Posts by MarkNestmann:

- Paying off a loan;

- Objecting to completing Currency Transaction Reports (required for transactions over $10,000);

- Changing currency from small to large denominations;

- Buying cashier’s checks, money orders, or travelers’ checks for less than the reporting limit ($10,000 for a cash transaction);

- Making deposits in cash, then having the money wired somewhere else; and

- Withdrawing cash without counting the cash first.

- Making an inter-library loan request for “The Little Red Book” by former Chinese communist leader Mao Tse-Tung;

- Owning a suspicious cat;

- Wearing a politically provocative shirt;

- Searching online for a pressure cooker and backpack;

- Putting a “Do not disturb” sign on the door to your hotel room;

- Making politically inflammatory remarks when getting a tattoo;

- Attempting to shield your computer screen from the viewing of others;

- Expressing frustration with “mainstream ideologies”; and

- Storing more than seven days of food in your home.

- Having a pale or dark complexion;

- Having a Hispanic appearance;

- Being between the ages of 25 and 35;

- Acting too nervous or too calm;

- Carrying $100, $50, $20, $10, or $5 bills;

- Wearing casual clothing;

- Wearing perfume;

- Having window coverings on your personal residence;

- Buying a one-way or round-trip airline ticket; and

- Being among the first, last, or middle group of passengers off of an airplane.

-

The US dollar is on a tear. Many investors purchase gold to guard against dollar devaluation. But the US Dollar Index, a weighted average of the dollar’s value against a basket of currencies, stands near its highest level (reached in March) since 2003. In the last year alone, this index has soared over 15%.

-

Digital currencies like Bitcoin are eating away at gold’s popularity. No, digital currencies aren’t backed by a commodity, but they’re not created out of thin air by a central bank either. And their ease of use and potential for anonymous financial transactions has reduced some of gold’s traditional allure.

-

Chinese consumers are selling. While it’s not received much attention in the US, Chinese stocks have cratered, dropping 30% in the last month. This drop comes on the heels of a stunning 154% gain between June 2014 and June 2015. As is often the case in roaring bull markets, many first-time stock investors used money they couldn’t afford to lose, to invest. Some of them even borrowed money to make leveraged bets. Those that borrowed money must now repay their loans with whatever asset is easiest to liquidate. In many cases, that’s gold.

-

Unprecedented appetite for high-risk investments. Who needs gold when you can get rich buying a startup company? While gold hit a 5½ year low last week, during the last quarter, venture capital (VC) companies invested the most money in high-risk startups since the heyday of the Internet boom in 2000. Back then, VC moguls were investing millions in questionable holdings such as WorldCom, Pets.com, and Baby Bob, all of which eventually declared bankruptcy. I suspect we’ll see a lot more bankruptcies when this VC frenzy ends as well.

-

Make a contribution of €650,000 (US$705,000) or more to the government;

-

Purchase €150,000 in Maltese government bonds or other approved investment; and

-

Buy a personal residence in Malta with a value of at least €350,000. Alternatively, you can lease a residence with an annual rental value of at least €16,000.

-

No exchange rate uncertainty. Eliminating exchange rates ended the ability of any one country to devalue its currency to boost exports.

-

Transparency and competition. A single currency was supposed to increase competition within the eurozone, lower consumer prices, and improve investment opportunities.

-

Reduced foreign exchange costs. Businesses and tourists in the eurozone no longer needed to pay foreign exchange fees.

-

Larger capital market. The eurozone integrated financial markets across Europe, leading to a freer flow of capital.

-

Less risk from exchange rate speculation. Speculators like George Soros have proved they can force down the value of individual currencies by taking huge short positions. But it’s much more expensive, and riskier, to target a major currency like the euro than, say, the Greek drachma.

-

Reserve currency. From the outset, the architects of the euro intended for it to be a viable alternative to the deutschmark, British pound, and the US dollar.

-

The FBI’s National DNA Index System, originally used to track sex offenders, has expanded to the point where the federal government now collects a DNA sample from every baby born in the US. In effect, newborn babies are now ranked with sex offenders.

-

The so-called E911 initiative that makes it possible for emergency responders to locate you when you dial 911 in the US quickly morphed into a massive GPS surveillance initiative. US courts have gone along, on the theory that your cell phone location data isn’t your property, and you therefore have no “expectation of privacy” that it won’t be disclosed.

-

And my “favorite” example: In the UK, anti-terrorism legislation now is being used (I kid you not) to investigate dog poop.

-

Unsubscribe from or greatly restrict activity on all social networks: Facebook, Twitter, etc.

-

Encrypt your text messages, chats, emails, phone calls, data files, etc.

-

Encrypt your data stream – the information going back and forth between your smart phone or PC and the Internet.

-

If you use webmail services, find a non-US provider.

-

Use secure non-US cloud storage.

-

Italy has literally banned all cash transactions over €999.99. To pay €1,000 or more, you must use a debit card, credit card, a “non-transferrable check,” or pay by bank transfer. Violations are punished by confiscation of 40% of the amount paid.

-

In France, cash transactions over €1,000 are now illegal. It’s also a crime to send any amount of cash by mail.

-

In Spain, the limit is a little higher: €2,500. And you “only” lose 25% of your cash if you violate the rules.

-

Drawing down bank reserves and hoarding cash. Document the withdrawals carefully so that you can prove the origin of the cash in the event of a Don Regan-style currency recall. In the US, hold only newly issued bills. More than 95% of circulating bills have drug residues on them, which under US law can be confiscated, as I discussed in this essay.

-

Converting a portion of assets now in banks or in cash to gold. Store the gold securely at home or in a non-bank depository. If you have more than $100,000 of gold, consider keeping a portion of it in a private vault outside the country you live in.

-

Keep the assets you maintain in banks in ultra-strong banks, to avoid the coming bail-ins.

-

Finally… there’s no question that technologies that will render obsolete central banks and indeed banks themselves are rapidly advancing. Bitcoin is a great example that’s worth looking into.

-

Were at birth a citizen of the US and a citizen of another country and continue to be a citizen of and taxed as a resident of that country and have been considered tax-resident in the US for no more than 10 years during the 15-year period ending with the year in which you expatriate; or

-

Give up US citizenship before you turn 18½ and were resident in the US not more than 10 years before your expatriation.

-

United States vs. 867 County Road 227

-

United States vs. $124,700 in US Currency

-

United States vs. James Daniel Good Real Property.

Spy on your customers… or else

September 23rd, 2015By Mark Nestmann.

Do you distrust the banking system? Prefer to do business in cash? Complain about the encroachment of Big Brother into every facet of your life?

If you answered “yes” to any of these questions, you’d better watch out. You’re a “person of interest” – and a growing number of businesses must report your “suspicious activities” to the feds. If they don’t, they can be fined and the responsible parties even imprisoned.

These requirements originated in a law called the “Bank Secrecy Act” (BSA). Of course, this Orwellian law has nothing at all to do with protecting bank secrecy. Indeed, the BSA has all but eliminated confidentiality.

Regulations issued under the BSA require financial institutions to notify the Financial Crimes Enforcement Network (FinCEN), a Treasury Department bureau, of any unusual transactions in which their customers engage. Reporting is mandatory for transactions that exceed $10,000 and are not the sort in which the particular customer would normally be expected to engage. For money transmitter businesses, a $2,000 threshold applies.

The businesses covered by these requirements must file “suspicious activities reports” (SARs) secretly, without your knowledge or consent. FinCEN makes the reports available electronically to every US Attorney’s office and to dozens of law enforcement agencies. No court order, warrant, subpoena, or even written request is needed to access a report.

What exactly is suspicious? According to official Treasury guidance, suspicious behavior includes:

Now, FinCEN has issued preliminary regulations that could extend these rules to investment managers. All SEC-registered investment advisers would be required to design and implement an anti-money-laundering program. They would also need to file SARs with FinCEN.

Once these rules come into effect, investment advisors would no longer be accountable to you, their client. Their highest duty, reinforced by civil and criminal sanctions, would be to act as unpaid undercover agents for the US Treasury.

