The former Fed chairman’s memoir helps explain why this economic recovery has been so disappointing.

News that the U.S. economy grew only 1.5% in the third quarter again raises the question: Why has the recovery from the recession been so historically weak?

Former Federal Reserve Chairman Ben Bernanke’s new book, “The Courage to Act,” amply illustrates how the failure to understand what caused the 2007-08 financial crisis ushered in policies that have slowed growth.

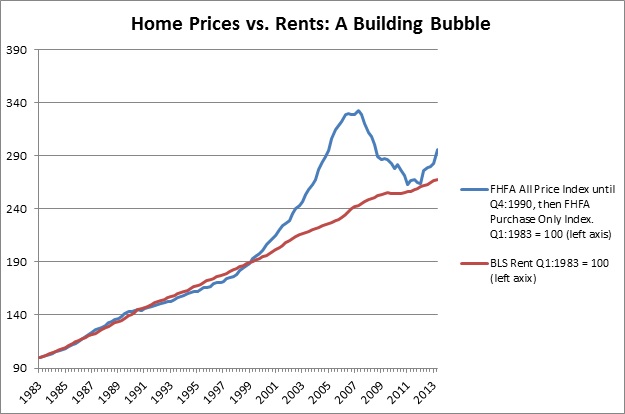

By the time he became Fed chairman in February 2006, Mr. Bernanke was aware that a large housing bubble was developing—by 2007 it had inflated to the largest in U.S. history—and that underwriting standards across the housing market were declining. Yet he apparently never tried to determine why these major shifts were occurring.

Because he didn’t investigate this issue, in March 2007 Mr. Bernanke famously told Congress that “the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.” When the crisis developed later that year, the only changes he could imagine that would prevent another crisis were, as he says in his book, “improved monitoring of the financial system and stronger financial regulation.”

Nowhere in the book does he mention or show any grasp of the true causes of the decline in underwriting standards: the federal government’s affordable-housing goals, which required Fannie Mae and Freddie Mac to meet annual quotas for mortgages made to borrowers at or below the median income. Nor does he mention that these goals had increased from 30% of all mortgages they acquired in 1992 to 56% of all they acquired in 2008, forcing Fannie and Freddie to loosen their standards further to reach the targets. Because they were the dominant players in the market, all underwriting standards deteriorated.

What little he knew about Fannie and Freddie appears to come straight from the left’s history of the financial crisis. He writes that from 2004-06, “anxious about competition posed by private-label [mortgage-backed securities], and eager for the high returns that lower quality mortgages seemed to promise, they bought and held private label MBS that included subprime and other low-quality mortgages.”

Yet by 2002 Fannie and Freddie had acquired $1.2 trillion in subprime and other weak mortgages. By the time he became Fed chairman, they’d racked up $3.4 trillion. By 2008, apparently unknown to the Fed or Mr. Bernanke, 31 million loans—more than half of all U.S. mortgages—were subprime or otherwise weak, and 76% of those sat on the books of government agencies, principally Fannie and Freddie. This shows, beyond question, where the demand for these subprime and risky loans originated.

So it came as no surprise, given his limited knowledge, that he and Hank Paulson, then-Treasury secretary, were, as Mr. Bernanke put it, “eager to focus Congress on the gaps in financial regulation” when they testified before the House Financial Services Committee in July 2008. After that, the Democratic-controlled Congress, working with the Obama administration, produced the overreaching Dodd-Frank Act, signed into law in 2010 and named after the two strongest congressional proponents of affordable-housing goals, former Rep. Barney Frank and Sen. Chris Dodd.

It is thanks to Dodd-Frank that the five-year growth rate has averaged about 2.2%. Dodd-Frank has had this effect primarily because of the new regulatory costs and lending standards it imposed on financial firms, particularly small banks. New regulations from the Consumer Financial Protection Bureau and other Dodd-Frank inventions have forced many small banks out of business, forced others to merge with larger competitors, and reduced the rate of new bank formation from an average of 100 a year before 2010 to only three afterward.

The regulations and restrictions on small banks have most acutely affected small businesses, particularly startups. Though most new employment in the U.S. economy comes from small business, entrepreneurial startups provide most small-business employment growth. A 2013 study published in the Review of Economics and Statistics shows that over time firms aged 0-5 years account for 20% of total job creation in the U.S.

This part of the economy has been hit hardest by Dodd-Frank rules that have driven up costs for small banks, reduced their number and applied large bank lending standards to the small outfits that have always met their communities’ needs with the flexible standards startups require.

A 2015 Goldman Sachsstudy shows that large firms—500 employees or more—have grown at a pace consistent with past recoveries, but small businesses have remained stagnant. The study concludes that, since Dodd-Frank, small businesses—which rely largely on small banks—have been unable to find the credit necessary for growth, while large firms have access to credit through the capital markets.

If Mr. Bernanke had used his academic skills and the Fed’s data to determine what actually caused the crisis, he might not have pushed Congress to fill “the gaps in financial regulation.” Had he advocated instead changing destructive housing policies, Dodd-Frank might never have happened and the economic recovery would have been far more robust.

The views expressed in this testimony are those of the author alone and do not necessarily represent those of the American Enterprise Institute.

Chairman Jeb Hensarling, Ranking Member Waters and members of the Committee:

I am grateful for the opportunity to testify before this committee on the question: “The Dodd-Frank Act Five Years Later: Are We More Prosperous?” My name is Peter Wallison. I am the Arthur F. Burns Fellow in Financial Market Studies at the American Enterprise Institute. My testimony is my own and does not necessarily represent the views of AEI.

I am particularly delighted to be seated here with Phil Gramm, not only the teacher of the chairman of this committee but to my mind the greatest political economist ever to sit in the US Senate. He is sorely missed by everyone who recognizes the need today for pro-growth economic and financial policies. To be sure, there are great advocates for these policies in Congress today, but the knowledge and clarity of expression of Senator Gramm was and is unique. Although I like to have the opportunity to speak once in a while when I testify before congressional committees, I would happily cede all of my time to Phil Gramm. In that way, not only will the members of this committee be educated, but so will I.

Dodd-Frank became a law on July 21, 2010, and this testimony will use that date as the reference point for determining the economic effects of the act. On whether we are more prosperous since July 21, 2010, it is important to understand that the question of prosperity or economic growth is relative. There has certainly been economic growth since July 21, 2010. In that sense, we are more prosperous, but as Senator Gramm said in his written testimony: “Had this recovery simply matched the strength of the average of the other ten recoveries since World War II, 14.4 million more Americans would be working today and the average income of every man, woman and child in the country would be $6,042 higher.”

Below is a chart, prepared by the Federal Reserve Bank of Dallas that encapsulates the point that Senator Gramm is making.

As the chart shows, through the first quarter of 2013, there had been some economic growth, but far less than in a normal recovery. Since then, as we know, things have not improved substantially. A recent op-ed in the Wall Street Journal by Glenn Hubbard (former chair of the Council of Economic Advisers under George W. Bush) and Kevin Warsh (a former Governor of the Federal Reserve) in effect updates this chart: “Economic growth in real terms is averaging a meager 2.2% annual rate in the 23 quarters since the recession’s trough in June 2009. The consensus forecast of about 1% growth for the first half of this year offers little solace.”

What’s the problem?

I believe that all the new regulation added by the Dodd-Frank Act in 2010 is the primary reason for the slow growth this country has experienced since 2010. Later in this testimony, I will show that the new regulations imposed on banks—particularly small banks—has created a bifurcated economy. Large firms in the real economy, which can access the capital markets for financing, have been growing roughly in line with previous recoveries, but smaller firms that rely on banks for financing are growing far more slowly. Since most of the growth in the US economy, and especially in employment, comes from small firms, the economy is underperforming and will continue to underperform until the treatment of banks under Dodd-Frank Act is substantially modified or repealed.

