased to 54.3 from 55.4. Forward-looking new orders and prices moved lower. President Xi did not repeat the goal of doubling China’s GDP in the 2010-2020 period, and many observers recognize that this could allow the country to report slower growth, which would be consistent with the shift toward quality issues.

Second, the BOJ did not change policy. It did, though, recognize the inevitable and brought this year’s inflation forecast to 0.8% from 1.1%. Next years was shaved to 1.4% from 1.5%. The GDP forecast was tweaked to 1.9% from 1.8% this year and left unchanged at 1.4% next year. Of note, the new board member, Kataoka dissented again, arguing for new measures to achieve the 2% inflation target. He argued to cap the 15-year yield below 20 bp. It is currently near 30 bp. Also of interest, Governor Kuroda did not waver on the ETF purchases (JPY6 trillion target). The Nikkei 400, which the ETF tracks is up 5.7% this month, and the BOJ is believed to have pulled away from its purchases.

Third, the eurozone reported better growth, but less inflation, than expected. The first look at Q3 GDP showed a 0.6% increase, and Q2 was revised to 0.7% from 0.6%. Growth is not the immediate challenge in the eurozone. Unemployment also continues to fall. At 8.9% in September, it is a new cyclical low. That the August figure was revised to 9.0% from 9.1% underscores the trend improvement.

On the other hand, price pressures eased. The headline pace slipped to 1.4%, but the real challenge to the ECB comes from the core rate, even though it does not directly target it. The core rate slipped to 0.9% from 1.1%. Thisindicates that it is not just energy prices, which Draghi had warned would likely drag inflation lower in the near-term. The key issue is what the ECB will do next September, as its course until then has been largely mapped out, with all the due caveats of its flexibility.

Fourth, the Catalan secessionist move has been thwarted. The leader, Puigdemont, reportedly is in Brussels seeking asylum. Madrid invoked Article 155, but importantly, it simultaneously called for quick elections (before Christmas). Madrid was taking away its autonomy and then giving it back quicker than anyone anticipated. Spanish stocks and bonds are outperforming a bit today, but note that the peak in the crisis was actually several weeks ago.

The New Zealand’s dollar appears to be trying to bottom, from a technical point of view, but the political/policy headwinds are a deterrence. Comments from the Finance Minister give the bears little reason to fear official concern despite 10% slide in the Kiwi over the past three months. The moves to deter foreign speculation (investment?) in New Zealand real estate is seen cutting into an important source of demand for the currency. That said, we continue to suspect that just as the market overreacted to Trudeau’s victory in Canada and his effort to buck the new fiscal orthodox and stimulate, the market may be exaggerating the negatives of the new government, like giving the central bank a dual mandate.

There are some large options that expire in NY today. There is a 1.1 bln euro options truck at $1.16, and a $614 mln option struck at JPY113.00. There is a GBP350 mln option struck at $1.3200 that will be cut today.

In the US despite, the two indictments and a surprised guilty plea from a third person in the investigation into Russia’s attempt to influence the US election, the market impact was limited. It is a bit like a game of bridge where players are signaling each other, in this investigation, with the type of charges and the like, which createssubtext and bit of Kabuki theater. The takeaway seems to be that the investigation is still in the early stages and it will probably linger through at least most of next year.

Meanwhile, investors are more interested in the tax reform, and here the situation, even at this late date is very fluid. Although the speculation has been around for a couple of weeks, the possibility of gradually phasing in the corporate tax cuts (three percentage points a year from 2018 through 2022), was disappointing to those who wanted a big move, while it seemed to be a compromise on cost. News that Treasury Secretary Mnuchin had given up, for the time being, on extra-long dated bond spurred a quick though small reaction in the curve at the very long end.

http://www.marctomarket.com/2017/10/month-end-leaves-market-at-cross-roads.html

Comments Off on Month-End Leaves Market at Crossroads

October 9th, 2017

By Marc Chandler.

(from my colleague Dr. Win Thin)

EM FX ended the week under pressure, as US data points to a rate hike in December and perhaps more in 2018. FOMC minutes this Wednesday will be closely studied for clues. US retail sales and CPI data Friday will also be important. We believe the most vulnerable currencies in this environment are ZAR and TRY, but one could also add MXN and perhaps RUB to that mix too.

China reports September foreign reserves Monday, which are expected to tick up to $3.1 trln. Money and new loan data could come out this week, but no date has been set. Trade data will be reported Friday. Exports are expected to rise 9.8% y/y and imports by 15.2% y/y.

Turkey reports August IP Monday, which is expected to rise 5.1% y/y vs. 14.5% in July. Turkey then reports current account data Wednesday, where a -$1.35 bln deficit is expected. If so, the 12-month total will remain steady at -$37.1 bln. Overall, the external balances are still deteriorating.

Czech Republic reports August industrial and construction output and September CPI Monday. IP is seen rising 4.2% y/y vs. 3.3% in July, while CPI is seen rising 2.7% y/y vs. 2.5% in August. Rising inflation and a fairly stable exchange rate should lead the central bank to hike rates at the next meeting November 2.

Hungary reports August trade Monday, where a EUR480 mln surplus is expected. It then reports September CPI Tuesday, which is expected to rise 2.7% y/y vs. 2.6% in August. If so, it would still be within the 2-4% target range. The central bank just eased at the September meeting, and so no changes are expected at the next policy meeting October 24.

Mexico reports September CPI Monday, which is expected to rise 6.46% y/y vs. 6.66% in August. If so, this would be the first deceleration since June 2016. Still, inflation would still be well above the 2-4% target range and so Banxico is likely to keep rates steady until it comes down further. Mexico then reports August IP Thursday, which is expected to contract -0.5% y/y vs. -1.6% in July.

Russia reports Q2 current account Tuesday, where a deficit of -$2.8 bln is expected. If so, this would be the first deficit since Q3 2013, and the 4-quarter total would fall to $32.9 bln from $36.1 bln in Q2. Russia then reports August trade Thursday, where a surplus of $5 bln is expected vs. $4 bln in July.

Chile reports September trade Tuesday. Export growth has been robust in recent months, helped by higher copper prices. However, import growth remains restrained due to the sluggish economy, and so the 12-month total surplus has been rising. The external accounts should remain in solid shape.

Taiwan reports September trade Wednesday. Exports are expected to rise 13.4% y/y and imports by 8.2% y/y. The external accounts remain in good shape, and export orders remain strong enough to suggest that this trend will continue.

Brazil reports August retail sales Wednesday, which are expected to rise 4.4% y/y vs. 3.1% in July. The economy is finally picking up, as is inflation. This supports the central bank’s intent to slow the pace of easing. We look for a 75 bp cut to 7.5% on October 25 followed by a 50 bp cut to 7% on December 6 that should effectively end the easing cycle.

Malaysia reports August IP Thursday, which is expected to rise 5.6% y/y vs. 6.1% in July. The economy remains fairly robust, but policymakers are likely to err on the side of cautions. CPI rose 3.7% y/y. Bank Negara does not have an explicit inflation target, and so can keep rates on hold for now. Next policy meeting is November 9, and no change is expected then.