But FinCEN’s suspicious transaction reporting rules are just the tip of the iceberg. For instance, official guidance from the FBI and other government agencies indicate that all of the following actions make you a terror suspect:

Then there’s the “drug courier profile” developed by the Drug Enforcement Administration (DEA). The following profiles are all court-approved reasons to search you and your property:

As Richard Miller expressed in his landmark book, Drug Warriors and Their Prey,

[B]eing a citizen is sufficient cause to suspect a person of criminal conduct, thereby constricting civil liberties protections for that person. That situation is hard to distinguish from the legal status of citizens of Nazi Germany.

In a world that views virtually everything you do as suspicious, there aren’t a lot of options to protect yourself. Indeed, simply by expressing your interest in privacy, asset protection, precious metals, or any of the other topics I cover routinely, you’re likely on one government watch list or another already.

However, you can take steps to avoid having a bank or other financial institution – including an investment manager – file an SAR on you. If you’re considering doing anything out of the ordinary in your account, talk to an officer at the bank, brokerage, or other financial institution first. For instance, you might want to let someone know before you pay off a loan or make or receive a large transfer.

If you have a reasonable explanation for the transaction, it’s much less likely to set off an alarm. And in a country in which all citizens are considered criminal suspects, that’s definitely something you want to avoid.

Comments Off on Spy on your customers… or else

Gold: It’s Time to Buy

July 30th, 2015

By Mark Nestmann.

I’m what people call a “contrarian” investor. I tend to buy assets that are out of favor with the chattering classes and the talking heads on television.

And I make it a point to sell when the “man in the street” starts giving me investment tips. That happened most recently in 2011, when over a glass of Malbec at a local watering hole, I overheard two other patrons talking about the “killing” they were about to make buying gold at $1,800 an ounce. I sold all but my core position the next day.

Since then, gold has had a tough time of it. It closed last week under $1,100 per ounce. The talking heads now predict $800 gold by the end of 2016.

I don’t agree, but I understand their logic. After all,

Under the circumstances, it’s easy to see why the talking heads see only disaster ahead for gold. But I think they’re missing the point.

That’s because gold is the ultimate “anti-dollar” investment. Despite its current strength, the dollar priced in gold has lost more than 95% of its value in the last 100 years. During that period, gold prices have increased more than 50-fold in dollar terms – from an official price of $20.67/oz. in 1915 to nearly $1,100/oz. today.

It’s also telling to observe that central banks, the folks who simply create dollars or euros out of thin air, are net buyers of gold. Indeed, as a group, the world’s central banks are buying more gold than they have in more than a half a century.

Obviously, central banks aren’t listening to the talking heads. But why are they buying gold? The only plausible reason is to hedge against a decline in value of the other assets they hold, primarily US dollars. Indeed, fully 60% of disclosed central bank reserves consist of US dollar holdings.

Central bankers understand that if the dollar takes a hit, the value of their reserves will fall sharply, unless they also hold assets that will appreciate as the dollar falls. That’s exactly what gold has done for more than a century. Indeed, gold has a 5,000-year track record as the ultimate asset to hold against debasement of a nation’s currency.

Unfortunately, it’s not at all clear how much gold central banks are buying. For instance, China announced two weeks ago that its official gold holdings now come to 1,658 tons. That’s only a fraction of what many analysts thought they had stockpiled. The small size of China’s hoard gave the talking heads yet another reason to recommend selling gold.

Yet, the Chinese might have lied about this statistic to depress the gold market further. After all, if you have a long-term strategy of accumulating a particular asset, the last thing you want to do is telegraph your intentions to others. They’ll just bid up its price, forcing you to pay more.

China is the world’s largest gold producer, mining more than 2,000 tons of gold since 2009. It’s imported at least another 4,000 tons of gold as well in this period. Chinese consumers no doubt purchased some of that gold, but I suspect a big chunk of it is sitting in the vaults of the People’s Bank of China. I think China has a lot more than 1,658 tons stockpiled.

Sure, gold could go lower. In any financial crisis, for instance, debtors must liquidate their assets to pay creditors. Since gold is a highly liquid asset, it’s easy for debtors to sell it to raise cash.

Still, gold is the cornerstone of my own portfolio. As the anti-dollar, when the dollar finally corrects – and it will – gold prices will recover, and the dollar will resume its 100-year plunge in value.

And that’s far from the only reason to buy gold. Unlike bank accounts, governments can’t “bail in” gold. If your gold is held securely in allocated form, it has far more intrinsic safety than a bank account deposit, a money market holding, or a promise to pay issued by any government.

There couldn’t be a better time to start buying gold – especially if you don’t already own some – than now.

Comments Off on Gold: It’s Time to Buy

“You? A Tax Evader?”

July 27th, 2015

By Mark Nestmann.

It’s no secret that governments worldwide are broke. One country after another is cutting social benefits and taking other measures to reduce government spending.

Take France, for instance. It’s under pressure from the EU to reduce its budget deficit to 3% of GDP. That’s the maximum permitted under the Maastricht Treaty, the agreement underpinning the EU. Currently, it’s at about 4%.

To comply with these rules, France cut family allowances and reduced grants to local authorities. It’s also started a renewed crackdown against tax evasion. It even laid off 7,500 soldiers.

But that’s not all. France also recently expanded incentives for new residents. The incentives exempt from tax some forms of income generated outside France.

That policy will reduce tax collections in the short term. But in the long-term, French decision-makers believe an influx of well-heeled foreigners will help lower the country’s budget deficit.

France is hardly alone. Throughout the world, governments are scrambling to offer tax-advantaged residence deals to wealthy immigrants.

In Europe alone, Austria, Bulgaria, Cyprus, Hungary, Ireland, Malta, Portugal, and the UK all offer cash-for-residence incentives. Tax reductions often come with the deal.

For instance, if you have £10 million (US$15.6 million) available, you can acquire residence in the UK as a “non-domiciled resident.” Simply invest the £10 million in UK government bonds or in active and trading UK companies. After just two years, you’ll qualify for UK citizenship and passport. Best of all, if you structure your affairs properly, you won’t pay any tax on your income outside the UK.

It’s even easier – and less expensive – in Malta. Legislation passed in 2013 created an “Individual Investor Programme” (IIP) that grants residence, and eventual citizenship and passport to foreigners who:

After a residence period of one year (during which you don’t need to actually physically live in Malta), you can apply for citizenship and a passport.

Outside the EU, the process is easier, faster, and much less expensive. The most cost-effective “citizenship-by-investment” arrangement now on offer is from the Commonwealth of Dominica in the Caribbean. You can obtain citizenship and a passport for a donation of $100,000, plus $30,000 or so in other costs. The entire process takes about six months, sometimes less.

Of course, not everyone approves of these arrangements. The Tax Justice Network (TJN) for instance, has bitterly criticized the concept of countries selling citizenship and residence rights.

John Christensen, TJN’s director, says that people seek alternative residence and citizenship “so they can evade taxes.” These options exist, he claims, so that “you can escape responsibilities.”

Regular readers won’t be surprised that I disagree with these statements. Of course, every national government imposes some form of tax in order to finance its existence. But it’s only rational for individuals or companies to seek lower tax burdens if those they’re paying now seem too high. Indeed, companies have a fiduciary duty to shareholders to reduce expenses, including taxes, to the lowest level possible to maximize profits.

Does that sound like tax evasion to you? After all, who’s a better judge of how to spend your hard-earned money? You or a government bureaucrat?

There’s a bigger picture here as well. We live in a world where governments impose increasingly stringent travel restrictions through visa requirements. Governments justify visa restrictions to fight terrorism, protect the local labor market, preserve public health, etc. Turmoil in Syria, Libya, Iraq, and other countries has forced millions of people from their homes, leading to even stricter immigration curbs.

At the same time, global debt levels have never been higher. Is it any wonder that some countries have decided to open a door to select individuals who make the requisite investment or contribution? The products these countries offer – residence, citizenship, and a passport – cost virtually nothing to provide. Yet, they’re more valuable than ever in today’s chaotic world.