A Cost-Benefit Analysis of Dodd-Frank’s Additional Regulations on Banks

The relevant question about the efficacy of any new regulation such as the Dodd-Frank Act is always one of balancing costs and benefits. Regulation inevitably imposes costs, and placing additional costs on any business will virtually always reduce the system’s productivity and growth by diverting expenditures to regulatory compliance instead of greater production. In banking and finance, which rely heavily on human capital, it may be easier to measure at least one element of cost—the effect on hiring practices. If, in order to comply with a regulation, a bank has to hire a compliance officer rather than a loan officer, the bank will inevitably be less productive—it will make fewer loans for the same amount of revenue.

Looking simply at employment practices instead of other effects of regulation is a very simple idea, and it doesn’t fully reflect all the costs of additional regulation. As Greg Ip recently wrote in the Wall Street Journal, “[N]o one knows the true costs or benefits of the blizzard of laws, rules and penalties imposed since the financial crisis…Unlike the rules governing pollution and automobile safety, the costs and benefits of big new financial rules are seldom rigorously quantified… The costs of financial regulation go beyond what banks and their shareholders must pay for more compliance personnel. By making credit more expensive and restricting supply, new regulation can ding growth, especially at times like the recent past when the Fed can’t compensate by lowering interest rates, which are already near zero.”

Nevertheless, although we can’t put a number on all the costs of more regulation, at least for the banking industry we can say that hiring practices shaped by additional regulation may be one way to measure some of the costs of the new regulation that came with the Dodd-Frank Act. I will assume in the discussion that follows that all the new regulations that have been imposed on banks have required them to add compliance officers instead of loan officers, and that this was one major cost of the Dodd-Frank Act. It added costs, but reduced the amount of lending. The next question is measuring the benefit.

Giving Congress its due, in enacting Dodd-Frank Congress was trying to achieve financial stability in the future through stricter regulation of the financial system. In doing so, I believe Congress misdiagnosed the financial crisis as the result of lax regulation of the private financial sector. In effect, it treated the symptoms rather than the disease. The symptoms were the weakness of private financial institutions as unprecedented numbers of mortgages defaulted in 2007 and 2008, but the disease was the government’s housing policies, which—between 1992 and 2008—caused a drastic deterioration in residential mortgage underwriting standards. A single fact demonstrates the government’s role in weakening the financial system: in 2008 more than half of all mortgages in the US—31 million loans—were subprime or otherwise weak and risky. And of these 31 million mortgages, 76 percent were on the books of government agencies. This shows, without question, that the government created the demand for these low quality mortgages.

For purposes of this testimony, however, whether Congress was right or wrong in its diagnosis of the financial crisis is immaterial. Even if Congress was correct in its assessment of the causes of the crisis, we can evaluate whether the balance it struck between costs and benefits in the regulation of banks was correct. Here we can be reasonably sure that we know what benefit Congress was seeking. Because of its diagnosis of the crisis, Congress was seeking to create future stability in the financial system by imposing greater regulation on private sector financial firms, particularly banks. So the question is whether the stability Congress was hoping to achieve through additional regulation in Dodd-Frank outweighs the costs.

Before beginning this analysis, it is important to note that we cannot weigh all the costs of Dodd-Frank. We don’t have the capacity to do that at this point. When Jamie Dimon, the chair of JPMorgan Chase, asked Ben Bernanke in 2011 whether “anyone bothered to study the cumulative effect of all these things,” Bernanke replied, “I can’t pretend that anybody really has. You know, it’s just too complicated. We don’t really have the quantitative tools to do that.”

Nevertheless, the fact that we can’t quantify all the costs of Dodd-Frank does not mean that we can’t assess at least one of them, and that is the cost of hiring compliance officers instead of loan officers. Compliance officers are necessary to meet the regulatory demands of the government; loan officers are necessary to increase lending or to sustain it at previous levels. To the extent that banks have to hire compliance officers instead of loan officers, they are inevitably reducing the amount of lending they will do.

A good place to assess the cost-benefit question underlying Dodd-Frank is the act’s requirement that all bank holding companies with $50 billion in assets or more be considered systemically important financial institutions (SIFIs) and subjected to “stringent” regulation by the Fed. Among many other requirements, these banking organizations must also prepare living wills—detailing how they would be broken up if they fail—and participate in annual Fed-designed stress tests. These and other requirements add substantial additional costs to whatever “stringent” regulation entails. These substantial additional costs, even if only in the form of more compliance officers than loan officers, will mean that these banks will supply less credit to the real economy. If banks did not have to hire any compliance officers, all their new hires—if any—would be loan officers, which would generate more loans and hence more revenue and more economic growth for the real economy.

Do the benefits that Congress sought in imposing substantial new regulation on banking organizations with assets of $50 billion or more outweigh the costs? The benefit is added stability. With “stringent” regulation, stress tests and living wills, it is fair to assume that these banks will be less likely to fail in the future, and if they fail their failure will not be as disorderly as failures in the 2008 financial crisis. The cost is that these banking organizations will, through their subsidiary banks, be making less credit available to the real economy because they have been required to hire more compliance officers instead of loan officers.

The Federal Reserve’s Flow of Funds accounts tells us that as of the end of the first quarter of 2015 the total financial assets in the US were $86 trillion, and total assets of private depository institutions were $17 trillion. $50 billion is .3% of 17 trillion. So the drafters of the Dodd-Frank Act believed that a banking organization with .3% of the assets of the entire banking business would cause the financial system to become unstable if it failed. A bank with $200 billion in assets would have 1.2% of total bank assets. Even a bank with $500 billion in assets has only a little over 3% of all bank assets. It seems completely implausible that in an economy with $85 trillion in financial assets and a banking system with $17 trillion in assets the failure of a $50 billion banking organization—or even a $200 billion or $500 billion bank—would cause any significant instability. Losses, yes. Instability in the whole financial system, no.

So it seems that Congress struck the wrong cost-benefit balance between economic growth and stability when it decided that any banking organization with assets of $50 billion or more ought to be subjected to costly new regulations in the interest of assuring the future stability of the financial system. This new regulatory burden imposes a high cost in the form of much slower growth—especially, as we will see, for businesses dependent on banks—with very little benefit in the form of additional stability. Senator Gramm described the high cost relative to benefits in the statement from his testimony that I quoted above. In that case, which assumed that Dodd-Frank had not been adopted at all, the cost came in the form of a slower economic recovery since the end of the 2009 recession than the average recoveries of the past.

We don’t know how much additional growth we would have had if Dodd-Frank had drawn the SIFI line for banking organizations at the different place—say, at $500 billion or $1 trillion. Although we know that regulation has some cost, there is insufficient data available to draw any connection between a certain amount of new regulatory cost and a certain amount of reduced economic growth. But what we do know in the case of the special regulations imposed on banks with more than $50 billion in assets up to as much as $500 billion is that we have bought more stability than we need at the cost of reduced economic growth.

The same is true for small banks, which have also been required to address many new regulations coming out of Dodd-Frank, especially in mortgage lending, debit and credit card activity and consumer lending. There has actually been some solid academic work on how regulation affects the employment practices and profitability of community banks—those with assets of less than $50 million. In 2013, three economists at the Federal Reserve Bank of Minneapolis actually looked at the effect of new regulations on these small institutions. They chose to model only the effects on bank hiring, although many other factors—risk-taking, legal liability, product costs—are affected by additional regulation. “[W]e find,” they write, “that the median reduction in profitability for banks with less than $50 million is 14 basis points if they have to increase staff by one half of a person; the reduction is 45 basis points if they increase staffing by two employees. The former increase in staff leads an additional 6 percent of banks this size to become unprofitable, while the latter increase leads an additional 33 percent to become unprofitable.”