South Africa reports August manufacturing production Thursday, which is expected to rise 0.1% y/y vs. -1.4% in July. The economy remains very weak, which is why we think the SARB will resume cutting rates at the November 23 meeting.

India reports September CPI and August IP Thursday. The RBI is looking for inflation to continue accelerating this year, which would justify its decision to remain on hold this month. The next policy meeting is December 6, and we do not expect any change then.

Peru central bank meets Thursday and is expected to keep rates steady at 3.5%. CPI rose 2.94% y/y in September, just within the 1-3% target range. The bank has been cutting rates at every other meeting since it started the easing cycle in May. As such, we look for the next 25 bp cut to 3.25% at the November 9 meeting.

Singapore reports August retail sales Thursday. Singapore then reports Q3 advance GDP Friday, which grew 2.9% y/y in Q2. The MAS holds its semiannual policy meeting on the same day. While the economy is picking up, we do not expect a change in policy then. However, there is a chance that the MAS changes its forward guidance to set up possible tightening in April.

Comments Off on Emerging Markets: Week Ahead Preview

September 1st, 2017

By Marc Chandler.

Yesterday US President Trump formally launched his campaign for tax reform. The Big Six (Mnuchin and Cohn for the administration, McConnell, and Hatch from the Senate and Ryan and Brady from the House) had been meeting and were to craft a reform bill.

Last week the Administration changed tactics and essentially withdrew from the process, leaving Brady, the Chair of the House Ways and Means Committee. Trump. Rather than a detailed plan that had been promised, Trump provided a few basic principles, like simplification (so that most Americans can file a return on one page), lower corporate tax schedule and an incentive to corporations to repatriate the earnings retained offshore.

The Administration has also indicated, it is interest no longer allow state and local income taxes to be deducted from the federal tax obligations. If it does materialize, it would be a significant impact for households, especially in high tax areas. Other deductions, like for mortgage interest, approved retirement savings (e.g., 401k), and charitable contributions will be retained.

Cohn recently suggested that the tax reform bill will be drafted over the next 4-5 weeks. This seems quite ambitious given the difficult issues for which the Big Six apparently made little substantive progress. Moreover, September is a “short month” for Congress, and there at least two more pressing issues; namely the debt ceiling and spending authorization.

One would think that with a Republican majority in Congress and the White House, that there should be no question of default (debt ceiling) or government shutdown (spending authorization). However, the majority is in name only. We have argued that the fissures within the Republican Party may be greater than some inter-party differences.

The same split, represented by the Freedom Caucus, on the one hand, and the more moderate Tuesday Group on the other, which prevented health care reform, appears to be frustrating Mnuchin’s desire for a clean increase in the debt ceiling. The Freedom Caucus, or at least some of its members, are seeking concessions in the form of extra spending cuts in exchange for lifting the debt ceiling. Recently President Trump threatened to allow the government to shut if Congress does not authorize spending for the controversial wall on the border with Mexico.

There is a new wrinkle in this that investors will want to monitor going forward. A couple of weeks ago (August 17) rumors that Cohn was considering resigning from his post as the Administration’s National Economic Council over the President’s handling of the violence in Charlottesville, the equity market swooned. Cohn was seen as a moderate voice representing business interests. He did not resign, though admitted to thinking about it. In any event, there are reports that there has been a falling out with the President. Yesterday, although Cohn was with the President on the trip to Missouri where Trump gave his pep talk on taxes, Trump neglected to thank him for his work on taxes. Everyone else traveling with Trump was identified and thanked by name, including Ivanka, his daughter, and senior adviser.

Although we would not make a big deal of Cohn not being mentioned by name, many are scratching their heads. Trump has been publicly vocal in criticism of cabinet members, like Sessions and Tillerson. However, there are a few strikes against Cohn. First, was Cohn’s public criticism of the President and his call for a higher standard. A week later Trump pardoned former Sheriff Arpaio who was found guilty of contempt of court for racially profiling. There is some talk that Arpaio is considering running against Senator Flake, a Republican Senator who has been critical of Trump.

Second, the market response to rumors of Cohn’s resignation overshadowed Trump, which is not acceptable, it seems. Third, Cohn did not deliver a detailed tax plan, and this appears to have forced Trump to adjust his strategy. He has already complained about the “do nothing Congress, ” and this could be the rallying cry of a slate of Trump candidates that could challenge the sitting Republicans in next year’s primaries.

There is another implication as well. Cohn has long been rumored to be the most likely successor to Yellen at the head of the Federal Reserve. When asked about it recently, NY Fed President and previously at Goldman, Dudley said Cohn was a reasonable candidate. Some journalists called this an endorsement. It did not seem like that. Dudley was asked and did not volunteer the assessment. And this is as neutral of an answer that one can imagine. It was not an endorsement, but an acknowledgment. Anything else would have put the NY Fed President in an awkward position. In what appears to be the consensus narrative, former employees of Goldman Sachs are some homogeneous group, but what has been brought into relief in the first part of Trump’s presidency is that there are stark differences among this cohort, and not that Bannon, for example, also worked at Goldman.

Some thought that Yellen’s speech at Jackson Hole mostly devoted to defending the regulatory regime that has emerged since the Great Financial Crisis was her way of acknowledging she was not going to be reappointed as Fed Chair. This may not be a formidable obstacle. Many financial institutions seem to want some modification of parts of Dodd-Frank, but few seem to want to return to status quo ante. We note that currently, PredictIt shows Cohn and Yellen in a dead heat.

http://www.marctomarket.com/

Comments Off on US Tax Reform and the Fed

August 16th, 2017

By Marc Chandler.

The North American Free Trade Agreement is more than 20 years old and should be updated. This has been clear for several years. It was anticipated that the upgrade would be part of the Trans-Pacific Partnership, which had entered its final stages of negotiations before President Trump pulled the US out of the effort that it had previously sponsored as part of the pivot to Asia.

Trump is no fan of NAFTA, and it seemed that he was prepared to pull out of it as well. However, he apparently was persuaded, some say by Canada’s Prime Minister Trudeau, not to abandon the agreement. The new negotiations will begin tomorrow. The US and Mexico are particularly eager for a fairly quick resolution. Mexico holds elections in the middle of next year, and although the US mid-term election in not until November 2018, there is concern that trade could be an issue in the primaries. In addition, it is thought that the White House would like a success in what has otherwise proved to be a lot of thunder with little rain.

The US runs a trade deficit with both Canada and Mexico. However, it does not appear to be a generalized lack of US competitiveness, as some suggest. Nor does it appear to be a function of some macroeconomic imbalance. The proper level of analysis is industry specific. If it weren’t for auto and auto parts, the US would run a trade surplus with Mexico. If it weren’t for energy, the US would record a trade surplus with Canada.

The US seeks to address the auto trade deficit with Mexico by adjusting the rules of origin. The US will also try to grow its own exports in agriculture, telecom, internet-based transactions. There is a large discrepancy in labor relations in Mexico compared with the US and Canada. The initial agreement included a sidebar on labor rights, but was never formally integrated. Mexico has a weak legal environment for workers and a large informal economy. The concessions Mexico made in the TPP negotiations may serve as a starting line, according to some press reports, but it is a low bar. The TPP agreement was simply to enforce domestic labor laws.