No matter where you live, though, getting a second residence – and if possible, a second citizenship and passport – is a wise move. If the country you live in descends into chaos, you’ll have a “Plan B” to deal with it. And no… despite the statements of blowhards like John Christensen, qualifying for a second residence or passport doesn’t make you a tax evader.

Comments Off on “You? A Tax Evader?”

The Beginning of the End for the Euro

July 9th, 2015

By Mark Nestmann.

A little over two decades ago, the elites of Europe met in Maastricht, the Netherlands, to realize a long-held dream. It was to create a common currency that could be used throughout Europe, and possibly, the world.

The “euro” arrived, with great fanfare, in 1999, as a trading-only electronic currency. Three years later, the “eurozone” officially came into being. 11 national currencies were abolished and exchanged for euros at a fixed exchange rate.

Over the next decade, a growing number of European countries clamored to get on board. The eurozone eventually grew to 19 members.

Like so many other grand plans, the intentions of the European elites were good, albeit self-serving. The European Union (EU) itself was cobbled together after World War II to help prevent the rise of super-nationalists like Adolph Hitler. The euro was another step along the way. As former German Chancellor Helmut Kohl often said: “We seek a European Germany, not a German Europe.”

And the promised benefits were impressive:

Countries that joined the eurozone promised to abide by the “convergence criteria” of the Maastricht Treaty, signed in 1992. These included price stability, a government budget deficit of 3% or less of GDP, a debt-to-GDP ratio of 60% or less, exchange rate stability, and long-term interest rates no more than 2% above the rates prevailing in EU member states with the lowest inflation.

Based on these requirements, several members of the eurozone should never have been admitted. I explained in this essay how the Greek politicians engaged in such sleights of hand as not counting military spending as a government expenditure in order to qualify.

But fudged admission standards were far from the only flaw in the plan. Another was inflation. Despite the promise of price stability, prices for many products and services in euros were substantially higher than their equivalent values in the now defunct national currencies. I witnessed this firsthand when I was living in Vienna during Austria’s transition from the schilling to the euro. I especially noticed this trend in the cost of food and beverages. For instance, a Grosse Bier (large beer) typically cost AS35 in 2000. Three years later, the same beer (still very tasty) cost €3.50 – nearly 40% more in schilling terms.

But the largest problem of all was that once the countries using the euro abolished their respective national currencies, they lost control of monetary policy. This authority passed to the European Central Bank (ECB), based in Germany. And a monetary policy that might be good for Germany might not be appropriate for, say, Greece or Cyprus.

Moreover, what European nation will step up to the plate and spend the billions – or even trillions of euros necessary to back it up? In the US, the dollar is backed by the “full faith and credit” of the US government. But what national government backs the euro?

Not Germany, the largest and healthiest economy in the eurozone. Chancellor Angela Merkel has made it clear that her country won’t bail out miscreants like Greece. And now, it’s SHTF time.

Last week, Greece missed a $1.7 billion payment to the International Monetary Fund (IMF) – a small part of the $260 billion it owes international creditors.

Then, two days ago, in a national referendum, Greek voters rejected an ultimatum from the IMF that would require the country to embrace further austerity measures. That would worsen unemployment – already exceeding 25% – and require further cuts in pensions and benefit payments, which have fallen by more than half since 2010.

As a result, Greece is likely to leave the eurozone – perhaps as soon as this week.

In the meantime, Greece closed its banks and imposed capital controls. Bank depositors can withdraw only €60 per day. When the banks reopen, it’s likely that depositors will see their euro savings accounts forcibly converted into drachmas, Greece’s old – and now newest – currency.

The price of treating economic basket cases like Greece as if they were well-ordered societies like Germany has finally become clear. Without a lender of last resort, it’s up to Germany and other wealthy EU countries to pick up the tab if they want the euro experiment to continue. And it’s clear they’re not willing to pay.

Greece is only the first domino. In the next few years, I anticipate the economies of Southern Europe, which are almost as badly managed as that of Greece, to follow in its footsteps. Spain, Italy, and Portugal will be the first to depart from the euro after Greece. Next will be France and Ireland, which aren’t in much better shape financially.

In the end, there will be a core group of countries still using the euro, with Germany, as always, presiding over it. And Germany itself might exit the euro, if its voters tire of being asked for handouts by the remaining eurozone countries. If Germany goes, there’s not much left to keep it together.

There’s a larger lesson here as well, no matter what country you live in. Only hours before imposing capital controls and closing banks, Greek politicians promised they would never do so. Like politicians everywhere, they lied.

Moving money into assets that the politicians in your country can’t steal from you is the only way to protect yourself. At home, that means stockpiling cash, gold, food, and other tangible assets. It also means making investments outside your own country. An offshore bank account, international real estate, or precious metals in a secure private vault are all good ways to begin.

There couldn’t be a better time to start making preparations than now.

Comments Off on The Beginning of the End for the Euro

Famous politician gets caught in his own web

June 12th, 2015

By Mark Nestmann.

Talk about a comeuppance. Former Speaker of the House of Representatives Dennis Hastert, who helped force through Congress stricter laws against anonymous cash transactions, now faces financial ruin – and an extended jail sentence – thanks to the very same laws.

Hastert withdrew at least $1.7 million in cash from bank accounts he controlled while trying to avoid having the transactions reported to the US Treasury. That apparently set off alarm bells with the anti-laundering software banks use to identify “suspicious transactions” in customer accounts.

Now, Hastert has been indicted for violations of the Bank Secrecy Act and lying to federal investigators about the purpose of the withdrawals. Each charge carries a penalty of as much as five years in prison and a $250,000 fine. The government can also seize every dime in the bank accounts Hastert used illegally.

The first crime Hastert stands accused of committing is “structuring.” This is the act of making an effort to avoid reporting cash transactions by breaking up one transaction into a series of smaller amounts. Hastert was evidently trying to avoid having the banks he dealt with complete a “currency transaction report,” which they must file with the US Treasury for cash deposits or withdrawals larger than $10,000.

According to the indictment, from 2010 to 2014, Hastert withdrew large sums of cash in small increments, through more than 100 separate transactions. By 2013, the activity had triggered an FBI investigation. But when the FBI asked Hastert about the cash withdrawals, he told them that he was simply holding on to the cash for his own purposes. That turned out not to be true – and it led to a second count in the indictment for lying to federal agents.

The indictment claims that Hastert paid the money to a person identified as “Individual A.” Law enforcement sources subsequently revealed that Individual A is a former male student that Hastert allegedly sexually abused while serving as a high school wrestling coach in the 1960s and 1970s.

There are numerous ironies implicit in the story, along with an important lesson that the mainstream media will never mention.

Irony #1: Hastert, who for decades has campaigned against “gay rights,” appears to be a closet homosexual.

Irony #2: The man who made millions as a lobbyist after retiring as speaker of the House of Representatives was compromised by the very system he helped sustain.

Irony #3: Hastert often took credit for spearheading enactment of the controversial USA PATRIOT Act. However, the indictment suggests that the FBI used the Act’s expanded financial reporting requirements to investigate his cash transactions.

Irony #4: Hastert is only the latest straight-as-an-arrow politician done in by the “structuring” statute. Just seven years ago, former New York Attorney General Elliot Spitzer was felled when investigators discovered he was structuring cash withdrawals to make payments to prostitutes.

And the important lesson the media has completely overlooked?

It’s that fundamentally, there is no “victim” of the crimes for which Hastert was indicted. I’m not referring to the alleged sexual abuse decades ago, but rather, to his indictment for structuring and lying to the FBI.

Real crimes need to have a real victim. But who is the victim when someone withdraws lawfully earned money from his or her bank account? Or lies about doing it?

Put another way: Were you somehow injured in even the most remote way by Hastert’s unreported cash withdrawals or lying to the FBI? Was anyone you know injured? Indeed, can you conceive of any possible victim, other than Hastert himself?