Although community banks with less than $50 million in assets are of course much smaller and simpler than banks with $50 billion in assets, the point is the same if we are talking about the effect of regulations on hiring practices. If a banking organization larger than $50 billion has to hire additional compliance officers in order to meet its new stringent regulation, living will and stress test requirements, its profitability will also be reduced, a certain number of those banking organizations will then become vulnerable to failure, and all of them will reduce the amount of credit they provide because relatively more of their human capital is engaged in compliance rather than sales.

In March, 2014, for example, JPMorgan Chase, the largest US banking organization, cut back its projections for the coming year, saying that its trading profits and return on equity would be down. It noted that it would also add 3000 new compliance employees, on top of the 7000 it added the year before. But the total number of employees of the banking organization were expected to fall by 5000 in the coming year. Absent the regulatory imperative, the bank might have cut 8000 employees instead of 5000, thus cutting its costs somewhat further, or it might have added 3000 new loan officers instead of compliance officers to increase its revenues. But with the regulatory imperative it faced, even a large banking organization that is experiencing a decline in profitability had to increase its hiring of compliance officials and cut employees from its profit-making activities. What we are seeing, then, is a clear case—even at the level of the largest banking organizations—of compliance costs substituted for the personnel that are normally the sources of revenue and profit.

Are There Other Explanations for the Slow Recovery?

Defenders of Dodd-Frank sometimes argue that a slow recovery is typical after financial crises, but recent scholarship casts doubt on this explanation. Michael Bordo and Joseph Haubrich studied 27 recession-recovery cycles since 1882 and concluded: “Our analysis of the data shows that steep expansions tend to follow deep contractions, though this depends heavily on when the recovery is measured. In contrast to much conventional wisdom, the stylized fact that deep contractions breed strong recoveries is particularly true when there is a financial crisis.” [emphasis added]

Bordo and Haubrich find only three exceptions to this pattern; in these cycles, the recoveries did not match the speed of the downturns. The three were the Depression of the 1930s, the 1990 recession that ended in March 1991, and the most recent recession, which ended in June 2009. What do these three exceptions have in common?

In each case, the government’s intervention in the financial system was unusual and extensive. During the Depression Era the Hoover and Roosevelt administrations tried many ways to arrest the slide in the economy, all without success. Hoover was an inveterate activist in all things, and Franklin Roosevelt believed in constant experimentation until something worked. Neither of them seemed to have a consistent theory about what brought on the economic downturn or how to address it. Under President Hoover, Congress passed the Smoot-Hawley Tariff Act, and the Emergency Relief and Reconstruction Act, and established the Reconstruction Finance Corporation. Under Roosevelt, the US went off the gold standard, established a deposit insurance system and a federal regulatory system for state-chartered banks; Congress adopted the National Recovery Act, the Emergency Banking Act, Emergency Farm Mortgage Act, the Securities Act, the Securities & Exchange Act and the Farm Credit Act. Other major laws with financial implications were the National Industrial Recovery Act and the Agriculture Adjustment Act (both of which were eventually declared unconstitutional by the Supreme Court). This enormous flurry of activity, however, while popular with the American people, did not produce a recovery until the nation geared up for war at the end of the 1930s.

In addition, the Pecora hearings of the early Roosevelt administration, propagated the idea that banks’ securities activities had caused the crisis; this is uncannily similar to the narrative that produced the Dodd-Frank Act, which blamed the financial crisis on insufficient regulation of the financial system and greed and recklessness on Wall Street. The Pecora hearings resulted in the Glass-Stegall Act, which separated securities and banking activities. Whether or not that was harmful can be debated, but the wholesale revision of financial structures it entailed probably constricted credit and market confidence in the years that followed.

The recession in 1990 and early 1991 came after the collapse of the S&L industry in the late 1980s and the failure of almost 1600 banks during the same period. Both were blamed on insufficient regulatory authority or lax enforcement—again like the narrative that supported the Dodd-Frank Act—and produced the Financial Institutions Recovery, Reform and Enforcement Act (FIRREA) in 1989 and the FDIC Improvement Act (FDICIA) in 1991.

These laws increased the regulatory authority of federal bank regulators, and under pressure from Congress and the public they cracked down on depository institutions, causing a credit crunch and what was called a “jobless recovery” in 1991. As one observer put it, the Comptroller of the Currency “had softened regulatory policies on banks early in his tenure, helping fuel excessive real estate lending by banks. By mid-1990 and early 1991, the regulatory attitudes had apparently changed: “Bank examiners became too restrictive, helping to create a near credit crunch.” In addition, the first set of Basel risk-based capital rules were adopted in 1988 and were gradually phased in at this time, requiring banks to re-compute their capital positions and in many cases required them to increase their capital.

Thus, there is historical evidence that the slow recovery from the 2008 financial crisis is due in part—maybe primarily—to the fact that the Dodd-Frank Act was adopted shortly after the crisis. Instead of allowing the economy and the financial system to heal naturally, it introduced constraints, costs and uncertainties that have interfered with the natural course of the recovery. Moreover, like the Pecora hearings, Dodd-Frank was based on the idea that the private sector was to blame for the crisis and thus sought to punish the very entities that were necessary to finance a recovery.

The idea that a post-recession series of actions can in fact slow an economic recovery receives added weight from a recent book by James Grant called The Forgotten Depression. Grant traces the sharp downturn and the following sharp recovery in 1920 and 1921. The downturn in 1920 was severe. “Just how severe,” writes Grant, “is a question yet to be settled…Official data as well as contemporary comment paint a grim picture. Thus, the nation’s output in 1920-21 suffered a decline of 23.9 percent in nominal terms, 8.7 percent in inflation-(or deflation)-adjusted terms. From cyclical peak to trough, producer prices fell by 40.8 percent. Maximum unemployment ranged between two million and six million persons…out of a nonagricultural labor force of 31.5 million. At the high end of six million, this would imply a rate of joblessness of 19 percent.”

But the government did nothing. President Wilson had suffered a second severe stroke in October 1919, and was partially paralyzed, although this fact was withheld by the White House. What little energy Wilson had through the election year of 1920 was reserved for the fight over the League of Nations. The Republican Harding administration, which followed, did nothing either, says Grant. “The successive administrations of Woodrow Wilson and Warren G. Harding met the downturn by seeming to ignore it—or by implementing policies that an average 21st century economist would judge disastrous. Confronted with plunging prices, incomes and employment, the government balanced the budget and, through the newly instituted Federal Reserve, raised interest rates…Yet by late 1921, a powerful, job-filled recovery was under way. This is the story of America’s last governmentally unmedicated depression.” Needless to say, there was no new regulation, and the economy recovered quickly.

This is not to say that a laissez-faire policy is always best, but simply that adding new regulatory activity after a severe recession seems to slow a rapid return of economic growth, and that certainly seems to be borne out by the examples cited above.

It is of course possible that the 2008 financial crisis and the ensuing recession were such shocks to the economic system that they have caused a secular change in the performance of the US economy—a “new normal” of slow growth and declining living standards for the middle class. However, it is far more likely that government policies are responsible for these conditions, and if we look for the policies that could have had the greatest effect on the economy since the financial crisis, there have been only three—the Affordable Care Act, the Fed’s historically low interest rates, and the Dodd-Frank Act. Neither the ACA nor low interest rates should have had a repressive effect on new business formation; quite the contrary. Nor should either of them significantly suppress capital investment—again, it’s more likely that they’ve both had stimulative effects. So that leaves Dodd-Frank as the most likely cause of the slow-growth economy we have been experiencing.