Addressing Canada’s bilateral surplus will also prove difficult. Canada has long been exempt from the previous ban on US oil exports. There was a period earlier this year that China imported more US oil than Canada. The US Commerce Department has recently escalated longer-term simmering disputes over lumber and dairy. It was hoped that the lumber dispute could be resolved before the NAFTA negotiations, but this has not been the case.

The Trump Administration’s trade strategy was part of a broader agenda that included tax reform at home. To the extent that globalization has come to mean offshoring and extensive supply chains, Trump argued that it hurt America. To address this, he flirted with a border tax, that was pushed by the Republican leadership in the House, until being dropped last month. Corporate tax cuts were also advocated to create disincentives to offshore production. Mexico, and to a less extent, Canada are not eager to alter the extensive supply chains. The global supply chains, after all, were an important part of the economic development experienced in Mexico and Asia in the last quarter of a century.

The negotiations will begin off fairly easily and smoothly. The initial issues will be largely administrative: meetings’ agendas, the number of negotiating groups, and the process that leads to the compilation of a new agreement. Later in the negotiations more difficult issues will be addressed, and of courses, the thorniest is not resolved if at all until the very end.

The Trump Administration wants to include in the new agreement guidelines on currency market manipulation. The Bank of Canada is now and traditionally one of the most laissez faire central banks when it comes to exchange rates. Mexico is more interventionist, but as the currency tends to depreciate over time, its intervention is mostly to strengthen the currency. This is what happened recently.

Trump’s campaign rhetoric helped fuel sharp peso losses, and the central bank responded by changing its intervention tactics to the husband is reserves and raised interest rates to address the inflation fed through from currency depreciation. The function of the clause may be more about setting a precedent, but the US needs to tread carefully because it could find that such a clause hampers its degrees of freedom in the future.

One of the most difficult issues with the new NAFTA negotiations is the Chapter 19 dispute resolution mechanism. Simply put, the rulings often go against the US, and it is not surprising that the Trump Administration wants to scrap them. However, Canada, and to a lesser extent Mexico, find protection against the US, which is of course so much larger than Canada or Mexico. Indeed, Canada appears to have made this a critical issue. Thiswarns of the risk of protracted negotiations, and possible brinkmanship tactics. NAFTA may not be loved by any of the participants, but there would be no winners if the NAFTA were to collapse.

Comments Off on NAFTA: Rock, Paper, Scissors

August 4th, 2017

By Marc Chandler.

The US reports the monthly jobs data tomorrow. The unemployment rate stood at 4.4% in June, after finishing last year at 4.7%. At the end of 2015 was 5.0%. Some economists expect the unemployment rate to have slipped to 4.3% in July.

Recall that this measure (U-3) of unemployment counts those who do not have a job but are looking for one. There are several other measures, and which one is right depends on what question one is answering.

A more comprehensive measure includes not only those looking for employment but also those that take part-time jobs because they cannot find full-time work (U-6). It includes people that are said to be “marginally attached” to the labor forces, which includes those that are not working or looking for work, but affirm that want to work and have looked a job in the past year. This measure of unemployment stood at 8.6% in June after finishing last year at 9.2% and 2015 just below 10%.

Discussions of what has happened to unemployment since the Great Financial Crisis tend to focus on the drop in the participation rate and age-related issues. The changing composition of the workforce, with Baby Boomers retiring and new hires, are unable to command comparable salaries, which in turn weighs on aggregate wage measures.

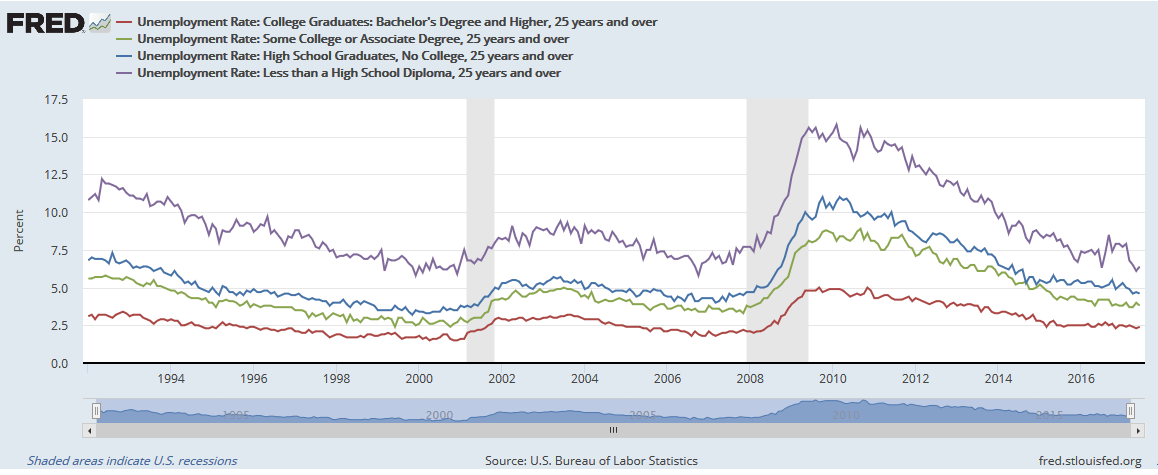

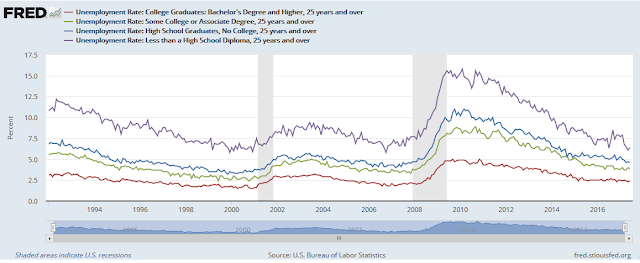

Another way the labor force can be looked at is by education level. That is what the

Great Graphic, from the St. Louis Fed shows. There are four educational cohorts tracked for people at least 25 years old. From top to bottom they are no high school degree (purple); high school graduate but no college (blue); some college or Associate Degree (green), college graduates with a Bachelor’s Degree or more (red).

The chart goes back a quarter of a century. The broad pattern remains the same. The more education, the lower the unemployment rate, not just now but consistently over the period under review. In June, those who graduated college had a 2.4% unemployment rate, or to say the same thing, looking at the glass as more full, 97.6% of those who graduated college are either working or looking for work. People who have some college, up to the Associate’s Degree had a 3.8% unemployment rate in June. People with a high school diploma had a 4.6% unemployment rate. The narrowness of the gap between high school graduates and some college is also noteworthy. Those without a high school degree have a 6.4% unemployment rate.