There are countless federal, state, and local laws that criminalize conduct with no possible victim other than the perpetrator. Anti-drug laws are the most obvious example. In every state in the US, for instance, you can be incarcerated for mere possession of illegal plants.

There’s no doubt that Dennis Hastert has some explaining to do. But the real victim here of Hastert’s structuring scheme is Hastert himself, and no one else.

I suspect that prosecutors will drop criminal charges against Hastert. He’s a leading member of the political class and thus qualifies for special treatment. The end result could look like the case of Elliot Spitzer. There, prosecutors claimed there was “insufficient evidence” to bring Spitzer to trial.

Hastert might even get to keep the cash in the bank accounts he used for his structuring scheme, courtesy of a policy announced last year. The IRS Criminal Investigation Division says it will no longer confiscate funds associated solely with “legal source” structuring, except under “exceptional circumstances.” Earlier this year, the Justice Department announced it would follow the same policy.

Hastert’s millions – mostly generated from his lobbying activities after retirement – are unquestionably “legal source.” So, it’s possible he could get off scot-free. This is as it should be. However, even if Hastert escapes prosecution for a victimless crime, that doesn’t mean you will if you’re not politically untouchable.

Incidentally, the structuring statute is unique to the US. There’s nothing like it internationally, although a handful of countries ban “parceling” the transactions into smaller transactions below the applicable limits to avoid reporting. But other than the US, no other country explicitly targets lawful funds.

That fact suggests an obvious strategy: get your money out of the US into a financial system in which the government doesn’t look at your lawful assets as a piggy bank it can tap whenever it finds a pretense to do so. There couldn’t be a better time to start than now.

Comments Off on Famous politician gets caught in his own web

Even if Congress Repeals the PATRIOT Act, You’ll Still Have Zero Electronic Privacy

May 22nd, 2015

By Mark Nestmann.

I got a good laugh earlier this month when a federal appeals court ruled that the National Security Agency (NSA) could no longer collect the phone records of all US persons – and then store them in a massive database.

The laugh didn’t result from the decision itself, which I wholeheartedly support. It came from the media coverage of the ruling, which made it sound like the NSA could no longer vacuum up all of our electronic data without any meaningful limits.

The decisions issued by the Second Circuit Court of Appeals dealt with the NSA’s interpretation of Section 215 of the PATRIOT Act. That section authorizes the government to collect data “relevant” to terrorism investigations. However, whistleblower Edward Snowden revealed that the Bush and Obama administrations interpreted Section 215 as giving the government carte blanche authority to collect the phone records of virtually every person in the US.

This should come as no surprise. For many years, I’ve documented the phenomenon of “surveillance creep,” where a technology or law intended for narrow law enforcement or anti-terrorism purposes is used much more broadly.

And just like DNA surveillance, GPS surveillance, and even dog poop surveillance, the Second Circuit’s ruling will do little or nothing to restrict the NSA from sweeping up our electronic data. That will be true even if Congress fails to reauthorize Section 215 of the PATRIOT Act, as appears increasingly likely, and despite the claim by some in Congress that the repeal will “end bulk data collection.”

In fact, the PATRIOT Act is just a tiny piece of the global surveillance infrastructure the US government has constructed in the years since World War II. The lynchpin of this effort is the so-called “Five Eyes” club – a top-secret intelligence-sharing alliance first formed in 1946, whereby members agree to share intelligence they collect with one another. The Club’s first members were the UK and the USA. Canada, Australia, and New Zealand joined later, to form what we now know as the “Five Eyes.”

The Five Eyes agreement – first documented in 1982 in James Bamford’s landmark book on the NSA, The Puzzle Palace – contains a really nifty tool. Nifty, that is, if you work for the NSA or another intelligence agency of a Five Eyes signatory. It includes a clause that makes clear that each member agrees not to spy on citizens of another member without permission from that other member.

So, if Congress repeals Section 215, what do you think will happen? Simple. The NSA will simply “outsource” this data collection to one of its Five Eyes partners. Indeed, this type of outsourcing is common and longstanding.

For instance, in the 1970s, the Communications Security Establishment, Canada’s equivalent of the NSA, asked the US to monitor the communications of former Canadian Prime Minister Pierre Trudeau’s wife, Margaret. Was Margaret a suspected terrorist? A narcotics kingpin? A spy spilling secrets to the former Soviet Union? Not at all… When her marriage to Pierre foundered and they separated, she had affairs with the likes of Ted Kennedy and Mick Jagger. This, of course, justified surveillance by the world’s most sophisticated monitoring network.

The Five Eyes agreement isn’t the only NSA “solution” to the possible repeal of Section 215. There are numerous other ways the NSA can grab your phone records, and much more.

The most important option is Executive Order 12333, authorized by President Ronald Reagan in 1981. This order gives free rein to the NSA to spy on anyone, as long as the surveillance takes place outside the US. However, if the NSA “incidentally” collects the contents of a communication within the US, the order allows it to be retained.

In today’s networked world, “incidental” collection of data is more the rule than the exception. For instance, all major domestic email providers have backup servers outside the US. To retrieve the data, all the NSA needs to do is to tap into these servers – a capability the Snowden leaks demonstrated it has practiced for years.

The bottom line is that if you want to “privatize” your communications, you’ll need to work at it. Basically, there are five steps you should take:

One thing is for certain: Governments don’t cede power willingly. Edward Snowden provided overwhelming evidence that the NSA is much more focused on assembling data for blackmailing current and future political enemies than it is in unearthing terror plots. And it’s storing that data, permanently, in mega-facilities such as a data center in Utah that’s five times the size of the US capitol building.

Nothing less than a political earthquake will change this status. And the repeal of Section 215 represents only a very small tremor.

Don’t say you haven’t been warned.

Comments Off on Even if Congress Repeals the PATRIOT Act, You’ll Still Have Zero Electronic Privacy

Will Central Banks Abolish Cash?

May 10th, 2015By Mark Nestmann.

Cash has never been a popular asset with the totalitarian set. It’s difficult, if not impossible, to trace. Cash makes it possible to do business “off the books.”

For decades, with the US leading the effort, governments have engaged in a War on Cash. The original justification for this war was to fight racketeering. The War on Cash morphed into the War on Drugs, then the War on Money Laundering, and subsequently, the War on Terror.

But now, central banks and their lackey governments have a new rationale for the War on Cash: the very existence of cash makes it more difficult to enforce negative interest rates. That’s a big deal, because nearly $3 trillion worth of bonds with negative interest rates have already been issued. Incredible as it may seem, investors actually pay financially insolvent governments for the privilege of buying their bonds. Negative interest rates punish banks that fail to make loans but instead maintain reserves at a central bank. And of course, they punish savers seeking a positive return on their investment.

The European Central Bank has had negative interest rates in effect since June 2014. These rates apply to the “deposit facility rate,” which is the rate on “excess reserves” banks maintain at the ECB. Currently, that rate is -0.2%. If you’re a bank in the eurozone, your “reserves” gradually dwindle in value if you don’t lend them out. For instance, after one year at a -0.2% rate, €1 million of your reserves would only be worth €998,000.

The Danish and Swiss national banks have gone even further, with negative interest rates of -0.75%. After a year, 1 million Danish krone or Swiss francs would be worth only DKK/CHF992,500, respectively.

This policy isn’t reserved just for banks. I hold a position of Swiss francs at a domestic brokerage house. A few weeks ago, I was informed that money market holdings over CHF100,000 would now be subject to negative interest rates. I suspect this policy will gradually percolate into money market accounts for all currencies sporting negative interest rates.

Now, I can understand why central banks impose negative interest rates. They’re desperate to reinvigorate national economies that remain mired in recession years after the economic collapse of 2007–2009.

I also understand the reluctance of banks to lend. Debt levels in developed economies, especially Japan and the eurozone, are at all-time highs. Indeed, debt levels have grown by 40% since the last financial crisis. And cash-strapped borrowers are the last candidates to which banks want to extend credit.

The bottom line is that developed economies are so deeply in dept that they can no longer grow. The solution the central banks offer is more debt, but debt issued at negative interest rates.