Finally, quite apart from the fact that Dodd-Frank has probably slowed the recovery from the financial crisis and the ensuing recession through adding excessive regulatory costs, it is important to note that it has also added regulations that impose major costs but which have little or no relationship with the financial crisis. In a 2014 study, the American Action Forum showed that three requirements in the Dodd-Frank Act, the pay ratio rule, the Conflict Minerals provisions and the Volcker Rule totaled more than $10 billion in costs for financial firms, but none has been shown to be a cause of the crisis. For the reasons outlined earlier, these costs are reducing the availability of credit and slowing economic growth for reasons of social justice or the placation of a special interests, not because they were deemed necessary to address the financial crisis. In the case of the Volcker Rule, as discussed later, it may be the eventual cause of another financial crisis by reducing liquidity in the financial markets. In this case, the eagerness of Congress to impose more restrictions on the financial system than were warranted by its own misdiagnosis of what happened in 2008 may have planted the seeds for a future crisis.

How Dodd-Frank has Slowed Economic Growth

If excessive regulatory costs have slowed the recovery from the financial crisis, they will continue to slow economic growth until they are reduced or eliminated. In the balance of this testimony, I will focus on the additional regulatory costs imposed on banking organizations, especially small banks, because I think there is a strong case that reducing credit availability from banks is having a particularly adverse effect on small business, which in turn is the principal source of growth and employment in the US economy.

The most important factor in this analysis is the dependence of small and medium sized businesses on bank lending. Larger businesses have access to other sources of credit, primarily through the capital markets. Firms that have registered their securities with the SEC are able to sell bonds, notes and short-term paper in the capital markets—normally a less expensive and easier process than borrowing from a bank. The chart below shows that since the mid-1980s the capital markets have outcompeted the banking industry as a source of credit for business corporations. This popular alternative means of financing, however, is not available to small or medium sized businesses, because they are not generally owned by public shareholders and do not report their financial results to the SEC. Accordingly, they are more dependent on bank financing than larger firms. Greater and more costly regulation of banks, then, would inevitably cause either an increase in the cost of bank credit, a reduction in its availability, or both, to these smaller firms.

Source: Fed Flow of Funds

A second factor causing difficulties for small banks in particular is the narrative underlying the Dodd-Frank Act—that the financial crisis was caused by insufficient regulation of banks and other financial firms. Solid academic work by my AEI colleague Paul Kupiec and two others has shown that when the regulators were said to have been lax, that is followed by more intrusive activity by bank examiners, and this reduces the amount of lending. “[S]upervisory restrictions,” they report, “have a negative impact on bank loan growth after controlling for the impact of monetary policy, bank capital and liquidity conditions and any voluntary reduction in lending triggered by weak legacy loan portfolio performance or other bank losses.” This analysis received confirmation from Fed Governor Duke in testimony to Congress in February 2010, “Some banks may be overly conservative in their small business lending because of concerns that they will be subject to criticism from their examiners…some potentially profitable loans to creditworthy small businesses may have been lost because of these concerns, particularly on the part of small banks.”

Finally, the new and more costly regulation imposed by Dodd-Frank appears to have stalled the formation of new banks, which in turn has also affected the availability of credit for the small and medium-sized businesses that are dependent on bank lending. A Federal Reserve Bank of Richmond report in March 2015 notes that “The rate of new-bank formation has fallen from an average of about 100 per year since 1990 to an average of about three per year since 2010.” Trying to assess the reasons for this sharp decline, the report continued, “Banking scholars …have found that new entries are more likely when there are fewer regulatory restrictions. After the financial crisis, the number of new banking regulations increased with the passage of legislation such as the Dodd-Frank Act. Such regulations may be particularly burdensome for small banks that are just getting started.”

The authors suggest other possible causes, but the fact that the decline became so severe in 2010, the year of the enactment of Dodd-Frank, is strong evidence that the new requirements in the act—which have been cited again and again by small banks since 2010—are responsible. In any event, the decline in new banks caused an overall decline of 800 in the total number of small independent banks between 2007 and 2013. This would have had a disproportionate effect on small business and account in part for the failure of the economy to gain any momentum since the enactment of Dodd-Frank.

Another 2015 study ties the decline of community banks even more closely to the Dodd-Frank Act: “[C]ommunity banks’ share of U.S. banking assets and lending markets has fallen from over 40 percent in 1994 to around 20 percent today. Interestingly, we find that community banks emerged from the financial crisis with a market share 6 percent lower, but since the second quarter of 2010—around the time of the passage of the Dodd-Frank Act—their share of commercial banking assets has declined at a rate almost double that between the second quarter of 2006 and 2010. Particularly troubling is community banks’ declining market share in several key lending markets, their decline in small business lending volume and the disproportionate losses being realized by particularly small community banks.”

If these factors are indeed adversely affecting banks and thus small business, we should see a difference in growth rates between small business and larger businesses since 2010, when the Dodd-Frank Act was adopted. A recent paper shows exactly that kind of disproportionate effect on small and medium size businesses.

In a Goldman Sachs report published in April 2015, and titled “The Two-Speed Economy,” the authors posit that new banking regulations have made bank credit both more expensive and less available. “This affects small firms disproportionately because they largely lack alternative sources of finance, whereas large firms have been able to shift to less-expensive public market financing.” But banking regulation was not the only regulation that had an effect on small business: “While banking regulation has played a key role, regulation outside of banking has also raised the fixed costs of doing business.” These costs fall most heavily on small firms because larger firms can more easily cope with the fixed costs imposed by regulation.

Using IRS data, the Goldman study finds that large firms—those with $50 million or more in revenue annually, have been growing revenue at a compounded annual rate of 8 percent, while firms with less than $50 million in revenue have been growing revenue at an average of only 2 percent compounded annually. Using Census data, Goldman found that “firms with more than 500 employees grew by roughly 42,000 per month between 2010 and 2012, exceeding the best historical performance over the prior four recoveries. In contrast, jobs at firms with fewer than 500 employees declined by nearly 700 per month over the same timeframe, whereas this figure had grown by roughly 54,000 per month on average over the prior four recoveries.”

This accounts for the dearth of new business formations. Small firms are simply unable to get the credit that used to be available to small business and small business start-ups, and the credit that they can get is more expensive. This would also have a disproportionate effect on employment in the recovery, because small business is the principal source of new employment growth in the US economy.

The Goldman paper then turns to the lack of capital investment, and also finds the source of that in financial regulation. “Even as large firms experience a relatively robust recovery, they appear to be investing less than we would expect given their historically high profit margins, and investing with a bias toward shorter term projects; this dynamic may be playing out because large firms are facing less competition from smaller firms. Investments in intellectual property, for example, are tracking nearly five percentage points below even the low end of the historical experience and more than 20 percentage points below the historical average.”

Finally, the Goldman paper expresses concern that this is not necessarily a temporary phenomenon: “Taken together, the reduced competitiveness of small firms and the changing investment decisions of larger ones are reshaping the competitive structure of the US economy in ways that are likely to reverberate well into the future, and in ways that any future evaluation of the aggregate effects of post-crisis regulations should consider.”

It would be hard to find a better way to express the dangers of leaving the Dodd-Frank Act in place without serious reforms.

Dodd-Frank, the Volcker Rule and the Danger of another Financial Crisis

Any policy that reduces market liquidity should be worrisome for this country, given the experience of the financial crisis. More than anything else, the crisis was a liquidity crisis, not a solvency crisis. When Lehman Brothers was allowed to fail, liquidity in the market dried up, meaning that firms that wanted to sell securities to raise cash were not able to do so. We don’t know what lies before us, and what event or events could cause many investors to seek to liquidate their holdings of fixed income securities, but what is clear is that if the market does not have the liquid resources to buy these securities their prices will drop precipitously. The securities “fire sales” that regulators say they are worried about will become a reality. The irony is that it is the laws and regulations that Congress has put in place through the Dodd-Frank Act that will cause the crisis.