The Trump Administration is proposing a dramatic change in US immigration policies. It is not only illegal immigration that is incurring official wrath, but a 50% cut in legal immigration and a focus on skill-based criteria is advocated. In the context of this discussion, the share of immigrants who arrived with college degrees has nearly doubled to almost 50% from the 1986-1990 period. What this means is that in some states, immigrants have a higher level of educational attainment than the native population. According to the Economist, most states have gained college-educated immigrants between 2010 and 2015, and immigrants are more educated than Americans in just over half the states.

http://www.marctomarket.com/

Comments Off on Great Graphic: Unemployment by Education Level

July 31st, 2017

The tide of sentiment has turned against the dollar. The enthusiasm seen in the second part of last year, when the real broad trade weighted dollar rose in seven of the last eight months have been put into reverse. This measure of the dollar is set to record its seventh consecutive monthly decline this year, among the longest such runs in the modern era.

The tide against the dollar is both political and economic. At the start of this year, many feared the populist-nationalist wave which was seen as on its way to Europe after sweeping the UK out of the EU and Trump into the White House. As we anticipated, Europe has turned back the populist threat at every opportunity. The political anxiety has been deflected back to the US, where distractions, inexperience, and/or incompetence have frustrated the legislative process despite one party enjoying a majority in both houses of the legislative branch and control of the executive branch. Also, with a UK snap election, after repeated denials, and an unexpected outcome, UK politics is anything but settled, as the Brexit countdown continues.

Leaving aside the filibuster rules that require 60 votes to proceed, the Republicans failed to marshall a simple majority to repeal and replace the national health care system, despite several years of critiquing it. The health care reform was initially also intended to help fund tax reform. Nearly $1 trillion was expected to have been saved. Last week saw the House leadership finally drop its insistence of a Border Adjustment Tax (BAT). The controversial tax was supposed to free up another trillion dollars to fund tax reform. With those two pieces gone, the prospect of tax reform diminishes.

Tax cuts are still possible, but if by CBO’s reckoning that the tax cuts will increase the debt level in a decade, then a 60-vote majority is needed. The Bush Administration’s work around was to make the tax cuts temporary. When those tax cuts expired, the country contended with a “fiscal cliff” and what felt like tax increases.

Still, it is not clear that the current leadership can bridge the chasm between its conservative and moderate-wings to agree to cut taxes. The basis for an agreement would likely mean that the tax cuts are fiscally neutral, which in turn could limit the stimulative impact. Moreover, without tax reform, the tax holiday to encourage repatriation of earnings held offshore would simply keep the cycle going, whereby mostly the same industries accumulate earnings offshore and wait for the inevitable break. By seeking to tax some of those earnings, Ireland has added pressure to reform the US approach to corporate taxes.

This leaves the US economy expanding around trend (~1.8%). The labor market continues to improve as the job creation has accelerated after a slow start to the year. Productivity growth is weak, and apparently without an immediate solution, and labor costs increases are also subdued. This was underscored by the disappointing 0.5% increase in the Q2 Employment Cost Index, released before the weekend. The expected 0.3% rise in average hourly earnings will not be sufficient to avoid the year-over-year pace slipping back to 2.4%, the lower end of a two-year range. The last time it was weaker was in September 2015.

Barring a significant upside surprise, the jobs report is unlikely to increase the risk of a September hike by the Fed or spur sharp backing up of long-term rates. Given the poor sentiment and interest rate backdrop, the dollar may struggle to sustain more than shallow bounces.

Similarly, news from the eurozone is unlikely to dampen expectations that the ECB will announce in September plans to scale back its asset purchases starting next year. Many investors have concluded that the ECB expanding its balance sheet around 180 bln euros in H1 18 (vs. 360 bln euros in H2 17) is somehow more supportive of the currency than the Fed likely shrinking its balance sheet $150 in H1 18. It does bring forward the day that the ECB may begin raising rates, but remember, it is beginning with its deposit rate at minus 40 bp. If it is hiked to minus 20 bp in H2 18, is that really a tightening? And isn’t it reasonable to expect the Fed to hike before this happens?

This week’s eurozone data include PMI (Spain and Italy are the focus since the flash), Q2 GDP (0.6%-0.7%, after 0.6% in Q1), unemployment (tick down to 9.2%, more than twice the US rate). At the start of the week, investors will see the first estimate of July CPI. Both the headline and core rates are unexpected to be unchanged at 1.3% and 1.1% respectively. Even a slightly disappointing inflation report is unlikely to impact expectations for ECB tapering.

Two central banks hold policy making meeting, the Reserve Bank of Australia and the Bank of England. The RBA is expressing no sense of urgency to change the cash rate from 1.5%. Governor Lowe recently noted that a weaker currency would be more helpful, but this is a low-level protest and one the market’s duly shrugged-off. Speculators have been drawn to the Aussie, which for the sixteen sessions beginning July 7, has only declined four times.

The Bank of England also most likely will stand pat. The vote may attract interest. One of the three dissenters at the last meeting (Forbes) term end and her replacement (Tenreyro) is widely expected to vote with the majority. However, there is some risk that Haldane votes with the hawks, which would leave the vote 5-3. Paradoxically, if Haldane does not vote for a hike, the quid pro quo may be a more hawkish quarterly inflation report, that is released at the same time as the MPC meeting concludes and the minutes are released.

Ahead of the BOE meeting, the July PMIs for construction, manufacturing, and service will be reported. Forward looking new orders and business expectations have softened, this batch of PMIs will likely suggest that the UK economy is gradually slowing, and the Bank of England is must recognize this in word and in their forecasts. After a slow H1 (Q1 02% and Q2 0.3% vs. 0.2% and 0.6% in Q1 16 and Q4 16), the economy is not expected to accelerate in H2. We suspect that the peak in UK inflation is within a month or two. The base effect of sterling’s sharp drop is eliminated from the year-over-year comparison, the pullback in energy prices, and softer consumption as the squeeze on real wages bite. The contest is between these forces and the patience of a majority of the MPC.

The main interest in Japan does not lay with its economic data, but with politics. First, the LDP, with a comfortable majority is an increasingly facing disenchanted citizenry. It lost the Tokyo election resoundingly, and the Abe government and the Prime Minister himself have been accused of abuse of power and favoritism. The allegations and scandals led to the Defense Minister’s resignation at the end of last week. This is a prelude of a large cabinet reshuffle in the coming days.

Domestic problems in Japan are not as bearish for the yen as may be intuitively assumed. Japan’s large net international investment position provides the wherewithal to repatriate savings back home. Also, to address his low level of support, Abe would not be the first politician to offer a shot of fiscal stimulus.

A second political issue emerged before the weekend. Due to a surge of imports of frozen beef, Japan announced, in apparent compliance with the WTO, have levied a surcharge on top of its customary tariff. Currently, US exports of frozen beef to Japan have a 38.5% tariff assigned. Under emergency rules, the tariff rises to 50%. The surcharge will remain in place through March and can be automatically imposed if imports surge by more than 17% year-over-year in any quarter. But wait, the plot thickens.

The US and Australia account for 9/10 of the Japanese market for imported frozen beef. Japan has a free-trade agreement with Australia, which is exempt from the surcharge. Its normal tariff is 27.5% and is to be reduced in stages, according to the agreement. Japan accounts for about a quarter of the international market for US frozen been exports. US cattle futures sold off when the news was initially announced.