While I get dizzy when I start thinking about the concept of paying someone for the privilege of holding my money, there’s an easy, albeit inconvenient, way to deal with the problem. And that’s to hold assets in cash. After all, 100 Swiss francs in a floor safe will still be worth CHF100 in 12 months, not CHF99.25.

Banks and governments don’t like that option one bit. Citigroup Chief Economist Willem Buiter made headlines a few weeks ago when he proposed abolishing cash to allow banks to impose negative interest rates. He suggests negative interest rates as low as -6.0% annually be imposed in financial crises, to force banks to lend and consumers to spend.

Currently, the US doesn’t have any restrictions on spending cash or even moving it across a national border, although there are strict reporting rules. If you deposit or withdraw more than $10,000 from a bank or other financial institution, the bank must file a “currency transaction report” with the US Treasury. In some areas subject to “geographic targeting orders,” the limits are reduced to $3,000 or even less.

Most Americans know nothing about these rules, which has led to countless numbers of innocent people having their savings confiscated and in some cases even being imprisoned. I most recently wrote about this racket in this essay.

Other countries, though, have been much more aggressive in the War on Cash:

Similar restrictions are in place in Belgium, Bulgaria, Greece, Mexico, Russia, Uruguay, and a handful of other countries.

Naturally, these restrictions are justified by the need to fight “tax evasion” and “terrorism.” But I think the real reason is to force savers to help prop up the tottering banking system. And don’t forget that the global “bail-in” model applies to these deposits. If a bank goes bust, depositors must share in the losses, as I discussed in this essay.

In the meantime, numerous banks have restricted the ability of customers to withdraw cash. In Switzerland, the Swiss National Bank – the country’s central bank – prohibited a large hedge fund from withdrawing cash out of its bank account to avoid negative interest rates.

Could these restrictions be a bellwether for outright confiscation or prohibition of cash? I don’t see that as likely, because it would raise such a political outcry. What’s somewhat more likely would be a cash recall along the model first proposed by former US Treasury Secretary Donald Regan in 1989.

Regan recommended that all $50 and $100 bills be recalled and replaced with a new currency. The changeover would occur in a 10-day period, Regan proposed, and the old money would no longer be legal tender after that time. Regan also recommended that anyone turning in more than $1,000 in old bills be forced to prove that they had paid all taxes on the cash and that it had not been generated through illegal activity. Otherwise, the cash would be confiscated.

Negative interest rates and the escalating restrictions on cash transactions are just two more indications of the desperate situation the global financial system faces. And they call for urgent defensive measures, such as:

As I’ve said before, the global experiment in negative interest rates combined with escalating levels of debt will eventually end – badly. I don’t know when it will happen, but when it does, it won’t be the central bankers and politicians who designed these policies who get burned. It will be ordinary citizens like you and me.

Get your assets out of the “too big to fail” banks – now. It’s only a matter of time before the SHTF.

Comments Off on Will Central Banks Abolish Cash?

Why Janet Yellen Should Start Smoking Cigars

April 8th, 2015

By Mark Nestmann.

Every three months, the mainstream media participate in a ridiculous charade: interpreting the quarterly announcements from the Federal Reserve Board of Governors.

The first time I paid much attention to this spectacle was more than 30 years ago, when Paul Volcker was Fed chairman. Pundits joked that investors could get a feeling for the direction of interest rates by watching where the ashes from Volcker’s ever-present cigar would land. If they drifted to his right, rates would go up… to his left, rates would decline.

Interest rates, of course, are supremely important in a capitalist economy. And they’re especially important for baby boomers like me who are eying retirement and yearning for higher returns on our fixed-income investments: savings accounts, CDs, bonds, etc. But since current Fed Chairwoman Janet Yellen doesn’t smoke, we can no longer use the cigar ash indicator to predict the rate’s future direction. But since current Fed Chairwoman Janet Yellen doesn’t smoke, we can no longer use the cigar ash indicator or the best cigar humidor to predict the rate’s future direction

For the last seven years, we’ve been hoping for higher rates in vain. Ever since 2008, the Fed has held the Fed Funds Rate – the rate at which financial institutions trade balances held by the Fed – at effectively 0%. The official reason for this ultra-low rate has been to “grow the economy” out of the financial debacle of 2007-2008, the worst economic downturn since the Great Depression of the 1930s.

We boomers got a glimmer of hope last December, when the Fed announced that the era of ultra-low interest rates would eventually end. But it also stated that:

Based on its current assessment, the Committee judges that it can be patient in beginning to normalize the stance of monetary policy.

On March 17, though, in the Fed’s most recent quarterly pronouncement from the pinnacle of global finance, it didn’t include the word “patient.” The media frenzy was palpable and the market reaction immediate. Investors dumped interest rate-sensitive investments, with bond funds leading the way down. After all, newly issued bonds with higher interest rates will be more attractive than older bonds with smaller payments.

If they ever get issued, that is.

Personally, I feel that the Fed announcement is much ado about nothing. The Fed will never significantly raise rates, at least not in my lifetime.

It can’t. The consequences would simply be too dire… and not just to the domestic economy.

The reason the Fed won’t raise interest rates has nothing to do with economic growth or the lack thereof. No, the Fed won’t do so because a national treasury with an $18 trillion debt and unfunded liabilities exceeding $200 trillion simply can’t afford to make much higher interest payments.

If this average interest rate were to rise to just 1%, interest payments on the debt would increase by a staggering $180 billion. And if interest rates were to return to their historical average of around 5%, US taxpayers would need to cough up nearly $900 billion in additional taxes each year to pay the tab.

It’s easy to assume that the reason interest rates have remained so low is that the Fed really, sincerely, wants to keep the US economy afloat. It’s also easy to conclude that the reason investors haven’t forced the Fed to increase rates by not purchasing its debt is because the US is such a fantastic credit risk. But the fact is, at the same time the federal deficit has been soaring, the Fed has done what central banks so frequently do: create money out of thin air. It has then taken that “funny money” and purchased a big chunk of federal debt on its own books.

Incidentally, economies in other developed nations aren’t any better off, especially in most of Europe and Japan. Despite the absence of the word “patient” from the Fed’s latest announcement, interest rates in the US and most other major global economies won’t rise anytime soon, perhaps not for many years.

The long-term implications of this policy are grim for anyone seeking a safe retirement. If you’re planning to retire anytime soon and are hoping to earn more than 1%-2% in a “safe” portfolio of bonds… think again. If you think your pension with guaranteed payments is secure… think again. Chances are, it won’t be able to generate enough income to meet its obligations.

Fortunately, there are alternatives, but you won’t find most of them in the US. I’m earning 3% in US dollars in a CD held at a very liquid, well-capitalized bank in Panama, for instance. I own AAA-rated bonds denominated in New Zealand dollars that pay about 4%. I also own a lot of precious metals, because even if the Fed manages to keep interest rates at their current level, the federal debt will continue to metastasize. There really is no turning back, and when the global monetary system eventually collapses, gold will be the only viable alternative.

Comments Off on Why Janet Yellen Should Start Smoking Cigars

Is this the end of the Euro?

March 26th, 2015

By Mark Nestmann.

With the US dollar hitting multiyear highs against other global currencies almost daily, Americans are in a sweet spot for making international investments. Your US dollars will buy a lot more rubles, yen, and Canadian dollars than they would a year, or even a month, ago.

But it’s the dollar’s rise against the euro, the official currency for 19 EU countries, that has the world’s attention. On March 13, the euro hit an intraday low of 1.046, its lowest level against the dollar in 12 years. It’s bounced back a bit since, but indeed, the euro has fallen nearly 25% against the greenback since July 2014.

Economic pundits attribute the collapse in the euro’s value to the actions of the European Central Bank (ECB). The ECB has embarked on a €1.1 trillion effort to revitalize eurozone economies that never really recovered from the global financial collapse of 2007-2008. It has announced it will buy €60 billion of eurozone government bonds monthly through September 2016.