Chief among these is The Volcker Rule, which forbids banks or their affiliates to engage in proprietary trading of debt securities. Although it was justified by the claim that banks were taking risks with insured deposits, this was truly an absurd idea. The riskiest thing that banks do with their insured deposits is make loans. Trading securities in a liquid market is far less risky than giving a borrower a substantial amount of money in the hope of eventual repayment. Before the Volcker rule, banks were active in making markets in debt securities by standing ready to buy or sell these securities . It is very difficult to tell the difference between making a market—that is, buying and selling for your own account—and proprietary trading. As a result, banks have begun to reduce their market-making activities, leaving the market for all securities with far less liquidity than it had before the Volcker rule was adopted. Some large banks have simply disbanded their bond-trading groups.

This has substantially reduced the amount of capital and liquidity available to the debt markets. The lack of liquidity has almost certainly increased the buy-sell spreads in the debt markets and the costs of buyers, sellers and investors who trade in fixed income securities. It is now much more difficult to sell a fixed income security and thus much more risky to buy one. As reported on May 20, 2015 in the Wall Street Journal,

Talk to almost any banker, investor or hedge-fund manager today and one topic is likely to dominate the conversation. It isn’t Greece, or the U.S. economy, or China…It is the lack of liquidity in the markets and what this might mean for the world economy—and their businesses. Market veterans say they have never experienced anything like it. Banks have become so reluctant to make markets that it has become hard to execute large trades even in the vast foreign-exchange and government bond markets without moving prices, raising fears investors will take unexpectedly large losses when they try to sell. The U.S. corporate-bond market has almost doubled to $4.5 trillion since the start of the crisis, yet banks today hold just $50 billion of bonds compared with $300 billion precrisis.

As Douglas Elliott of the Brookings Institution has pointed out, there have been several periods of extreme volatility in recent years, for which market liquidity was necessary. Nevertheless, Basel III’s capital requirements and Stable Funding Ratio, and the Fed’s new Liquidity Coverage Ratio have all increased the cost of funding a portfolio of bonds, all of which—together with the Volcker Rule—reduce the amount of liquidity in the market. This could lead to a serious liquidity crisis if one or more major financial institutions is required to sell assets to meet its cash needs: “Illiquidity in financial markets,” says Elliott, “can help trigger or exacerbate a financial crisis by creating actual or paper losses at banks or other financial institutions. If a bank needs to raise cash quickly, perhaps to meet deposit outflows in the event of a loss of confidence in that institution, they will likely need to sell securities, especially if they have an excessive mismatch between the maturities of their assets and liabilities. In illiquid markets, this would require ‘fire sales’ in which the seller accepts a significantly lower price in order to get cash quickly.”

On October 15, 2014, the Treasury market moved 40 basis points, an almost unheard of drop for the world’s most liquid market. Investigations are underway, but it is difficult to believe that this move was not related to the fact that banking organizations—the largest players in the fixed income markets—now hold only one-sixth of the amount of bonds they held before the crisis. There are fewer market makers and the fewer market makers have fewer cash resources. This is a prescription for a liquidity disaster similar to the 2008 financial crisis.

The Obama administration has denied that the Volcker Rule could be a major factor—or indeed any factor—in the decline of market liquidity, but in July 2015, Lael Brainard, Fed governor, admitted that regulation could be playing a role. Other experienced market observers have been more definitive. In a Wall Street Journal op-ed piece on June 9, 2015, Stephen Schwartzman, the CEO of Blackstone, noted that “A warning flashed last October in the U.S. Treasury market with huge intraday moves, unrelated to external events. Deutsche Bank has reported that dealer inventories of corporate bonds are down 90% since 2001, despite outstanding corporate bonds almost doubling. A liquidity drought can exacerbate, or even trigger, the next financial crisis.”

Another article in the Wall Street Journal in May 2015, reported that a board member of the European Central Bank, Benoit Coeure, saw “extreme volatility in global capital markets [as] showing signs of reduced liquidity.” The article noted that “The world’s largest banks dumped around $1 trillion in assets from government bond-trading businesses between 2010 and the end of last year.”

Still a third article, in the American Banker in June 2015, quoted Richard Berner, the director of the Office of Financial Research, a Treasury unit, to the effect that “the financial reform law could ‘be contributing to more permanent adjustments that could impair market functioning,’ including by reducing market liquidity.”

The administration’s refusal thus far to admit that the Dodd-Frank Act may be responsible for what could be a future financial catastrophe, must be seen as a wholly political effort to defend what they see as one of President Obama’s key legacies. With financial markets “flashing danger” it is time to look objectively at this problem before it causes another financial crisis. Thus, the Dodd-Frank Act is not only holding back the growth of the economy by reducing the credit available for small businesses; it is also creating the foundation for another financial crisis in the future.

Comments Off on The Dodd Frank Act Five Years Later: Are We More Prosperous?

For years, Congress has been trying to determine whether the Financial Stability Oversight Council is recognizing legitimate risks to the economy when it designates large financial firms as systemically important financial institutions. Now, thanks to MetLife’s legal challenge to its designation as a SIFI, Congress has an answer: The FSOC had no credible metrics or data to support its designation of MetLife.

The sponsors of the 2010 Dodd-Frank Act created the council in the belief that the failure of Lehman Brothers in September 2008 caused the financial crisis. The council’s 10 voting members—all heads of federal financial regulatory agencies—are charged with identifying other companies whose failure could cause another financial crisis. Firms designated as SIFIs are turned over to the Federal Reserve for what Dodd-Frank calls “stringent” regulation.

In reality, Lehman’s role in the crisis is questionable. There was chaos after it failed, but this was due to the government’s sudden reversal of the policy it established six months earlier with the rescue of Bear Stearns. That reversal upended the expectations of market participants; they sought and hoarded cash, creating the liquidity shortage we know as the financial crisis.

Yet no large financial firms failed as a result of Lehman’s bankruptcy. This means there is no real evidence for the widely held idea that large financial institutions are so interconnected that the failure of one will drag down others. Although this undermines the rationale for the SIFI designation process, the metrics the FSOC uses to show dangerous interconnections have never been disclosed.

FSOC regulations outline two principal ways that the distress or failure of a firm could cause instability in the financial system as a whole. One is by causing losses to others financially exposed to the failing firm, say by holding its debt securities. This is called the exposure channel. The other is by a “fire sale” liquidation of assets that drives down asset prices and thus weakens other firms holding the same assets. It’s called the liquidation channel.

In January, MetLife, the nation’s largest insurer, challenged its designation as a SIFI in federal court. Its brief for summary judgment, filed on June 16, demolishes the idea that the FSOC designated MetLife because of dangers posed by MetLife through either channel.

In addressing the exposure channel, Met Life submitted evidence showing that even its total collapse would not pose a threat to other large firms. For example, in the unlikely event that the largest U.S. banks were to lose 100% of their exposure to MetLife, their losses would not exceed 2% of their capital. By comparison the fines recently levied on the largest U.S. banks by the Justice Department were four times as large. Yet those fines had no observable effect on the health of the banks involved.

As for the liquidation channel, a study done for MetLife by Oliver Wyman showed that even in the implausible event that all policyholders were to surrender their policies and ask for return of their cash values—and all other MetLife liabilities that could accelerate would immediately become due—the firm could still liquidate enough assets to cover its liabilities “without causing price impacts that would substantially disrupt financial markets.” The FSOC produced no data to contradict this evidence. Instead, it merely asserted that these assets sales “could” have an adverse effect on the broader economy.

The facts in MetLife’s brief raise some broad policy questions:

First, why, despite the apparent lack of evidence to support its case, did the FSOC designate MetLife as systemically important? I have written in these pages, and some members of Congress have also observed, that the actions of the council mirror the decisions of the Financial Stability Board (FSB), a mostly European group of central bankers and finance ministers of which the U.S. Treasury and the Fed are members. The FSB designated MetLife as a “global” SIFI in July 2013, without disclosing any of its evidence for doing so. The MetLife designation adds weight to the idea that the FSOC considers itself bound by the prior FSB decisions in which the Treasury and Fed concurred.