The Trans-Pacific Partnership agreement would have addressed these issues. This may be one of the first tangible results of pulling out of the late-stage negotiations. Still, it is surprising that Abe did not intercede. The strategy that officials had intimated was to seek to avoid antagonizing an unknown, volatile, if not vitriolic partner. This goes does the opposite, and before Finance Minister Aso and Vice President Pence hold bilateral trade talks later this year. On the other hand, if the roughly $400 mln export issue dominates the agenda, then more substantive issues might not be discussed and thus strengthening the inertia that defends the status quo.

North Korea tested another intercontinental ballistic missile over the weekend. Some reports suggest that this second test this month suggests the capability to hit the midwest of the US, though there seems to be some disagreement. The US appears to have responded by testing its missile defense system in Alaska and flew to supersonic bombers over South Korea. Tensions remain high, but investors do not appear alarmed. The Korean won is the strongest currency in Asia this month, appreciating nearly 2% against the US dollar. Korean shares have underperformed, with the Kospi up about 0.4% in July while the MSCI Asia Pacific Index has rallied about 3.3% and a nearly 5. 2% gain in the MSCI Emerging Market equity index this month.

Lastly, we turn to Canada, where the positive news stream has sent the Canadian dollar to levels not seen in a couple of years (above $0.80). The surge in May’s GDP (0.6% for a 4.6% year-over-year pace) reinforces ideas that the Bank of Canada will take back the other cut that it provided for support in 2015, having taken the first back earlier this month. Canada reports June trade balance and July employment at the end of next week.

Employment surged in June, and a more subdued pace is expected (~10k). Growth differentials and the terms of trade warn of downside risks of Canada’s trade balance. Widening of trade deficit may not be negative for the Canadian dollar because it would increase the likelihood of a hike in Q4 (October?). Extrapolating for the OIS, there appears to be a little more than a 50% chance of a hike discounted. Since the day before the July 12 rate hike, the December the implied yield of the December BA futures have risen by 14 bp to 1.51%, which is where it finished last week.

Comments Off on The Dollar may Need more than a Strong Employment Report

June 19th, 2017

By Marc Candler.

(from my colleague Dr. Win Thin)

EM FX was mixed Friday to cap off a mostly lower week. Obviously, we’re seeing a bit of a washout in EM after the hawkish FOMC. Market was overly complacent and very long EM going into the FOMC meeting. The big question is how deep this selloff gets. For the better part of this year, EM dips have been met with renewed buying. We remain cautious on EM and think that investors should avoid the high beta currencies like ZAR, TRY, BRL, MXN.

Taiwan reports May export orders Tuesday, which are expected to rise 7.6% y/y vs. 7.4% in April. The central bank meets Thursday and is expected to keep rates steady at 1.375%. Taiwan reports May IP Friday, which is expected to rise 1.4% y/y vs. -0.6% in April.

South Africa reports Q1 current account data Tuesday. The deficit is expected to widen to -1.8% of GDP from -1.7% in Q4. It then reports May CPI Wednesday, which is expected to remain steady at 5.3% y/y. This would remain within the 3-6% target range. SARB next meets July 20, and rates are expected to be kept steady at 7.0%.

Hungary central bank meets Tuesday and is expected to keep rates steady at 0.9%. However, it may add stimulus via unconventional measures to offset recent forint strength.

Poland reports May industrial and construction output, PPI, and real retail sales Tuesday. Consensus y/y readings are 8.3%, 12.6%, 2.9%, and 7.6% y/y, respectively. The central bank releases its minutes Thursday.

Russia reports May real retail sales Tuesday, which are expected to rise 0.5% y/y vs. flat in April. The central bank cut rates 25 bp to 9.0% on Friday, and signaled further cautious easing in H2. More important for Russian growth is the price of oil.

Malaysia reports May CPI Wednesday, which is expected to rise 4.1% y/y vs. 4.4% in April. The central bank does not have an explicit inflation target. Next policy meeting is July 13, rates are expected to be kept steady at 3.0%.

Argentina reports Q1 GDP Wednesday, which is expected to grow 0.2% y/y vs. -2.1% in Q4. If so, this would be the first positive reading since Q1 2016. The fundamentals are slowly improving, with CPI inflation easing to 24% y/y in May from the peak of 27.5% in April.

Philippines central bank meets Thursday and is expected to keep rates steady at 3.0%. CPI rose 3.1% y/y in May, close to the 3% target and well within the 2-4% target range. We see steady rates for now, but the bank has signaled a more hawkish stance if price pressures rise.

Brazil central bank releases its quarterly inflation report Thursday. Brazil reports mid-June IPCA inflation Friday, which is expected to rise 3.48% y/y vs. 3.77% in mid-May. Petrobras just announced cuts to gas and diesel fuel prices, so price pressures are likely to move lower. COPOM next meets July 26, and a 75 bp cut to 9.5% is expected.

Mexico reports mid-June CPI Thursday, which is expected to rise 6.25% y/y vs. 6.17% in mid-May. This would be the highest rate since January 2009 and further above the 2-4% target range. Banco de Mexico meets that day and is expected to hike rates 25 bp to 7.0%. With the peso firming and inflation showing signs of topping out, this is likely to be the last hike in the cycle.

Singapore reports May CPI Friday, which is expected to rise 1.3% y/y vs. 0.4% in April. It also reports May IP that day, which is expected to rise 6.8% y/y vs. 6.7% in April. Despite firmer data, the MAS opted to keep its forward guidance intact at its April meeting, which suggests no move at the October meeting.

http://www.marctomarket.com/

Comments Off on Emerging Markets Preview: Week Ahead

June 14th, 2017

The US dollar is trading within its pre-weekend range against the major currencies as participants await the central bank meeting starting in the middle of the week. The Federal Reserve, Bank of England, and the Bank of Japan meet. Only the Fed is expected to hike rates, but given the disappointing growth and softening of the preferred core PCE deflator (February through April), there is talk of a dovish hike.

Meanwhile, politics is front and central. UK Prime Minister May announced a cabinet reshuffle over the weekend that gave two of her former rivals (Gove and Leadsom) join the cabinet, while she lost two of her close advisers. She faces the backbenchers in Parliament today. There is great uncertainty whether May survives as Prime Minister, but it is not clear either who would replace her and if they have greater support about the Tory base. Brexit negotiation was to begin shortly, and it is not clear if they will go forward and if and how the newly chastened government’s position will be modified.

In France, Macron’s new party (Republic on the Move) appears to have won a little more than 31% of the vote, suggesting that in the second round it can secure 415-455 seats in the 577-seat parliament. It polled about 10% more than the center-right Republicans, the party from which the Prime Minister hails. The Socialists were decimated. It will likely see the number of seats it controls fall to 20-30 from 331. Marring the results a little was the extremely low turnout. Nevertheless, Macron efforts to reshape French politics and economics took a step forward. His signature program is labor market reforms, which seek to break the tradition of industry-wide settlements, will go full steam ahead. Macron wants the measures ready before the end of the quarter.

