By Andrew McKillop.

EXPENSIVE POWER AND THE URANIUM PINCH

Nuclear power is now one of the most capital-intensive, highest cost types of electricity generation which exists, around 5 – 8 times more expensive on a cost-per-kilowatt of capacity basis, than key alternatives like gas-fired power plants, windpower and solar photovoltaic plants. Uranium is far from abundant and only the near-zero rate of nuclear power capacity growth prevents a supply pinch from driving up prices – with uranium fuel costs presently making up about 12%-17% of typical operating costs for nuclear power plants.

THE URANIUM FLAG : NAMIBIA

Electron configuration 2-8-18-32-21-9-2

Atomic number 92 Atomic weight 238.02891

SOURCE/ MINING WEEKLY

In 2010, after two lost decades of low activity, with zero orders some years starting long before the Chernobyl catastrophe of 1986, and spanning the 1990s and start of the 2000s, the nuclear renaissance was in full flood. Just months before the Fukushima catastrophe struck Japan.

In July 2010, the WNA-World Nuclear Association (previously named the Uranium Institute) hailed the fact that over 50 reactors were under construction in 13 countries. Nuclear power capacity added through 2010-2020 was forecast by the WNA in 2010 as at least 75 GW (75 000 MW). Other estimates went beyond 100 GW.

Some country plans and proposals, especially as outlined by India’s NPCIL, claimed that India alone could develop 400 GW of nuclear capacity by around 2040. World total operating capacity of all 440 civil reactors operating in 29 countries in 2010 was about 340 GW.

New entrant and possible “new nuclear” countries in the 2010-2030 period were outlined by the WNA as possibly including Kazakhstan, Mongolia, Venezuela, South Africa, Nigeria, Ghana, Algeria, Sudan, Egypt, UAE, Kuwait, Saudi Arabia, Jordan, Vietnam, Singapore, Thailand, Malaysia, the Philippines, Bangladesh, Indonesia, Poland and several others – such as Libya – whose civil nuclear intentions are rather likely on hold, right now.

BATTLE OF THE BULGE

The chart below shows what expansion of uranium output would be needed if the Nuclear Renaissance was to happen:

(Source/ http://www.roperld.com/science/Nuclear )

Taking only 2010-forecasts and projections for nuclear power growth in the period 2010-2020 this would raise world total civil power capacity by over 400 GW in more than 45 countries by 2020, in other words at least a doubling of total capacity from today’s level around 340 GW.

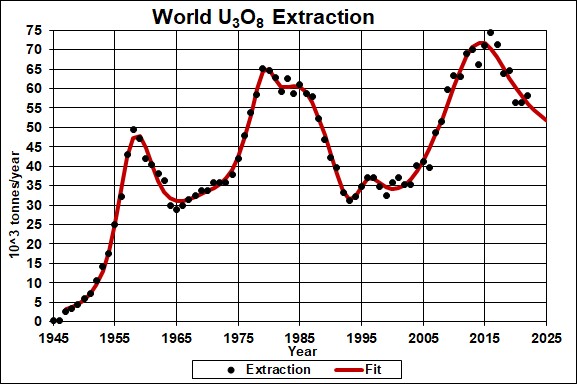

Under this scenario, world uranium requirements could rise to 120 000 tons a year by 2020, from their 2010 level of about 65 000 tons, further driven by increasing demand per “tranche”, that is bigger-sized power plant unit sizes, due to the trend for reactor sizes of around 1000-1200 MW each, compared with the present industry standard of 900 MW per tranche.

The massive uranium mining shortage is explained by the figure for world total mine output in 2010: about 53 000 tons. The balance of 12 000 tons was supplied from uranium stocks held by miners, power plant builders and plant operators, as well as government stockpiles.

The nuclear industry’s claim is that uranium prices are not important. Taking an industry standard 900 MW LWR, this typically needs around 350 tons of low enriched uranium fuel on start-up, and about 150 – 160 tons per year after that. At the most recent peak price for uranium, in 2007 at over US $ 130 per pound ($ 285 per kg or $ 285 000 per ton), compared with present prices (Dec 2013) reported by UxC at around $40 per pound, fuel costs of nuclear plants are relatively easy to figure. However the extreme problem of forecasting reactor fuel costs is underlined by the most recent-historic low price of uranium, in year 2000, at around $ 8 per pound. Uranium prices have swung from $8 to $130 and back to $40 in the space of 13 years.

The nuclear lobby and its industry spokespersons often counter this clear problem – of forecast shortage or surplus of uranium playing havoc with prices – with a smokescreen of technical, industrial and economic rationales which downplay the role and importance of uranium fuel and its prices for nuclear power. One favoured rationale is the “coming generation of fast reactors”.

THE PLUTONIUM SOLUTION

This “high tech rationale” is that an average industry standard 900 MW LWR produces around 0.225 grams of plutonium per day, and the world’s present 440-strong reactor fleet produces about 36 tons of plutonium per year. This could palliate or avoid potential future uranium shortage – and is also enough plutonium to produce about 3600 Hiroshima-size bombs of 1945, or 4900 Abdul Qdr “Bombs R Us” Khan nuclear device of 1987 with the same explosive and radiological fallout potential, per year.