Second, although there have been three other nonbank SIFI designations—GE Capital, AIG and Prudential Insurance—MetLife’s brief is the first public disclosure of the data the FSOC used. If the interconnections and exposures between large financial firms are so limited that the failure of one will not seriously impair the safety and soundness of others, the rationale for designating particular firms as systemically important is unclear. A SIFI designation, in effect, is a government declaration that a firm is too big to fail—and subjecting firms to pointless designations and onerous regulations cannot be beneficial to the U.S. economy.

Now that we know the weakness of the FSOC’s data, Congress should consider whether the SIFI designation process makes sense. It should not leave the answer to an unaccountable organization of financial regulators.

Comments Off on MetLife Calls the Regulators’ Bluff

The central bank’s expansive regulatory powers should be subject to congressional and executive branch oversight.

With Republicans soon to hold majorities in the House and Senate, many commentators are speculating that the Federal Reserve will receive much more critical attention in 2015. In September, a large bipartisan majority in the House passed a bill to have the Government Accountability Office audit the Fed’s activities, including its monetary policies. The bill went nowhere thanks to Senate Majority Leader Harry Reid, but it could have significant support in next year’s Republican Senate.

Fed Chair Janet Yellen has expressed a legitimate fear that the Federal Reserve Transparency Act would endanger the Fed’s independence on monetary matters. But the Fed has now accumulated so much regulatory power that it can no longer claim the right to avoid congressional oversight. If the central bank hopes to maintain its monetary independence over time, it will have to surrender its regulatory authority.

There are serious potential conflicts of interest between the Fed’s regulatory and monetary roles. This became clear during the financial crisis, when the central bank used its existing authority under the Federal Reserve Act to provide assistance to financial institutions that were having liquidity problems. Many of these firms—bank holding companies, banks and their nonbank subsidiaries—are regulated directly or indirectly by the Fed. Their failure could have been seen as regulatory failure by the Fed. Did the Fed provide financial assistance to avoid this criticism, or because it was best for the economy and the financial system? It’s a painful question to consider, but the fact that it can legitimately be asked suggests the problem—and a reason why the Fed should not have both monetary and regulatory powers.

In 1999 the Gramm-Leach-Bliley Act gave the Fed “umbrella” authority to oversee the capitalization and activities of insurers and broker-dealers that were subsidiaries of bank holding companies. That made the central bank the closest thing to a “systemic regulator” of the U.S. financial system, with the ability to oversee the work of other financial regulators such as the Securities and Exchange Commission.

The Fed clearly failed in this role before the 2008 financial crisis, but in typical Washington fashion the 2010 Dodd-Frank Act enlarged the Fed’s powers. It now has authority to supervise all of the large nonbank financial firms that are designated as systemically important financial institutions by a council of regulators.

While enlarging the central bank’s authority in 2010, Congress never asked whether the Fed’s mandate to promote both stable prices and full employment—itself a situation rife with conflict—led it to pull its regulatory punches. Now Congress is wondering whether the Fed is a captive of the banks. To fight this charge, the Fed is trying to show that it is a tough regulator, flexing its regulatory muscles by telling banks that it doesn’t like some of the loans they are making—such as leveraged loans in corporate acquisitions. This comes perilously close to credit allocation and is especially troubling if it is motivated by an effort to maintain the Fed’s regulatory authority and monetary policy independence.

Apart from whipsawing the financial system so the Fed can make a political point, this practice and other excessive regulation adds significant operating costs for banks and others, causing them to withdraw from lines of business that regulatory costs make less profitable. These costs are also a burden on competition; large banks can bear them more easily than can smaller competitors. That’s why in 2013 Jamie Dimon, chairman of J.P. Morgan Chase, the largest bank in the U.S., referred to more regulation as a “bigger moat” against competition.

Because the Fed’s operating funds come primarily from interest on the government securities it holds, the central bank does not receive congressional scrutiny in the appropriations process. Nor are its expenditures examined by the Office of Management and Budget in preparing the president’s annual budget. Both reviews are ways for Congress and the president to control regulatory overreach.

At a minimum, as long as the Fed retains its regulatory authority, it should be required to provide Congress with a budget for its regulatory activities, to show each year how it met the prior year’s budget, and to explain why it should be permitted to allocate more to its regulatory functions in the year to come. In this review, the Fed should describe its regulatory policies in detail and explain and justify its plans for the future.

These steps would substitute for the authorization and appropriations reviews that occur each year for most other agencies. If there is an annual audit, it should tell Congress, the president and the public whether the funds that the Fed is using for regulation are being used efficiently. This would restore a small degree of accountability.

Before Congress acts on audit legislation that will certainly complicate the agency’s effort to retain its independence on monetary policy, the Fed should offer to support the consolidation of its regulatory authority into a separate federal financial regulatory body. That was recommended in the Ronald Reagan and George W. Bush administrations. The Federal Reserve has always resisted these proposals, but that may no longer be either advisable or possible.

A ‘chain’ of routine securities transactions, the Fed suggests, can transform a nonsystemic firm into a systemic firm.

Recent statements by senior Federal Reserve officials show that the agency is stepping up efforts to investigate and ultimately regulate what they call the “shadow-banking system.” As the regulators define that term, it is nothing less than capital and securities markets—the industries principally responsible for the growth of the U.S. economy over the past 40 years.

In December, Stanley Fischer , the Fed’s vice chairman and head of its internal systemic-risk committee, told an asset-management group that the New York Fed is “mapping” the relationships between and among financial institutions with a view to determining the scope of the shadow-banking system. The Fed, he said, is considering whether it has sufficient authority to regulate shadow banks. If it doesn’t, he said, the Fed will turn the matter over to the Financial Stability Oversight Council—created by the Dodd-Frank law and made up of the heads of all federal financial regulators, with the Treasury secretary as chairman—for appropriate action.

And on Jan. 30, Daniel Tarullo, a Fed governor, told a conference of financial regulators that the agency was working to corral financial activities that “migrate outside the regulated perimeter”—that is, financial activities that are not regulated like banks. The Fed, he said, wants to “serve the macroprudential aim of moderating the build-up of leverage” in shadow banks.

Most people probably imagine that the term shadow banking refers to large nonbank financial institutions that do what regulated banks do—borrow short-term funds like deposits and turn them into long-term assets like loans. Maturity transformation, as it is called, can be risky, because a firm that has lent out funds it has borrowed short-term may be pressed for cash if its short-term creditors want their funds returned immediately. The fear is that large firms facing this difficulty could fail, creating a “systemic” event.

For this reason, Dodd-Frank is based on the idea that all large nonbank financial institutions, including investment banks, finance companies and insurers, should be subject to designation by the FSOC as systemically important financial institutions, or SIFIs. Once designated, SIFIs are turned over to the Fed for stringent regulation.

The regulators apparently want to cast an even wider net. A 2012 report by the international Financial Stability Board—made up of central bankers and bank regulators of which the U.S. Treasury and the Fed are members—stated that systemic risks are created in the shadow-banking system through “a complex chain of transactions, in which leverage and maturity transformation occur in stages.”

What is a “chain of transactions”? As former Fed Chairman Ben Bernanke explained that year, a finance company might create a pool of auto loans for securitization. Afterward, “an investment bank might sell tranches of the securitization to investors. The lower-risk tranches could be purchased by an asset-backed commercial paper (ABCP) conduit that, in turn, funds itself by issuing commercial paper that is purchased by money market funds.” In other words, a “chain of transactions” involving many different firms can create the same systemic risks as a single large firm.