The objective of this exercise is to encourage banks to lend more money. Banks are supposed to make more loans. The idea is that banks take €60 billion and buy new assets to replace the bonds they sold to the ECB. That in turn is supposed to cause stock prices to rise and interest rates to fall, boosting investment in the eurozone.

Where will the ECB get the money? It will do what central banks do best: create the money out of thin air through “quantitative easing” (QE). The ECB and other central banks have run out of ways to stimulate global economies. If QE doesn’t work, there’s no backup plan – just more QE.

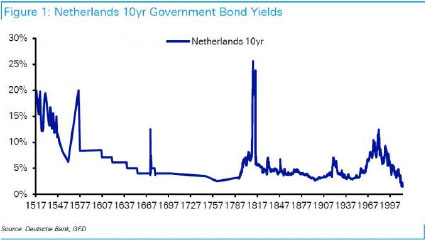

And there are plenty of indications that it won’t work. Even before the ECB climbed onto the QE bandwagon, interest rates in some eurozone countries were already at 500-year lows. Here’s a chart, for instance, of Dutch interest rates since 1517. As you can see, they’ve never been lower.

Indeed, the ECB itself started charging banks that hoard cash at the central bank negative interest rates last June (currently -0.2%). This policy punishes banks that have strict lending standards and encourages them to lend money.

The fall of the euro spells big opportunities for Americans who have most of their savings in dollars. Without doing anything at all, your US dollars will buy a lot more euro-denominated assets than they could only a few months ago. For instance, that apartment in Vienna I’ve been eyeing for years is now 25% less expensive in dollar terms than it was only a few months ago.

But along with these opportunities come risks. And not just the obvious ones.

The obvious risk, of course, is that the euro could fall further. While negative interest rates may give banks an incentive to lend money, and consumers and businesses an incentive to borrow, it makes the currency less attractive to investors. For that reason, I think the fall in the euro could go further. Indeed, the euro’s all-time low against the US dollar is just above 82 cents, a level it reached in 2000. That’s nearly 25% below its current levels.

A less-obvious risk is if the country you decide to invest in decides to leave the euro. What if I wanted to buy an apartment in Athens, for instance, rather than Vienna?

At first glance, buying property in Athens sounds like a no-brainer. Prices for the average residential property are down more than 40% in euro terms since 2008. Combined with the fall in the value of the euro, that means investors with greenbacks to burn can buy property in Athens at a 50% savings from what they could only a few years ago.

But if Greece were to abandon the euro, the government would need to resurrect the drachma – the currency Greece used prior to joining the euro – overnight. It’s unlikely anyone would be excited at the prospect of buying drachma-denominated bonds, so the Greek government would have to offer sky-high interest rates to pay civil servants, finance social benefits, and defend its borders. Some economists think that the value of the “new” drachma could fall 40% or more in a matter of days.

The prospect of a “Grexit” (Greek euro exit) is real, as I explained in this essay. And not only Greece – Spain, Italy, and Portugal all have fiscal problems only marginally less severe than those of Greece. All of these countries would face the same dilemma as Greece if they were forced to revert to pre-euro pesetas, lira, or escudos.

That’s why I’m not in a hurry to buy any assets in these countries. I think that despite the fall of the euro against the dollar, assets in the countries on the southern periphery of the eurozone could get a lot cheaper in the years – and possibly months – ahead.

There’s an even less-obvious risk as well. What happens if not just sick economies like Greece pull out – or are forced out – of the euro, but relatively healthy ones like Germany do so as well? After all, German taxpayers are tired of footing the bill to pay (among other outrages) for Greek civil servants to retire at an average age of 53. What would happen if Germany abandons the euro and reverts back to the Deutsche mark?

In that event, the exact opposite effect would probably occur: The value of the Deutsche mark would soar as investors flock to it seeking a safe currency haven. That’s why if I invest anything more in the eurozone than I already have, I’ll be looking to put it into stronger economies like Germany and Austria.

If the euro does collapse, and the countries now comprising the eurozone resurrect their own currencies, EU policymakers will view it as a colossal defeat for their dreams of a centrally planned currency. Indeed, the loss of confidence could be so shattering that it encourages Europe’s power elites to do something that is now unthinkable: revert not just to pre-euro currencies, but to gold.

From the time of ancient Egypt until the early 20th century, gold was the backbone of the global economy and the ultimate store of value. It’s not a particularly attractive asset from a central planner’s perspective, which is why it’s gotten short shrift during the last century. After all, you can’t devalue it, and you can’t create it out of thin air. But once the ECB’s QE program meets its demise along with the euro, gold could well be the only real option left.

Comments Off on Is this the end of the Euro?

Is This the First Nail in the Coffin of Citizenship-Based Taxation?

March 21st, 2015

By Mark Nestmann.

US citizens who expatriate – those who give up their citizenship and passport – don’t get a lot of respect.

Take Facebook co-founder Eduardo Saverin, for instance. When the Brazilian-born Saverin gave up US citizenship in 2011, it led to a political witch-hunt.

Sen. Charles Schumer (D-NY) responded with a proposal he called the “Ex-PATRIOT Act.” The law would permanently bar wealthy expatriates like Saverin from ever returning to the US, even for a visit. “Eduardo Saverin wants to de-friend the United States of America just to avoid paying taxes,” Schumer declared. “We aren’t going to let him get away with it.”

Oh, yeah? When Eduardo expatriated, he had to pay an “exit tax” on the increase in value of his Facebook stock. Virtually every dollar of gain was subject to the exit tax. I estimate he paid an exit tax of more than $350 million just on the value of these shares.

Does that sound like tax avoidance to you? If that really was Eduardo’s intent, he didn’t do a very good job of it. It’s true the future appreciation of his Facebook shares wouldn’t be subject to US tax, assuming he didn’t have to sell them to pay the tax. But those gains could be subject to tax in another country, and it’s even possible that Eduardo could be forced to pay tax twice on the same gains, since the US exit tax isn’t coordinated with the tax laws in other countries.

But the fact is, for every rich and photogenic expatriate like Eduardo Saverin, there are dozens of Americans who don’t fit his profile.

Carol, a Canadian citizen who emigrated to Canada with her husband in 1969, is a great example. After arriving in Canada, she obtained Canadian citizenship, and later became the mother of a developmentally disabled son, Roy. Since Roy was born to US-citizen parents, he automatically became a US citizen. Now Roy benefits from something called a Registered Disability Savings Plan (RDSP). Carol and her husband regularly contribute to this plan, and the Canadian government matches their contributions up to C$3,500 annually.

When Carol acquired Canadian citizenship, she thought that she had automatically given up her US citizenship. And she had no idea her disabled son would automatically be a US citizen even though he was born in Canada. It’s easy to make that mistake, because the US State Department calls the acquisition of a second nationality an “expatriating act.” (It is, but only if you confirm your intention to expatriate at a US consulate.)

Carol and her husband have now lived in Canada for 46 years, and their son has spent his entire life there. Of course, the entire time, they’ve paid Canadian taxes, which are considerably higher than taxes in the US.

Yet, under the US tax rules, she’s treated as if she never left the US. That’s because unlike any other major country, the US imposes taxes on its citizens, no matter where they live. And get this: The IRS considers the matching grants to Roy’s RDSP as taxable income. Roy’s parents are even supposed to file a form declaring the RDSP as a “foreign trust.” The penalty for not filing the form is $10,000 or 35% of the value of the assets conveyed to the “foreign trust,” whichever is greater. And that penalty applies for every year the RDSP has existed.

Obama Proposes Relief for Some Expatriates

Now the Obama administration has proposed a modest reform of the grossly unfair system of citizenship-based taxation in its 2016 budget presentation. Certain individuals who were dual citizens at birth would be permitted to expatriate under a considerably easier process than currently applies.

Under the current expatriation law, wealthy “covered expatriates” (defined here) are subject to an “exit tax” and other unpleasant tax consequences. Currently, the only ways to avoid the impact of this tax if you’re a covered expatriate is if you:

If you’re not a covered expatriate, or if you meet these tests, you won’t have to pay the exit tax when you give up US citizenship. But you’ll still need to sign a certification that you were compliant with all US tax and reporting obligations for the five years preceding your expatriation. That poses big problems for people like Carol, her husband, and her disabled son Roy, who must still pay tax and interest on the “income” the Canadian government paid into their RDSP.