There were two political surprises over the weekend. First, Italy had local elections in around 1000 cities in the last flurry ahead of the national elections, which must be held by next spring. There had been some movement toward elections later this year, but the political compromise between the four largest parties unraveled last week. Hobbled by internal strife, the Five Start Movement (M5S) did particularly poorly, leaving it in a weak position to compete in the second round on June 25. Investors responded positively to the electoral developments. Italy’s 10-year bond yield is off six-seven basis points to bring the one week decline to 25 bp, and near 2%, it is near the lows for the year. Its premium over Germany has narrowed 20 bp over the past week. The premium over Spain has narrowed 10 bp at the same time.

Italian shares are off around 0.3% in late morning turnover in Milan. It is faring better than most European equity markets today. The Dow Jones Stoxx 600 is off twice as much, led by information technology sectors that were hard-hit in the US before the weekend. Italian bank shares, however, are off 0.8%, for the second consecutive declining session. Italian large banks are considering injecting cash into two troubled regional banks which would allow a precautionary recapitalization. This would prevent having to bail-in equity investors and junior creditors. A decision is seen necessary by the middle of next week when a subordinated credit of one of the troubled banks comes due.

Separately, Italy’s economic news disappointed. April industrial output fell 0.4%, snapped a two-month advance, and defying expectations for a 0.2% increase. There was hope that the Italian economy was finally catching gaining some traction. Growth in Q1 was the best since Q4 2010, but it was flattered by inventory accumulation. Business and consumer confidence softened in May.

Finland is also facing a political challenge. A new head of the Finn’s Party threatens to undermine the fragile coalition under Prime Minister Sipila. A more outspokenly, anti-immigration, anti-EU, socially conservative-wing of the party gained control. A cabinet meeting is to be held today to determine if the current coalition can continue or if a replacement is needed. Finland’s 10-year yield is up a little, despite the decline in the other benchmark bonds in Europe. Finnish equities are off around 1%.

The MSCI Asia-Pacific Index also was dragged lower by the technology sector after the losses in the US before the weekend. It was off almost 0.3%, its third consecutive losing session, the longest losing streak in a month. Losses in the region were led by information technology and/or telecoms. Japan reported softer than expected April machine orders (-3.1% compared with median expectations for 0.5% gain). It not only snapped a two-month advance, but it offset it (February rose 1.5% and March 1.4%). Despite the softer Japanese data and steady-to-firmer US yields, the dollar continues to trade heavily against the yen, perhaps amid falling equity prices. It is straddling the JPY110 level after having run out of steam before the weekend near JPY110.80.

The euro extended the late recovery in the North America before the weekend into Asia and European activity today. New bids seemed to dry up as the euro approached $1.1230. Recently, it was turned lower after testing the $1.1285 area (ahead of $1.13) repeatedly. Still, despite the setback, it has not closed below the 20-day moving average (now ~$1.1205) since April 17. Sterling traded near $1.2770 in late Asia but found sellers in early European hours, pushing it back toward the lows, a little above $1.2700. The pre-weekend lows near $1.2635 seem to be inviting a retest.

What promises to be an important week for the US is beginning slowly. The highlight is the FOMC meeting where a rate hike is widely expected, and nearly fully discounted. The US also reports producer and consumer price inflation, industrial output and retail sales. The investigation into Russia’s attempt to influence the US election will hear from US Attorney General Sessions tomorrow.

http://www.marctomarket.com/

Comments Off on Ahead of Central Bank Meetings, Politics Dominates

May 26th, 2017

By Marc Chandler.

It is not just the fear that the investigations into Russia’s attempt to influence the US election willdistract from the Trump Administration’s economic program. It is also that the economic agenda itself seems is less clear.

That China was not cited as a currency manipulator is no major surprise. Bush and Obama also made the threat on the campaign trail over jettison it when the were in office. China has not been cited since 1994. Although we argue the designation is not as onerous as it is frequently made to be, lack of use appears to have increased its symbolic importance.

During the campaign and as recently as a fortnight ago, President Trump was talking about his willingness to address to “too big to fail” problem in the US financial sector. There was explicit support for some kind of new Glass-Steagall which forced a separation between deposit-taking institutions and investment banks. However, in recent testimony before the Senate, Mnuchin played this down and denied a commitment to support a “full separation” of commercial and investment banks.

There was much debate in the primaries a year ago about how fast the US economy can grow. Trump has talked about 5% and sometimes 4%. The budget presented assumes 3% growth. The Federal Reserve estimates that trend growth in the US is a little below 2.0%. Obama was the first President since the end of WWII that did not record a single year of growth above 3.0%. The last year that such growth was reported was 2005, and the last four-quarter period that averaged at least 3% was mid-2006.

Fed Chair Yellen recognizes that some supply-side reforms can boost growth potential. However, in the long run, growth is a function of hours worked and productivity. Slower growth of the pool of available workers and weak productivity growth limits the growth potential of the economy. There appears to be little thought given to boosting productivity, though the right kind of infrastructure investment can help.

Judging from the budget proposal, the Administration seems to be banking on boosting the labor force by making draconian cuts in the social safety net. As if fewer life choices, greater susceptibility to illnesses, experience greater hardships, and reduced longevity is not a sufficient disincentive of poverty, the budget proposals won’t raise the cost of being poor.

Mnuchin previously said that high income earners would not be beneficiaries of tax reform. This has become known as the “Mnuchin Rule,” which appears to have been repealed. The Treasury Secretary softened his commitment by saying that the necessary compromises with Congress may violate his rule. This seems disingenuous, as the budget proposals, first for the remainder of this year, and then for next year that came from the White House, before Congress even touched it, seemed to contradict the rule.

El-Erian has argued that the problem is the sequencing of the President’s economic agenda. He says the health care out not to have been the starting point. Yet that seems to be politically naive. Given the desire to exploit the Republican majority in both houses of Congress, then getting rid of the Affordable Care Act, which the GOP had harangued against for years, must be the centerpiece. This has to do with repealing the tax cuts associated with the ACA that would free up funds to pay for broader tax reform, in a way that can be achieved through the reconciliation process of the legislative branch.

Moreover, when Trump was elected, the US was near full employment, the Fed’s inflation target and trend growth. Many economists argued that economic stimulus risks accelerating inflation and forcing the Fed to move faster. Simply put, health care reform was needed to tax reform.

However, the CBO says that rather than free up $1 trillion that was initially expected, the House version of the healthcare reform would only save $119 bln over a decade. Also, the White House has become less sympathetic to the House’s border adjustment tax, which was to raise another $1 trillion that could have been used for tax reform.

Some observers argued that the rally in US stocks (exemplified by the Nov 2016-Feb 2017 10% rally in the S&P 500) was in anticipation of Trump’s three-prong economic strategy of deregulation, tax reform, and stimulus spending. If the economic program is challenged by distraction and incoherence, then why, they ask, is the market making new highs? It seems that one of the factors that make equities appear attractive, despite arguably stretched valuations, low interest rates. Low interest rates are not only an under-appreciated boost to many corporate earnings, but also makes the alternative to equities less attractive.

The uncertainty over the trajectory of US economic policy is likely to continue at least for the next several months. There is some hope that the Senate can do its version of health care reform before the summer recess. Ironically, Trump’s budget proposals assume the initial House health care bill ($150 mln deficit reduction). Mnuchin initially suggested tax reform could be complete by the August recess but has conceded that year-end may be more likely. And of course, this assumes that the political maelstrom is not a significant distraction from the economic agenda.