These are normal transactions in the securities and capital markets. So when Fed officials say that they are investigating and hope to regulate shadow banking, what they mean is that they want to regulate what kind of transactions occur in the securities and capital markets. What is necessary, Mr. Tarullo noted, is a “significant building out of a regulatory regime” for shadow banks, “and so I think that’s where attention is going to be paid.”

One big, threshold question: Where do the Fed and FSOC imagine that they obtained the grant of such power? It can’t be from Dodd-Frank. As capacious as this legislation is, it doesn’t provide authority to regulate financial firms that by themselves are not systemic but become systemic because they participate in a “complex chain of transactions.”

The most likely possibility is the Financial Stability Board, an entity little known outside the financial industry. This group was deputized by the G-20 leaders in 2009 to reform the international financial system, and since then—with the explicit approval of the G-20—has made the regulation of the shadow-banking system a major objective. Perhaps the FSOC and the Fed see the decisions of the G-20—of which President Obama is a member—as authority for their actions in the U.S.

While this might be true in other countries, the U.S. Constitution provides for a separation of powers in which Congress makes the laws and the president carries them out. The fact that a president has agreed with other G-20 leaders to take international action of some kind would not give federal agencies the authority to act in the absence of explicit legislation.

And yet if Congress fails to insist on a recognition of its authority, the Federal Reserve and the Financial Stability Oversight Council will be free to take control of and regulate sectors of the economy that even the drafters of the far-reaching Dodd-Frank law saw fit not to include.

Comments Off on Regulation of Shadow Banking Takes a Dark Turn

A ‘chain’ of routine securities transactions, the Fed suggests, can transform a nonsystemic firm into a systemic firm.

Recent statements by senior Federal Reserve officials show that the agency is stepping up efforts to investigate and ultimately regulate what they call the “shadow-banking system.” As the regulators define that term, it is nothing less than capital and securities markets—the industries principally responsible for the growth of the U.S. economy over the past 40 years.

In December, Stanley Fischer , the Fed’s vice chairman and head of its internal systemic-risk committee, told an asset-management group that the New York Fed is “mapping” the relationships between and among financial institutions with a view to determining the scope of the shadow-banking system. The Fed, he said, is considering whether it has sufficient authority to regulate shadow banks. If it doesn’t, he said, the Fed will turn the matter over to the Financial Stability Oversight Council—created by the Dodd-Frank law and made up of the heads of all federal financial regulators, with the Treasury secretary as chairman—for appropriate action.

And on Jan. 30, Daniel Tarullo, a Fed governor, told a conference of financial regulators that the agency was working to corral financial activities that “migrate outside the regulated perimeter”—that is, financial activities that are not regulated like banks. The Fed, he said, wants to “serve the macroprudential aim of moderating the build-up of leverage” in shadow banks.

Most people probably imagine that the term shadow banking refers to large nonbank financial institutions that do what regulated banks do—borrow short-term funds like deposits and turn them into long-term assets like loans. Maturity transformation, as it is called, can be risky, because a firm that has lent out funds it has borrowed short-term may be pressed for cash if its short-term creditors want their funds returned immediately. The fear is that large firms facing this difficulty could fail, creating a “systemic” event.

For this reason, Dodd-Frank is based on the idea that all large nonbank financial institutions, including investment banks, finance companies and insurers, should be subject to designation by the FSOC as systemically important financial institutions, or SIFIs. Once designated, SIFIs are turned over to the Fed for stringent regulation.

The regulators apparently want to cast an even wider net. A 2012 report by the international Financial Stability Board—made up of central bankers and bank regulators of which the U.S. Treasury and the Fed are members—stated that systemic risks are created in the shadow-banking system through “a complex chain of transactions, in which leverage and maturity transformation occur in stages.”

What is a “chain of transactions”? As former Fed Chairman Ben Bernanke explained that year, a finance company might create a pool of auto loans for securitization. Afterward, “an investment bank might sell tranches of the securitization to investors. The lower-risk tranches could be purchased by an asset-backed commercial paper (ABCP) conduit that, in turn, funds itself by issuing commercial paper that is purchased by money market funds.” In other words, a “chain of transactions” involving many different firms can create the same systemic risks as a single large firm.

These are normal transactions in the securities and capital markets. So when Fed officials say that they are investigating and hope to regulate shadow banking, what they mean is that they want to regulate what kind of transactions occur in the securities and capital markets. What is necessary, Mr. Tarullo noted, is a “significant building out of a regulatory regime” for shadow banks, “and so I think that’s where attention is going to be paid.”

One big, threshold question: Where do the Fed and FSOC imagine that they obtained the grant of such power? It can’t be from Dodd-Frank. As capacious as this legislation is, it doesn’t provide authority to regulate financial firms that by themselves are not systemic but become systemic because they participate in a “complex chain of transactions.”

The most likely possibility is the Financial Stability Board, an entity little known outside the financial industry. This group was deputized by the G-20 leaders in 2009 to reform the international financial system, and since then—with the explicit approval of the G-20—has made the regulation of the shadow-banking system a major objective. Perhaps the FSOC and the Fed see the decisions of the G-20—of which President Obama is a member—as authority for their actions in the U.S.

While this might be true in other countries, the U.S. Constitution provides for a separation of powers in which Congress makes the laws and the president carries them out. The fact that a president has agreed with other G-20 leaders to take international action of some kind would not give federal agencies the authority to act in the absence of explicit legislation.

And yet if Congress fails to insist on a recognition of its authority, the Federal Reserve and the Financial Stability Oversight Council will be free to take control of and regulate sectors of the economy that even the drafters of the far-reaching Dodd-Frank law saw fit not to include.

Comments Off on Regulation of Shadow Banking Takes a Dark Turn

From the time it was first proposed by the Obama administration early in 2009, the legislation that eventually became the Dodd-Frank Act was opposed by Republicans in Congress. It got no Republican votes when it passed the House and only two Republican votes when it passed the necessary procedural vote in the Senate.

The reason for this nearly unanimous Republican opposition is simple: the key provisions of the act bore little relationship to the actual causes of the crisis. Indeed, the record shows that in designing and adopting the act neither the Obama administration nor the Democratic Congress made any effort to understand why there was a financial crisis in 2008 or the role of the government’s housing policies in bringing it about.

The necessary information was certainly available. Fannie Mae and Freddie Mac became insolvent in September 2008, and were immediately taken over by their regulator as conservator. Thus, when the Obama administration came into office in January 2009, it had access to all the financial information of both firms.

In August 2009, now under the government’s supervision, Fannie published the first reasonably complete credit report on its mortgage exposures. This showed that 81 percent of Fannie’s 2008 losses had come from its exposure to both subprime loans (loans in which the borrower had a FICO credit score of 660 or lower) and other loans that were particularly risky because they had low or no downpayments or other deficiencies. This should have been a surprise; up to that point, most people thought Fannie only acquired prime loans. Further inquiry would have shown that Freddie Mac had suffered similar losses for the same reason. Because it was now in charge of Fannie and Freddie, the administration had this information well before it was published.

In June of 2008, this and other data showed that there were 31 million subprime and other risky mortgages in the US financial system, amounting to 56 percent of all US mortgages. Of the 31 million loans, 76 percent were on the books of government agencies, primarily Fannie and Freddie (about two-thirds) but also FHA, the Veterans Administration, and others. This showed incontrovertibly that it was the government-and not the private sector-that had created the demand for the vast majority of these loans.

If the administration and Congress had really wanted to know what happened in the financial crisis, the information was at hand. The data cited above made clear that the overwhelming majority of the losses in the mortgage meltdown had come from subprime and other risky loans. If Fannie and Freddie had suffered 81 percent of their losses because of these mortgages, the defaults on these loans were what had driven down housing prices 30-40 percent all over the United States.