Obama’s 2016 budget proposes to eliminate this certification requirement for some people who were dual citizens at birth. It’s a step in the right direction, although of the 7 million US citizens living abroad, most won’t qualify for relief under this proposal. But many – perhaps as many as several hundred thousand – will benefit.

Does Obama Really Feel US Expatriates’ Pain?

I’d like to think that Obama and his team heard the outcry from the millions of Americans living overseas, who, uniquely among citizens of major countries, must endure citizenship-based taxation. Due to laws like FATCA (the Foreign Account Tax Compliance Act) they also find it increasingly difficult to hold bank accounts, obtain mortgages, acquire insurance coverage, and carry on the other aspects of ordinary life they once took for granted. It’s simply easier for the foreign financial institutions subject to FATCA to fire their US clients than to deal with the IRS.

But I don’t think Obama gives a rat’s ass about Americans living abroad. He’s much more concerned about making FATCA a success, so he can fulfill his campaign promise of “shutting down” what he calls “offshore tax havens.” And FATCA – the centerpiece of this plan – faces real threats, as I wrote about in this essay.

Now there’s another threat. In Canada, two US-Canadian dual citizens at birth have filed a lawsuit against the Canadian government. The lawsuit demands that the Canadian courts declare it illegal for the Canadian government to discriminate against US-Canadian dual citizens. The FATCA intergovernmental agreement between the US and Canada does discriminate – it forces Canadian financial institutions to release more information to the IRS than they are permitted to disclose to the Canadian tax authorities.

If this litigation succeeds, it could prove disastrous for FATCA – not just in Canada, but globally. But if Obama’s proposal becomes law, it would weaken the plaintiffs’ arguments – perhaps sufficiently to have their claims thrown out of court.

But it’s highly unlikely that the Obama budget proposal will become law. Congressional blowhards like Chuck Schumer will surely oppose it, and Republican lawmakers hardly want to make it look as if they’re friendly to the likes of Eduardo Saverin. In theory, Obama could issue an executive order authorizing the Treasury Department to make the change, but I really doubt he’d use up what little political capital he has left to do it.

That doesn’t change the fact, though, that Obama made the proposal to begin with. While his motives may be purely political, this is the first time since the income tax was adopted in 1913 that a president has proposed modifying the current regime of citizenship-based taxation. While this effort is unlikely to succeed, it won’t be the last. And in retrospect, it may eventually be seen as the first nail in the coffin of citizenship-based taxation.

Comments Off on Is This the First Nail in the Coffin of Citizenship-Based Taxation?

What Happens When Big Brother “Privatizes” Debt Collection?

March 13th, 2015

By Mark Nestmann.

It’s bad enough to have the IRS or another government agency after you. But when Uncle Sam – or even a state or local government – hires a collection agency to chase after you, things can go downhill fast.

Ordinary debt collectors must abide by consumer protection laws that forbid them from using strong-arm tactics. For instance, they can’t threaten to have you arrested or suspend your driver’s license. But when the government hires an agency to collect a debt from you, the gloves come off. Even an unpaid toll of $1 can quickly balloon into a debt of hundreds of dollars.

David Jackson is a poster child for this strategy, which has gained immense popularity in this age of “privatization.” A $100 speeding ticket in 2010 quickly mushroomed into a $2,200 liability once the city of Overland Park, Kansas, turned the matter over to a collection agency, Linebarger Goggan Blair & Sampson. Homeless and broke, Jackson couldn’t afford to pay all the penalties, interest, court costs, and fees Linebarger tried to collect. When he failed to pay, Linebarger followed through on its threat to have him arrested. He wound up in jail numerous times – and was billed $35 per night for jail fees.

The mostly poor and middle-class victims of privatized debt collectors often have no recourse against anyone, least of all the collection agency, which may be shielded from lawsuit or prosecution under the doctrine of “sovereign immunity.”

In many cases, the debts collected by agencies like Linebarger are for bills from years or even decades ago. And the government agencies that refer the cases often issue arrest warrants, garnishment orders, driver’s license suspensions, etc. – all cited in the collection letters.

Like the civil forfeiture racket I’ve written about in previous essays, outsourcing debt collection is a sweet deal for state and local governments, since the debtors, not the governments, must pay the collection fees. These fees are much higher than in collection efforts for ordinary creditors.

Some states permit regular collection fees of 40%; effective fees in toll collection cases start at 100% and can go much, much higher. And while most states limit garnishment orders to 20% or less of a person’s income, when it comes to debts owed the government, some states permit a court to garnish 100% of your after-tax earnings.

Some of the cases pursued by collection agencies come as a result of misconduct by police or government officials. That’s why New York City resident Laverne Dobbinson received a $710 bill from Linebarger in the summer of 2012. A few months earlier, Laverne’s 27-year-old son, Tamon Robinson, was mowed down by a New York City police car. The official accident report said that Robinson “ran into” the car and then fell backwards onto the pavement. He later died of a head injury. But the autopsy report released by the city medical examiner found that Tamon had died due to being “struck by police vehicle during pursuit.”

Several months later, apparently based on the accident report, Laverne opened a letter from Linebarger addressed to her son. The letter sought reimbursement of $710 for “property damage to a vehicle owned by the New York Police Department.” It threatened a lawsuit if the bill wasn’t paid immediately.

Laverne, who was already pursuing a wrongful death lawsuit against the city, turned the letter over to her attorney. Linebarger acknowledged that the city had referred to it numerous collection cases, including that of Tamon Robinson. Linebarger stopped its collection efforts only when it received proof of Tamon’s death. And in 2014, the city settled Laverne’s wrongful death lawsuit for a hefty $2 million payout.

Of course, privatization isn’t just a US phenomenon. In response to sluggish economic growth and growing deficits, governments worldwide have privatized airports, energy monopolies, and many other types of facilities formerly operated as public services. This trend is to be applauded; time after time, for-profit businesses have proven they can provide superior services for lower costs than governments can. Japan is a great example; after the government privatized inter-city routes beginning in the 1980s, service improved dramatically and ticket prices fell. But neither Japan, nor any other country outside the US that I’m aware of, has privatized collection of debts owed to the government.

Ordinarily, I would be the last person to complain about privatization and other efforts to reduce the power of Big Brother. But private debt collectors acting on behalf of government agencies should abide by the same rules as they do to collect any other debt. Anything else opens the door for manifest abuse… along with so many other abuses that are all-pervasive in the US.

Offshore, anyone?

Comments Off on What Happens When Big Brother “Privatizes” Debt Collection?

Why This Greek Tragedy Could Mean Global Disaster

March 5th, 2015

By Mark Nestmann.

One of the assumptions of the eurozone – those 19 countries in Europe that use the euro as their national currencies – is that if any country left the zone, economic disaster would follow in its wake.

Only a few days ago, it appeared that heavily indebted Greece might be forced to drop the euro and return to the drachma, the currency it used before the euro.

During the 1990s and early 2000s, Greece was spending money like a sailor on shore leave with a limitless credit card. The government ran up debts amounting to hundreds of billions of dollars to prepare for the 2004 Olympics, among many other infrastructure projects. It also promised retired Greek citizens some of the cushiest pensions in the EU.

In 2002, Greece was among the first EU members to adopt the euro. Entrance into the eurozone was contingent on Greece’s accomplishing certain reforms and demonstrating a threshold level of economic prudence. Among the requirements was to maintain a budget deficit of less than 3% and a total government debt under 60% of GDP.

Greece never even came close to meeting these targets. To make it look as if it were, Greek politicians engaged in such sleights of hand as not counting military spending as a government expenditure. But if it wanted to join the euro, Greece needed to do more. And Greek politicians weren’t about to ask voters permission to dismantle the cradle-to-grave welfare state financed by borrowed money.