Comments Off on The Opaqueness of US Economic Policy

May 11th, 2017

Investors absorbed a few developments that might have been disruptive for the markets with little fanfare. North Korea’s ambassador to the UK warned that his country would go ahead with its sixth nuclear test, as South Korea elected a new president who wants to reduce tensions on the peninsula.

South Korea equities fell nearly 1% from record highs, while the MSCI Asia Pacific Index rose 0.2%. The Korean won fell 0.4% and is the weakest among emerging market currencies. The dollar has pulled back against the yen. Yesterday in the North American afternoon, the dollar was stretching through JPY114.30 when the news broke and pushed it back below the figure. The dollar held above JPY113.60 in Asia, and before Europe opened, it made an attempt to resurface above JPY114.00 but met new sellers. Recall last week; the dollar finished near JPY112.70. The price action may be best understood as consolidation, perhaps encouraged by the couple basis point pullback in the US 10-year yield.

President Trump fired the widely criticized director of the FBI yesterday. It is unusual for a president to fire the head of the FBI. The optics are horrible as the FBI was investigating the campaign’s ties to Russia. However, the impact the Administration’s economic agenda is minimal, and while the drama will continue to play out, it is a domestic political story. It still seems important to keep in mind that although Trump’s overall approval rating is low in relative and absolute terms, he continues to draw high levels of support from the Republican constituency.

The American Petroleum Institute estimated that US oil inventories fell for a fifth consecutive week, and the 5.8 mln barrel draw down was the most so far this year. Gasoline inventories rose (3.17 mln barrels) in line with the seasonal build, while distillates stocks fell 1.17 mln barrels. June light sweet crude oil stabilized and is holding above $46 a barrel. Recall that a month ago, the futures contract was near $54 a barrel and plunged to $44 at the start of this week. The bounce is muted and needs to rise above $48 to be of technical significance.

The EIA is expected to show oil inventories fell 2.1 mln barrels. Since the beginning of March, the EIA’s estimates of US oil stocks has alternated between builds and draw downs. The anticipated draw down would keep the pattern intact. On the supply side, the EIA estimate of US output this year and next from forecasts made last month. Meanwhile, as the May 25 OPEC meeting approaches, there is talk about extending the output cuts not just until the end of the year but into next year as well.

The economic news has been largely limited today to China’s price gauges and Italy’s industrial output figures. China’s CPI ticked up to 1.1% from 0.9%; It was 2.1% at the end of last year. The subdued price pressures will give officials room to stimulate later this year if needed, and the 0.4% decline in the month-over-month measure of producer prices may warn that it may indeed be needed. PPI rose 6.4% year-over-year. The median in the Bloomberg survey expected a 6.7% increase after 7.6% in March. The moderation comes as commodity prices, such as iron ore, steel, and oil prices retreated. The government has used the better growth numbers to focus on the credit excesses and to tighten lending to the housing market. The Chinese yuan is flat. It is up almost 0.6% against the dollar this year, and for the fourth month, it is in narrow ranges.

It has not often been when it can be said, but Italy reported a larger than expected rise in March industrial output. The 0.4% increase builds on the 1.0% rise in February. On a workday adjusted basis, Italian industrial output rose 2.8% compared with the 2.0% pace seen in February. Next week Italy will report Q1 GDP. It is expected to rise 0.2%, the same as in Q4 16.

European shares have been unable to match the minor strength seen in Asia. The Dow Jones Stoxx 600 is off about 0.2%, led by industrials and telecoms. Energy and utilities are posting small gains. Energy relates to the firmer oil story, while the rise the utility sector may have been helped by the decline in bond yields.

The Dollar Index gapped lower in response to the first round of the French election. That gap was closed yesterday and the Dollar Index in the upper half of yesterday’s range. If it can hold on to the recent gains, the five-day moving average can cross back above the 20-day for the first time in a nearly a month. A similar gap in the euro, however, has not been filled. The gap is found between $1.0738 and $1.0821. The 20-day average is found near $1.0830, and the euro has not closed below that average since April 17. The 200-day average is also at $1.0830.

Sterling remains firm but continues to encounter selling pressures in front of $1.30. Initial support is seen near $1.29. The Bank of England meets tomorrow. Although no change in policy is warranted, the MPC may recognize the continued resilience of the economy, and reiterate its patience with an overshoot of inflation is not boundless, which could see another attempt on the $1.3000-$1.3055 objectives. Forbes who dissented at the last meeting, in favor of an immediate hike, is likely to dissent again. It is unlikely that she convinced any of her colleagues, and if she did, that could also see sterling spike higher.

Dollar-bloc currencies are consolidating. The Australian dollar’s losses were extended yesterday on the back of soft retail sales. The government’s budget proposals showed a wider than expected deficit, but many focused on the new tax on banks. The Australian equity market rose 0.6%, and although financial stocks gained (0.2%), bank shares remained under pressures. The US dollar recorded a key reversal against the Canadian dollar at the end of last week, but so far this week, it has traded within last Friday’s trading range. It continues to straddle the CAD1.37 area. Recall that speculators in the futures market had a record large gross short Canadian dollar position as of a week ago.

Today’s US calendar features the import and export prices ahead of tomorrow’s PPI report. Friday sees the more important CPI and retail sales. The Fed’s Rosengren and Kashkari speak today. Dudley speaks tomorrow. The Canadian calendar is light today and sees March house prices tomorrow.

For More on Marc Chandler please visit click here

Comments Off on Markets Adjust to North Korean Threat, Fifth Fall in US Oil Inventories and Trump Drama

April 29th, 2017

Marc Chandler.

Equity markets are stalling into the end of the month. MSCI Asia-Pacific Index is snapping a six-day advance, and the week’s gain was sufficient to extend the advancing streak for the fourth consecutive month. The Dow Jones Stoxx 600 is trading off for the second consecutive session, after rallying for six consecutive sessions. Its 2.4% rally this week ensures a higher close for the month. This European benchmark has risen for three consecutive months and five of the past six. The S&P 500 has gained 1.1% so far this month, coming into today’s session. Last month the S&P 500 slipped 0.4%, which broke a three-month advance.

Bonds also rallied this month. The US 10-year yield is off 12 bp, with Gilts off 10 bp, and the Bund yield down six bp. On the month, French premium narrowed about four basis points. The 10-year JGB yield slipped almost five basis points to almost zero. Italy is the only major bond market to see rising yields. Fitch downgraded Italy last week (to BBB). Note that the PD has an open primary this weekend. Renzi is expected to win, after the left-wing and some old guard broke away from the PD.

The US dollar is mixed on the day. On the month, the dollar has risen against most currencies except, sterling and the euro (and the Danish krone). The dollar-bloc currencies fell out of favor this month, and are off around 2%. Sterling is the best performer, with the surprise election announcement a major prop.

The month-end and what for many in Europe and Asia will be a long holiday weekend with May Day celebrations and the bank holiday in the UK at the start of next week. Perhaps that could help explain the subdued market reaction to a series of economic reports.