Any serious effort to understand the crisis would have asked at this point why government agencies held so many subprime and other risky mortgages, and that inquiry would have turned up the affordable housing goals, adopted by Congress in 1992. These required Fannie and Freddie, when they bought mortgages from banks and other originators, to meet a quota: 30 percent of those mortgages had to be made to borrowers at or below the median income in the communities where they lived. Data from HUD, which administered the goals, would have shown the administration and Congress, had they been curious, that HUD had gradually increased the quota to 50 percent in 2000 and to 56 percent in 2008.

Anyone in the administration who was interested would have realized that as the quota was increased Fannie and Freddie were required to reduce their underwriting standards; it was simply impossible to meet the increasing affordable housing goals for borrowers below median income while maintaining their traditional prime mortgage standards. By 1995, they were accepting loans with 3 percent downpayments, and by 2000 loans with zero downpayments.

From that point on, the analysis would have been easy. Because Fannie and Freddie were the dominant players in the housing finance market, when they reduced their underwriting standards lenders were compelled to follow suit. Mortgage lending is competitive, and consumers went to the lenders that offered the easiest terms. Any observer would have understood why Countrywide, formerly a minor league subprime lender, ultimately became one of the largest mortgage originators in the US. It was the principal supplier to Fannie and Freddie.

But neither the Obama administration nor Congress was interested in this analysis. The narrative they adopted, and sold to the American people, was that Wall Street and other large financial institutions had taken excessive mortgage risks because they had not been sufficiently regulated. Fannie and Freddie, as HUD secretary Donovan later told Congress, bought all those subprime loans for profit or market share. The government’s role, and the affordable housing goals that drove down underwriting standards, were conveniently ignored.

The conclusion one should draw from this is that the Dodd-Frank Act is illegitimate. Although the American people were told that the act was a response to the 2008 financial crisis, and was intended to prevent similar financial crises in the future, neither the administration nor Congress ever made any effort to determine what actually caused the crisis. Instead, the narrative that drove the Dodd-Frank Act was concocted to achieve an ideological purpose: to impose greater regulation on the US financial system.

Just last week, Treasury Secretary Jack Lew wrote in an op-ed: “Given how far we have come…it is hard to understand the efforts of some to undermine our ability to protect consumers and taxpayers from excessive risks taken by financial institutions.” The false narrative will never be abandoned until the American people know the truth.

Comments Off on The illegitimate Dodd-Frank law has nothing to do with the financial crisis

Because of the government’s extraordinary role in bringing on the crisis, it should not be treated as an inherent part of a capitalist or free market system, or used as a pretext for greater government control of the financial system. On the contrary, understanding the financial crisis for what it was will permit the debate we should have had about the Dodd-Frank Act.

Far from being a failure of free market capitalism, the Depression was a failure of government. Unfortunately, that failure did not end with the Great Depression. . . . In practice, just as during the Depression, far from promoting stability, the government has itself been the major single source of instability. — Milton Friedman

Political contests often force the crystallization of answers to difficult political issues, and so it was with the question of responsibility for the financial crisis in the 2008 presidential election. In their second 2008 presidential debate, almost three weeks after Lehman Brothers had filed for bankruptcy, John McCain and Barack Obama laid out sharply divergent views of the causes of the financial convulsion that was then dominating the public’s concerns. The debate was in a town-hall format, and a member of the audience named Oliver Clark asked a question that was undoubtedly on the mind of every viewer that night:

Clark: Well, senators, through this economic crisis, most of the people that I know have had a difficult time. . . . I was wondering what it is that’s going to actually help these people out?

Senator McCain: Well, thank you, Oliver, that’s an excellent question. . . . But you know, one of the real catalysts, really the match that lit this fire, was Fannie Mae and Freddie Mac . . . they’re the ones that, with the encouragement of Sen. Obama and his cronies and his friends in Washington, that went out and made all these risky loans, gave them to people who could never afford to pay back . . .

Then it was Obama’s turn.

Senator Obama: Let’s, first of all, understand that the biggest problem in this whole process was the deregulation of the financial system. . . . Senator McCain, as recently as March, bragged about the fact that he is a deregulator. . . . A year ago, I went to Wall Street and said we’ve got to reregulate, and nothing happened. And Senator McCain during that period said that we should keep on deregulating because that’s how the free enterprise system works.

Although neither candidate answered the question that Clark had asked, their exchange, with remarkable economy, effectively framed the issues both in 2008 and today: was the financial crisis the result of government action, as McCain contended, or of insufficient regulation, as Obama claimed?

Since this debate, the stage has belonged to Obama and the Democrats, who gained control of the presidency and Congress in 2008, and their narrative about the causes of the financial crisis was adopted by the media and embedded in the popular mind. Dozens of books, television documentaries, and films have told the easy story of greed on Wall Street or excessive and uncontrolled risk-taking by the private sector — the expected result of what the media has caricatured as “laissez-faire capitalism.” To the extent that government has been blamed for the crisis, it has been for failing to halt the abuses of the private sector.

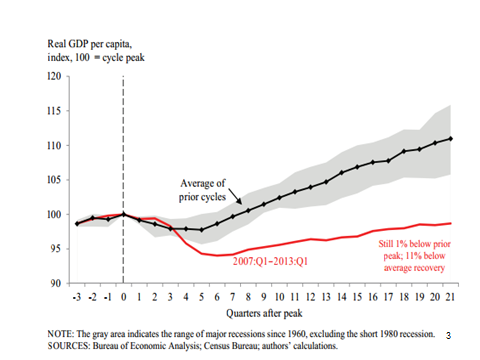

The inevitable outcome of this perspective was the Dodd-Frank Wall Street Reform and Consumer Protection Act, by far the most costly and restrictive regulatory legislation since the New Deal. Its regulatory controls and the uncertainties they engendered helped produce the slowest post-recession US recovery in modern history. Figure 1 compares the recovery of gross domestic product (GDP) per capita since the recession ended in June 2009 with the recoveries following recessions since 1960.

Unfortunately, Dodd-Frank may provide a glimpse of the future. As long as the financial crisis is seen in this light — as the result of insufficient regulation of the private sector — there will be no end to the pressure from the left for further and more stringent regulation. Proposals to break up the largest banks, reinstate Glass-Steagall in its original form, and resume government support for subprime mortgage loans are circulating in Congress. These ideas are likely to find public support as long as the prevailing view of the financial crisis is that it was caused by the risk-taking and greed of the private sector.

For that reason, the question of what caused the financial crisis is still very relevant today. If the crisis were the result of government policies, the Dodd-Frank Act was an illegitimate response to the crisis and many of its unnecessary and damaging restrictions should be repealed. Similarly, proposals and regulations based on a false narrative about the causes of the financial crisis should also be seen as misplaced and unfounded.

Figure 1. Current rebound in GDP per capita compared to previous cycles

Sources: Bureau of Economic Analysis; Census Bureau; authors’ calculations. Adapted from Tyler Atkinson, David Luttrell, and Harvey Rosenblum, “How Bad Was It? The Costs and Consequences of the 2007–09 Financial Crisis,” Staff Papers (Federal Reserve Bank of Dallas) no. 20 (July 2013): 4. Note: The gray area indicates the range of major recessions since 1960, excluding the short 1980 recession.

As demonstrated by Dodd-Frank itself, first impressions are never a sound basis for policy action, and haste in passing significant legislation can have painful consequences. During the Depression era, it was widely believed that the extreme level of unemployment was caused by excessive competition. This, it was thought, drove down prices and wages and forced companies out of business, causing the loss of jobs. Accordingly, some of the most far-reaching and hastily adopted legislation — such as the National Industrial Recovery Act and the Agricultural Adjustment Act (both ultimately declared unconstitutional) — was designed to protect competitors from price competition. Raising prices in the midst of a depression seems wildly misguided now, but it was a result of a mistaken view about what caused the high levels of unemployment that characterized the era.