Recycling this plutonium, using firstly MOX fuel in which low grade uranium is “cut” with plutonium oxide to produce reactor-capable fuel, and then moving to the use of plutonium to power Fast Breeder Reactors, which produce more plutonium that they consume, are favoured solutions to uranium shortage and high or unpredictable prices. Apart from the fast reactor route being a technological fantasy with stupefying human health risks, environment impacts and national security implications, this claimed-as-feasible shift is advanced by the nuclear lobby only because uranium shortage remains a dark shadow hanging over the industry.

Welcome to the plutonium economy.

Uranium prices, often with a delay, faithfully track oil prices and are not under control. When they soar, they add more negative weight to the economics of atomic energy. Possibly unknown to the most eager shills for nuclear power such as the Global Warming Boomers, Jim Lovelock and Al Gore, uranium mines operate diesel fuelled heavy machines on a 24/7 basis. After oil-majority fuelled uranium processing into “yellowcake”, it is exported in oil-fueled container ships to the “carbon conscious consumers” of the mature democracies, for energy-intensive fuel fabrication before final use in reactors, then transported using oil-fueled transport to reprocessing and disposal sites.

In the case of European countries using nuclear power, over 97% of their uranium fuel needs are imported.

The sheer physical shortage of uranium makes its production, stocks, supply and prices of key importance to the minds of political and corporate deciders, exactly like oil. The reasons are mainly simple ones, notably that supply is far behind demand and competition for supplies is now global, since the majority of consumer countries are heavily dependent on imported uranium – exactly like oil.

Exactly like the world oil industry, the uranium industry must resolve mine ownership and revenue disputes with host governments. In some cases – such as Niger – they must also handle geopolitical and national security issues, including hostage taking and world terrorism.

URANIUM MINING AT HOME ?

The world shortfall in uranium supplies can be related to the constantly shrinking, often completely abandoned uranium mining activity in the ‘old nuclear’ countries, and China and India, for a net combined total of nearly 99% of world uranium consumption being imported. The 2010 net shortfall of supply, about 12 000 tons, was around 7 times the USA’s total mine output, more than 14 times China’s total mine output, and close to 17 times India’s uranium mining output. It was also several hundred times French, German or British domestic uranium mine output.

Reasons why uranium mining “at home” was abandoned – making a mockery of claims for “national energy security” from nuclear power – include uranium depletion and the simple fact that uranium mining is dirty, generates huge spill and waste zones covering hundreds of square kilometres. Mining wastes also cause cancer through low level radiation and chemical toxins in affected water bodies. Impacts on agriculture, water resources and land values are all negative – so the problem is exported “over the horizon” to low income countries.

The uranium shortfall can also be understood by comparing the shortfall (12 000 tons in 2010) with Kazakhstan’s status of N°1 world uranium miner and exporter. In 2009, its record total production, which it equalled in 2010 and 2011 was about 13 500 – 14 500 tons. This only just exceeded the net 2010 shortfall of “fresh mined” uranium relative to world uranium fuel demand.

The uranium pinch will not go away.

POST FUKUSHIMA

The world uranium mining industry, following the 3/11 Fukushima disaster for nuclear power, now faces low and probably declining prices, certain to cause a shakeout of producers in which only low-cost miners can survive – comparable in fact to outlooks for gold mining! In other words, uranium prices, like gold prices have to rebound at some stage due to falling mine capacity and output, but also have to fall like gold prices for as long as miners dump their finished stocks on the market to try maintaining revenues. In addition, also like gold, the uranium market is very small in absolute size (about 55 000 tons a years, gold about 2 600 tons a year), easy to rig and heavily manipulated.

The world nuclear industry and its lobby, in classic style continues to argue that the world needs nuclear power and no uranium shortage exists – for example citing the US-Russian “Megatons to Megawatts” program of dismantling and recycling the radioactive materials from surplus nuclear weapons, to produce MOX-type fuels. At best this is a small stopgap and does not change the real outlook of uranium shortage – even with no expansion of the world’s current civil reactor fleet.

World accumulation of presently unusable plutonium from civil reactors (about 36 tons a year) is called “reactor grade plutonium” to distinguish it from bomb-grade plutonium, but its radiological health hazards are as extreme as bomb-grade material. Its capability for utilization in nuclear weapons devices is very high.

The mega-shift of the industry, from uranium fuel to plutonium fuel, is still considered both feasible and desirable by nuclear lobby stalwarts. Other “silver bullet solutions” touted by the lobby feature thorium fuels, but shifting the current reactor fleet to this supposed “alternate fuel” would take decades of extreme-high investment spending. Only one other semi-feasible alternative to uranium fuels would be the development of nuclear fusion reactors, but in this case a major limiting factor will be world mine supply of lithium for reactor blankets – also needed for rapid growing li-ion battery production.

The nuclear lobby and its related uranium mining lobby can be credited with continuing to play a spoiler role in world energy transition. By denying nuclear power plants are extremely capital-intensive and extremely high cost relative to alternatives – either fossil or other – and by denying there is any existing or future uranium fuel shortage, some political deciders continue to “believe in nuclear”. This can only increase the real and existing problems for rational energy transition, hinder its progress, and increase energy security problems.