The main exception to this generalization is the eurozone preliminary April CPI. It was much stronger than expected. The headline rose to 1.9% from 1.5%, and the core rate jumped to 1.2% from 0.7%. The data appears to have been flattered by calendar effect of Easter, and trip packages, for example, are included in the core. It is the highest level since mid-2013. The CPI report followed news of a stronger gain in M3 than expected, and an improvement in lending to both households and non-financial businesses.

The euro rallied toward the week’s high, but since the sharply higher opening on Monday, after the first round of the French elections, the euro has chopped around same cent range of $1.0850-$1.0950. Recall the $1.0935 area corresponds to the 61.8% retracement of the euro’s decline since the US election last November. And $1.0980 is the 50% retracement objective of the decline from last year’s high near $1.1615. Large option strikes at $1.09 (1.8 bln euros) and $1.0950 (2.4 bln euros) roll-off later today.

Draghi was upbeat about the region’s growth, which he seemed to acknowledge was mostly based on survey data. He was less sanguine on inflation, and due to the distortions with the April CPI, the May figures will be awaited for a cleaner read. The next ECB meeting is on June 8, and new staff forecasts will be available.

However, as we have noted, it appears the survey data is running ahead of actual activity. This concern materialized today. France reported a 0.3% expansion in Q1 17, which was a little softer than expected, weighed down by a 0.7% decline in net exports and household spending that practically stagnated. That said, Q4 16 growth was revised higher.

The UK also disappointed. The economy expanded by 0.3% in Q1. It is the weakest growth in a year. Services grew by 0.3%, their poorest showing in nearly two years. Industrial output rose 0.3%, arguably helped by stronger exports and a weak pound. Manufacturing output rose 0.5%. Construction rose a more modest 0.2%. Separately, the UK reported that mortgage approvals and consumer credit growth slowed in March.

Sterling shrugged off the news and is making new highs since early last October. It approached $1.2960. The $1.30 area is of psychological importance, but chart-based resistance is seen in the $1.3050-$1.3070 area. It may require a break of $1.2860 on the downside to stymie the bulls.

Japan’s end of the month data dump shows many expect the BOJ to lag behind the ECB. March CPI was a touch softer than expected at 0.2%, and the core rate was steady at 0.2%. However, excluding food and energy, CPI slipped back into negative territory (-0.1% vs. 0.1%). Although retail sales ticked up in March (0.2%), overall household spending disappointed. It fell 1.3% year-over-year, which was more than twice the expected pace, though not as deep as the decline in February. Industrial output was also weaker than expected, falling 2.1% in March, which gives back more of February’s 3.2% gain than expected. The median expectation was for a 0.8% decline. Lastly, unemployment was unchanged at 2.8%, though the jobs-to-applicant ratio increase to 1.45 from 1.43.

The dollar is consolidating in narrow ranges against the Japanese yen. Today’s range is about a third of a yen above JPY111.00, and inside yesterday’s range, which was inside Wednesday’s range. The dollar has been resilient even though US 10-year Treasury yields are struggling to re-establish a foothold above 2.30%. Yen sales against sterling and the euro may have bolstered the greenback’s resilience.

The US reports Q1 GDP. The median forecast in the Bloomberg survey is for a 1.0% annualized gain. We suspect the risk is on the downside. Beginning in 2010, Q1 growth in the US has averaged 1.1%, but our back of the envelope calculation warns that Q1 17 was likely weaker than average. Outside of the headline shock, it has no implications for monetary policy. The Federal Reserve hiked rates in March, rendering Q1 data moot. The FOMC meets next week, and the statement is likely to look past the setback in Q1. The US jobs report at the end of next week may be of greater importance than the FOMC meeting.

The US also sees the Chicago PMI for April and the final University of Michigan consumer confidence and inflation expectation survey. It is important that the US Congress approves a spending authorization bill or some stop gap measure. Otherwise, government closure cannot be ruled out. Separately, although press reports suggest progress on health care, a resolution still seems elusive. To appease the wing of the Republican Party (Freedom Caucus) that blocked the previous attempt appears to be alienating the moderate wing (e.g. Tuesday Group).

Canada reports February GDP (expected to have risen by 0.1%). The weekend sees the EU summit on Brexit. Reports suggest the EU may press for considering a united Ireland within the EU. Merkel’s speech earlier this week underscores the EU’s interest in first agreeing to the terms of exit before a new, even if temporary, arrangement, can be made. Also, ASEAN countries hold a summit as well.

Comments Off on Markets Limp into Month End

March 14th, 2017

By Marc Chandler.

Hit by profit-taking ahead of the weekend, despite US jobs data that remove the last hurdle to another Fed hike this week, the greenback remains on the defensive. It has softened against all the major currencies and many of the emerging market currencies. The chief exception is those in eastern and central Europe.

Turkey and Dutch tensions rose over the weekend as the Dutch refused to the leftTurkey’s foreign minister to enter the country to campaign, took another minister to the border, earning the wrath of Turkey’s Erdogan. The Dutch go to polls Wednesday. The Rutte government is credited with handling the affair well, and although supporters for the Freedom Party, may have become more enthusiastic, the PVV does not appear to be growing its base. Overall, the market impact looks minor.

What will be the busiest week of the quarter, if not year, has begun off slowly. The main economy news was the Italian industrial output figures. They disappointed, and follow the poor French figures are the end of last week (-0.3% instead of the expected 0.5% gain). Italian output fell 2.3% in January after a 1.4% gain in December. The median estimate in the Bloomberg survey was for a 0.8% decline.

Last week’s ECB meeting gave investors the clear impression that the central bank recognizes that the downside risks have lessened in the region. No more rate cuts are anticipated, and greater attention is being given to the eventual exit from the unorthodox monetary policy. The sequencing of the exit between asset purchases and negative interest rates may take a different form than the exit by the Fed or the earlier exit by the BOE.

Still, we can’t help but wonder who leaked news that there was a discussion along these lines (reduced negative deposit rate before asset purchases are complete) and to what end. It seems those who are critical of the ECB’s course may have had the incentive to provide that information to the media. Of course, it is reasonable to expect a push back. It came from Belgium’s central banker Smets, who recognize the macro improvement, was clear that no decisions were taken.

Also, over the weekend, the head of the US administration’s strategic and policy committee, Schwarzman, told a CNN interviewer the confrontation with China that candidate Trump had seemed to emphasize, might not materialize after all. Treasury Secretary Mnuchin had already indicated that the normal Treasury review would take place before any judgment was made about China and its yuan policy. Chinese stocks, especially those that trade in Hong Kong, did well. The Hang Seng Enterprise Index rallied 1.8%, the most since November, and is now up 9.2% year-to-date. The MSCI Asia Pacific Index advanced 0.8%. The index has been down only two week’s this year for a 7.7% gain.

European shares began firmer but surrendered the early gains. The Dow Jones Stoxx 600 was fractionally lower in later morning turnover. Telecoms and energy led most sectors lower. Materials seemed to like the rebound in some industrial goods (iron ore, zinc, copper) and the second was up nearly 1%.