To solve the problem, the government hired Goldman Sachs to help tidy up its balance sheet. Goldman created a series of currency swap arrangements using fictional exchange rates. The swaps took billions of dollars of debt off Greece’s balance sheet and allowed the country to issue far more debt than what was actually showing up in its account ledgers. Goldman used similar financial engineering to help prop up ill-fated energy trader Enron Corp., and we all know how well that experiment turned out.

In other words, Greece never, ever should have been allowed to join the eurozone. But now that it’s part of it, there seems to be no end to the willingness of EU politicians to throw money at Greece to keep it from leaving.

The Greek euro-farce escalated in 2010, when what has become known as the “troika” – the European Commission (the executive body of the EU), the International Monetary Fund (IMF) and the European Central Bank (ECB) – agreed to a €110 billion bailout after Greece agreed to draconian austerity measures. Then, in 2011, the EU agreed to second bailout, this time to the tune of €130 billion.

And Greece did deliver some of the promised reforms. Taxes were raised, pension payments were cut, and the cradle-to-grave welfare state was partially dismantled. Government salaries were frozen. Annual government spending fell nearly 25% from 2011 to 2015.

But austerity alone wasn’t enough, as the Greek economy also shrank 25% during this period. More than one in four Greeks of working age are unemployed. As matters now stand, while Greece’s budgetary position is much improved, with a 2014 deficit of only 2.5% of GDP, its debt-to-GDP ratio is much worse than it was in 2010: 175% vs. 130%.

In a sane world, the EU never would have allowed Greece to become part of the eurozone. And as soon as the EU understood the extent of the Goldman-inspired subterfuge to allow Greece into the eurozone, it would have forced Greece out of it.

You could also be excused for thinking that the election last month of former communist youth activist Alexis Tsipras as prime minister of Greece might have been the end of the charade. Tsipras, whom I wrote about in this essay examining the political impact of austerity measures, campaigned on a promise to end them. (Yes, I “called it”!)

Among other goodies, Tsipras promised free electricity and food stamps for the poor, and boosts in pension payments. He also promised an end to privatizations of government-owned shipping facilities, airports, and energy companies.

The election of Tsipras sparked a fresh euro crisis. But all is now smoothed over. Tsipras has promised the EU to resume the process of reform, even at the risk of setting off a revolt from his leftist backers. In return, the EU has given him four months to start implementing the promised reforms. My guess is that Tsipras will be back in Brussels in four months, asking for more money. And the troika, spineless as an amoeba, will comply with the request.

Of course, Greece is only the most recent and most visible example of this “kick the problem down the road” farce. Central banks worldwide are engaged in desperate and increasingly futile efforts to rejuvenate growth and price inflation through quantitative easing and other stimulus measures.

The wholesale failure of these policies worldwide places central banks in a real bind. You can be sure that Alexis Tsipras won’t be the only politician from a small, heavily indebted EU country to ask for further handouts, at the same time resisting the demanded reforms.

Even in the US, the one country where some sluggish real economic growth has resumed, the Federal Reserve is under attack. The “audit the Fed” movement has, for the first time, real bipartisan support. No less an authority than Fed Chairwoman Janet Yellen warned last week of the dire consequences of auditing a central bank.

What is it that the central bankers fear most? Here it is: The policies they have put in place to encourage one asset bubble after another can no longer be sustained. Having inflated the biggest financial bubble in history, they are terrified that it will pop, with devastating economic consequences, leading to a global deflationary depression that will make the recession of 2008-2009 look mild by comparison.

The beneficiaries of central banks’ largesse – governments, money center banks, and stock market investors worldwide – are equally terrified. And if they’re not, they should be.

I don’t know when it will happen, but there will be, as my former boss Bill Bonner says, a “day of reckoning.” Only this debacle will not be sorted out in a day. Ordinary citizens who realize that central banks are powerless to stop the unraveling of the bubbles created by quantitative easing and similar measures won’t be happy. They will elect men like Alexis Tsipras who promise an end to austerity. But without a greater fool – central banks creating money out of thin air – they won’t be able to deliver on their promises.

Things could get really ugly for a while, as all the fiat money-created bubbles in real estate, stocks, and commodities collapse. Political and social unrest will become part of daily life in many countries, as it already is in Greece.

How do you protect yourself? For starters, don’t believe the establishment claptrap trumpeted by the mainstream media. Central banks can’t solve the problems they’ve created with their easy-money policies. And since the bubbles will collapse, make sure you’re out of real estate and other inflated assets before they do (other than possibly your own home and property you own debt free). Keep your liquid assets in physical currency or in strong, highly capitalized banks. Gold is fine, too, but since it’s a commodity, don’t be surprised if it falls in value along with everything else when serious deflation begins.

Comments Off on Why This Greek Tragedy Could Mean Global Disaster

Why Eric Holder’s “Good Deed” on Civil Forfeiture…Wasn’t That Good

January 31st, 2015By Mark Nestmann.

One of the departing initiatives taken by retiring US Attorney General Eric Holder was to impose limits on a legal process called “adoption.”

This is not the kind of adoption in which you add a child to your family. It is a process that allows local, county, or state police agencies to confiscate assets under federal civil forfeiture laws. In effect, the feds “adopt” the forfeiture and kick back up to 80% of the proceeds to the agency that originated the seizure.

The feds call this processing “equitable sharing.” A better term would be “legalized theft.” It’s almost beyond belief that the feds would actively encourage police departments to keep most of the money they seize, but they do. Not surprisingly, this inherently corrupt “policing for profit” scheme has led to abuse after abuse.

Civil forfeiture is a procedure that permits police to confiscate property without convicting, or even charging, the owner with any crime.

The cases have names like these:

Why don’t police seize assets under state law instead? Usually, it’s because state laws require that seized assets be earmarked for specific purposes, such as education, or deposited in the state treasury. But in a federal adoption, up to 80% of the value of the seized assets are handed to the seizing agency. Local prosecutors get up to 5% of the net proceeds.

Since adoption began in 1984, the Justice Department has “equitably shared” billions of dollars with seizing agencies, with total “sharing” of more than $400 million per year.

Holder’s action is a welcome start to civil forfeiture reform, but it’s not nearly as big a deal as the media have made it out to be. And Holder’s successor, Loretta Lynch, a forfeiture lover who boasted about seizing more than $900 million in 2013 alone, could end the restrictions at the stroke of a pen.

For starters, the media got the story wrong. In an article entitled “Eric Holder’s Good Deed,” The Wall Street Journal wrote that the Justice Department was suspending adoption altogether. The Daily Kos wrote that Holder was ending most types of civil forfeiture. Another article claimed that Holder “was ending the Federal Government’s ‘Equitable Sharing’ program, otherwise known as civil forfeiture.” Some people took that to mean that Holder had abolished civil forfeiture altogether, and a social media frenzy on Facebook and Twitter began. Forfeiture victims were even asking if they could get their property back.

Unfortunately, Holder didn’t abolish civil forfeiture… not even close. The text of Holder’s order makes that very clear, although not many reporters or social media gadflies seem to have read it. And even if his successor doesn’t reverse his reforms, they won’t have much impact on civil forfeiture, because adoption is only one of many ways that forfeitures can be processed under federal law.

What Holder did was to restrict adoption to a specific list of offenses involving “public safety.” The list includes firearms, ammunition, and child porn. But it no longer includes cash, so the infamous highway shakedowns of motorists for their cash by police in many states can no longer be processed as easily under federal law.

But cash seizures from motorists are only a tiny part of the nationwide civil forfeiture “industry.” And Holder’s order doesn’t affect adoption in seizures by state/federal joint investigations and task forces. Seizures that occur under federal seizure warrants likewise are exempted. So if a sheriff in Texas really wants that $9,000 you’re carrying in your vehicle, he can confiscate it by getting a federal judge to issue to seizure warrant, or under the authority of a federal/state task force.

This article by forfeiture defense attorney Brenda Grantland, founder of Forfeiture Endangers American Rights, explains the sordid process in detail.